-

Cash management, Trust and securities services

Project Agorá and cross-border payments

24 June 2026

Can tokenisation unlock the next chapter of correspondent banking? With Project Agorá, the Bank for International Settlements, seven central banks and more than 40 financial institutions are putting that question to the test. flow reports on the progress — and the road ahead

MINUTES min read

When we asked ‘what’s next for correspondent banking’ in September 2025, the answer was, and remains, “greater transparency, richer data, and faster processing across the ecosystem”.

Described by the Bank for International Settlements (BIS) as the "backbone of cross-border payments", the correspondent banking model has supported global commerce for decades. Yet the BIS also notes that the "sequential processing across multiple intermediaries” that underpins the model “delays payments, increases costs, limits end-to-end visibility and siloes liquidity, complicating cash and treasury management".1

Cross-border payments continue to grow in scale and importance, with flows reaching around US$195trn in 2024 and projected to rise to US$320trn by 2032.2 Within this, wholesale payments account for the vast majority of value – representing around 91% of cross-border payment flows in 2023 – making them an important area for innovation and efficiency gains.3

Under the umbrella of the G20 Roadmap for Enhancing Cross-Border Payments,4 various initiatives are seeking to address the industry’s longstanding challenges – from the global shift to ISO 20022 and the adoption of Swift GPI to the exploration of one leg out schemes and real-time payment system interlinking.

Alongside these enhancements to existing infrastructure, attention is also turning to what emerging technologies could achieve. One example is how tokenisation and programmability could help address longstanding wholesale cross-border payment challenges while building on the strengths of today's correspondent banking network.

Project Agorá

Enter Project Agorá, an initiative from the BIS and Institute of International Finance (IIF) with seven central banks and what is now 40+ banks and private enterprises (coordinated by the IIF). Launched on 3 April 2024,5 the project – named after the Greek word for “marketplace” – is exploring the design of a unified ledger where tokenised deposits interoperate with tokenised central bank reserves for policy aware, atomic cross border settlement.

Its aim is to modernise correspondent banking while preserving the two tier system.6 What this means in practice is finding a solution to several longstanding, high-priority pain points – as identified by the BIS Innovation Hub – that continue to affect wholesale cross-border payments. These include:

- Sequential/serial processing. Cross-border payments are typically processed step-by-step, with messaging, screening, reconciliation and settlement occurring sequentially across multiple institutions. Each participant can only act once the previous stage is complete, creating delays, increasing operational complexity and reducing overall efficiency.

- Predictability and availability (operating hours). Payments initiated outside overlapping market hours can experience delays, particularly where transactions span multiple jurisdictions and time zones. This can make the timing of settlement less predictable and require additional liquidity and treasury management outside normal business hours.

- Settlement risk. Funds or securities may fail to settle as expected, creating both credit and liquidity risk. The need to manage this risk can introduce additional controls, prefunding requirements and operational complexity, particularly in cross-border and cross-currency transactions.

The underlying premise is that a shared programmable platform can help overcome several of the pain points: replacing sequential processing with coordinated execution on a single ledger, extending availability beyond today's fragmented operating hours, and reducing settlement risk through atomic settlement mechanisms that ensure transactions complete simultaneously and irrevocably.

“Project Agorá reflects the kind of collaboration needed to drive meaningful change in a network-based industry such as correspondent banking”

The project also recognises that transforming cross-border payments is not solely a technological challenge. It requires the alignment of policy objectives, regulatory frameworks and commercial realities across multiple jurisdictions and institutions.

“By bringing together central banks, commercial banks and market participants from around the world, Project Agorá reflects the kind of collaboration needed to drive meaningful change in a network-based industry such as correspondent banking,” reflects Sabih Behzad, Head of Digital Assets & Currencies Transformation, Deutsche Bank, who represents the bank on Project Agorá. He continues, “While this approach represents a significant step forward, there remains a considerable journey ahead before such a platform reaches the level of maturity required for live, industrial-scale deployment.”

What is tokenisation?

But how could such a unified ledger concept work across both the central bank and commercial bank rails of the financial system? The answer lies in the architecture of tokenisation – the process of representing real or financial assets, which are traditionally recorded on a ledger, as digital tokens on a programmable platform.

The genesis of the approach for wholesale cross-border payments was first set out in the BIS Annual Economic Report 2023, which presented a Blueprint for the Future Monetary System: improving the old, enabling the new.7

The report stated: “Tokenisation could dramatically enhance the capabilities of the monetary and financial system by harnessing new ways for intermediaries to interact in serving end users, removing the traditional separation of messaging, reconciliation and settlement.”

