-

Cash management, Technology

What corporate treasurers should know about cross-border instant payments

10 June 2026

Cross-border and cross-currency instant payments are still in their early days, but the architecture is now being built. What are the recent developments in this space that corporate treasurers should know about? Deutsche Bank’s Michael Knetsch and Prasanna Subramanian explore the new landscape

MINUTES min read

Cross-border instant payments are moving from regional experiments towards a global redesign of payment architecture. As of August 2025, more than 70 countries now operate domestic instant-payment systems,1 and policymakers are increasingly focused on how to connect those rails across borders to meet the goals of the G20 roadmap for faster, cheaper, more transparent and accessible payments.

However, the global market is not converging according to a universal model; it is assembling a new cross-border architecture from multiple regional and global building blocks: bilateral rail interlinking, multilateral interoperability hubs, regional utility platforms, and bank-orchestrated overlay models that use instant domestic last-mile rails on both ends.

This article provides an overview of the different models emerging in the cross-border instant payment space; exploring how each region is moving forward in terms of connectivity and describing how corporate treasurers can benefit.

Why does this matter for corporate treasurers?

For corporate treasurers, instant payments allow for faster money movement, better cash visibility, lower friction and richer data. Consumer-facing corporates can accelerate refunds, merchant settlement and disbursements; marketplaces and platforms can improve seller and gig-economy payouts;2 treasurers can gain real-time visibility of cash positions;3 and multinational finance teams can automate reconciliation more effectively with ISO 20022-structured information and live status events.

So far, however, use cases that require instant payments are often limited to domestic or single currency projects due to the lack of cross-border and cross-currency settlement capabilities. This will change as the cross-border architecture for instant payments builds up.

There is also a strategic upside for corporates in terms of resilience and optionality. A richer cross-border instant ecosystem gives corporates more routing choices: they do not have to rely on a single legacy rail for every use case. Low-value urgent supplier payments, instant consumer refunds, real-time marketplace settlements, local-currency payouts and cross-border collections can increasingly be routed over rails designed for speed, transparency and automation rather than through opaque multi-day chains.

That does not eliminate correspondent banking – but it does give clients a more flexible, intelligent and fit-for-purpose global payments stack. The most important shift is conceptual: cross-border instant payments are no longer just a payments topic. They are becoming a liquidity, embedded payments and FX topic.