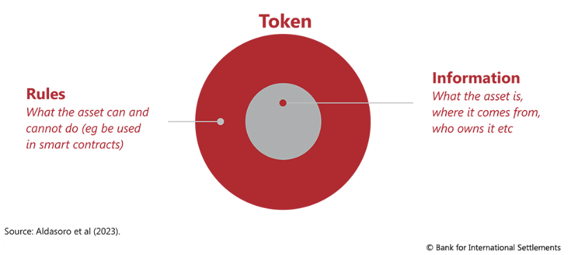

Figure 1: Structure of tokenisation

Source: Aldasoro et al (2023)

At its core, a token is a digital package that contains both information about an asset and the rules governing what can be done with it. As illustrated by the BIS, (see Figure 1) tokens merge two critical components:

- Information. Details about the asset, such as what it is, its origin, and its ownership.

- Rules. The logic defining what the asset can and cannot do, which can be enforced through smart contracts.

Unlike traditional systems where the rules for updating asset ownership are generally uniform for all assets, tokenisation allows these rules to be customised to meet specific user or regulatory requirements for individual assets.

As Hyun Song Shin, former BIS Economic Adviser and Head of Research who was recently announced as the 28th Governor of the Bank of Korea, put it at the launch of the project, “Tokenisation combines the record-keeping function of a traditional database with the rules and logic that govern transfers”. He explained, “We aim to improve existing capabilities and enable new ones, all based on the proven foundations of the two-tier monetary system with central banks at the core. These functionalities will come without sacrificing the safeguards on the integrity and governance of the monetary system.”

By tokenising – creating digital representations of commercial bank deposits and central bank reserves – Project Agorá seeks to “explore and enable secure and verifiable transactions”8. In turn, explained the BIS in an update published on 14 October 2025, “a Project Agora-type solution could more effectively support the intermediation of credit and the facilitation of payments, which sustains the economy through final settlement by central banks”.

The BIS explains how “settlement using central bank money (the safest and most liquid settlement asset) is crucial for a stable financial system as it eliminates credit risk”. This, it continues, “ensures the finality of transactions, prevents systemic risk from counterparty failure, and supports monetary policy effectiveness and public confidence in the currency”.

Project Agorá so far

The Project Agorá team at the BIS. Deutsche Bank’s Sabih Behzad is third from the right

By enabling atomic transactions – payments completed synchronously and in full – and preserving the critical relationships between depositors and banks, Project Agorá is charting a path that balances innovation with trust and reliability.

The objective has been to go beyond the proof-of-concept stage by building and testing a prototype capable of evaluating the potential of this new digital infrastructure.

This prototype has been developed iteratively since 2024 across multiple milestones and user-tested with participating institutions. It focuses on two transaction types: end-to-end (E2E) payments and payment-versus-payment (PvP) transactions, which, according to the BIS Innovation Hub, “offer the greatest opportunity to reduce the frictions that exist in today's cross-border payment ecosystem.”9

In addition to its technical innovations, Project Agorá has also looked to address critical regulatory and legal considerations. The project is examining how tokenised money can comply with existing rules on issues like settlement finality, anti-money laundering, and countering the financing of terrorism. By identifying potential gaps and challenges across multiple jurisdictions, the project is laying the groundwork for a regulated financial market infrastructure that could transform cross-border payments.

Prototype outcomes and next steps

Published on 27 May 2026, the BIS Innovation Hub report entitled Project Agorá: A shared programmable platform for wholesale cross-border payments sets out a thorough summary of the prototype itself, its key features and its intended outcomes (see Figure 2).10 The prototype demonstrated that:

- Tokenised commercial bank deposits can be combined with the trust, safety and finality of tokenised central bank reserves on a shared platform.

- The platform can support atomic, multi-currency settlement of wholesale cross-border payments, with the potential for around-the-clock operation if implemented at scale.

- Smart contracts enable financial institutions to embed workflow logic, compliance requirements and conditional payment triggers directly into transactions, supporting greater automation and programmability.

Together, these capabilities have the potential to reduce reconciliation burdens, manual intervention and other operational frictions – all key sources of delay, cost and inefficiency in today’s cross-border payments ecosystem.

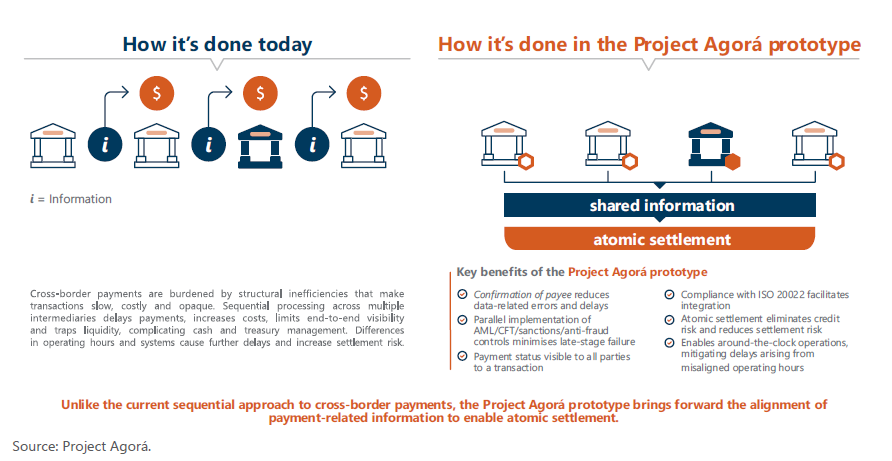

Figure 2: How the Project Agorá prototype works

While the prototype successfully demonstrated the feasibility of a shared programmable platform for wholesale cross-border payments, the BIS Innovation Hub report emphasises that it was developed with an intentionally narrow scope and should not be viewed as a solution that can be used at scale, but it currently represents a messaging layer. Several critical areas were outside the scope of testing in the initial phase, including operational resilience, throughput and latency, failover mechanisms, real-time monitoring as well as interoperability with domestic RTGS systems and integration with core banking infrastructure.

The prototype also relied on synthetic rather than live production transactions, meaning that "user behaviour, operational frictions and integration challenges that typically emerge in live environments could not be fully observed." As a result, further testing with real application flows may identify additional requirements, constraints and opportunities.

Finally, although no legal barriers to implementation were identified, the project highlighted a range of policy, operational and contractual questions that would need to be addressed before integrating the platform into the payment processing. These include governance arrangements, participant responsibilities, and the legal enforceability of programmable settlement rules across jurisdictions.

Looking ahead, the report indicates that Project Agorá's work is far from complete. While the prototype phase has concluded, project participants, including central banks, have expressed "strong and sustained interest" in further exploring its potential. We look forward to contributing to the next stage of Project Agorá as the concepts demonstrated by the prototype are further explored, potentially in real-world environments.

Timeline for Project Agorá

- 20 June 2023. ‘Blueprint for the future monetary system: improving the old, enabling the new’, the precursor to Project Agorá first explained in the BIS Annual Report11

- 3 April 2024: Launch of Project Agorá12

- 6-8 May 2024 BIS Innovation Summit presentation from BIS Innovation Hub13

- 27 May 2026 Prototype delivery announced14

- Next steps: live transactions

Sources

1 See Project Agorá at bis.org

2 FXC Intelligence, “New data: cross-border payments market now worth over US$194tn and is forecast to reach US$320tn by 2032”, 16 January 2025.

3 See G20 Roadmap for Enhancing Cross-border Payments at bis.org

4 See G20 Roadmap for Enhancing Cross-border Payments at fsb.org

5 See Project Agorá: central banks and banking sector embark on major project to explore tokenisation of cross-border payments at bis.org

6 See Next-generation monetary and financial system takes shape, based on a tokenised unified ledger: BIS at bis.org

7 See III. Blueprint for the future monetary system: improving the old, enabling the new at bis.org

8 See Project Agora: exploring tokenisation of cross-border payments at bis.org

9 See Project Agorá at bis.org

10 See Project Agorá at bis.org

11 See III. Blueprint for the future monetary system: improving the old, enabling the new at bis.org

12 See Project Agorá: central banks and banking sector embark on major project to explore tokenisation of cross-border payments at bis.org

13 See 10 BIS Innovation Hub project showcase: project Agorá at youtube.com

14 See Project Agorá: a shared programmable platform for wholesale cross-border payments at bis.org

You might be interested in

Cash management

Inside downstream correspondent banking – and why it matters Inside downstream correspondent banking – and why it matters

As regulation and standards evolve, the view of risk linked to downstream correspondent banking relationships is also changing. Deutsche Bank’s Matthew Probershteyn explores this shift in perception – and examines how banks are strengthening both control frameworks and transparency in practice

flow white papers and guides

Digital Money – a perspective on stablecoins, tokenised deposits, and CBDCs Digital Money – a perspective on stablecoins, tokenised deposits, and CBDCs

This new white paper explores the digital money landscape – spanning stablecoins, tokenised deposits and central bank digital currencies – the regulatory and market forces shaping it, and how these changes are impacting financial institutions, corporate treasury and custody models

Trust and securities services

Ready for take-off: scaling digital assets Ready for take-off: scaling digital assets

As digital assets move from proof of concept to application, banks face a number of operational and regulatory challenges. Sabih Behzad, Head of Digital Assets and Currencies Transformation at Deutsche Bank, shares what it takes to scale digital assets responsibly