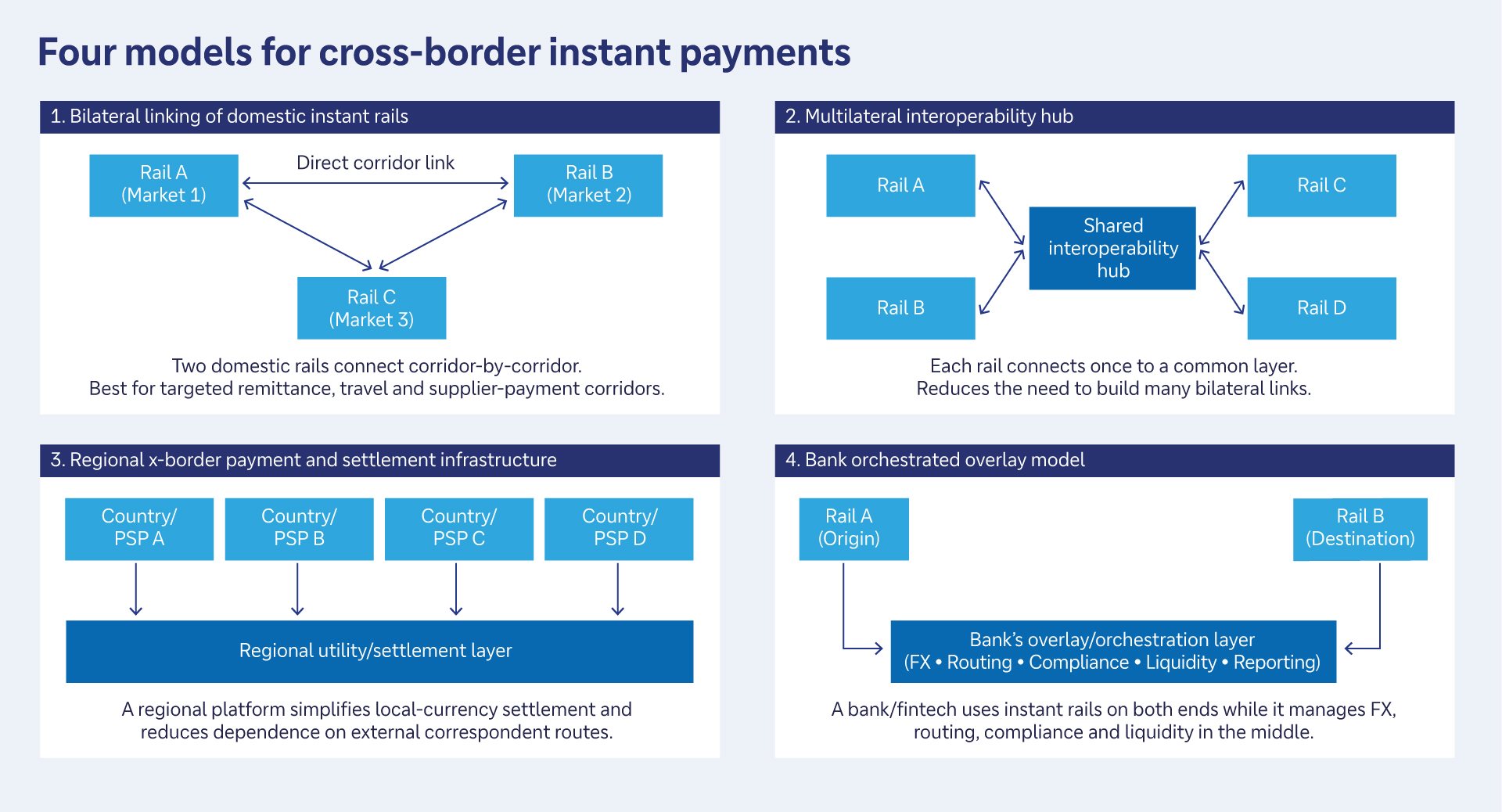

Four models for cross-border instant payments

So what will the new architecture for cross-border payments look like? There are four models evolving as shown in Figure 1.

Figure 1: Four models for cross-border instant payments

Source: Deutsche Bank

- Bilateral interlinking of domestic instant rail

The first model is the most intuitive: connect two domestic fast-payment systems and allow customers or institutions in one market to reach beneficiaries in the other. Asia has pioneered this approach through live bilateral linkages (e.g., PayNow-PromptPay) and QR-based extensions,4 while Europe is now pursuing similar logic by exploring interlinking its TARGET Instant Payment Settlement (TIPS)5 with India’s Unified Payments Interface (UPI) and the Swiss Interbank Clearing Instant Payments system.6 Bilateral links are attractive because they can be launched corridor by corridor and targeted at high-priority flows such as remittances, travel, supplier payments and retail collections. - Multilateral interoperability utilities

The second model is the utility model, where many instant-payment systems connect once to a common interoperability layer rather than building links corridor by corridor. Project Nexus, led by the Bank for International Settlements, is the clearest example. It aims to standardise domestic instant-payment systems so that each operator makes a single connection to the Nexus platform and can then access all other connected systems.7 The logic is powerful: bilateral links are efficient for a handful of corridors, but multilateral schemes reduce the marginal integration cost when many markets need to interoperate. - Regional cross-border payment infrastructures

The third model is less about retail instant rails directly interlinking, and more about regional cross-border infrastructures that simplify local-currency settlement and reduce dependence on correspondent banking. For example, a system called AFAQ connects real-time gross settlement systems in Gulf Cooperation Countries (GCC) to enable real-time processing with same-day settlement finality in GCC currencies.8 - Bank-orchestrated overlay models

The fourth model is the one many global banks and fintechs can pursue immediately: use instant domestic rails on both ends, while the bank or provider orchestrates the cross-border bridge – routing, FX, liquidity and compliance – in the middle. This model is especially relevant in markets where domestic instant rails are already mature but formal inter-country rail connectivity is still developing. It is also the model most closely aligned with how global corporate banks can move now: connecting local capabilities through APIs, account structures, prefunding, FX and real-time reporting rather than waiting for a universal scheme to mature everywhere.9

Instant payments: what is happening by region?

Asia-Pacific: still the global frontrunner

Asia-Pacific (APAC) remains the most advanced region in turning domestic instant rails into cross-border use cases. The Association of Southeast Asian Nations has moved from policy intent to live corridors and formal regional payment-connectivity commitments, while Project Nexus is being jointly implemented by the central banks in India, Malaysia, the Philippines, Singapore and Thailand. The region is also experimenting beyond classic bank-to-bank transfers: cross-border QR, alias-based transfers, local-currency settlement and multilateral interoperability are all active themes. In practice, APAC is showing the rest of the world that instant cross-border does not need to start with wholesale transformation – it can start with retail, small and mid-sized enterprises, travel and platform use cases and then move up the value chain.10

Europe: from domestic instant maturity to outward connectivity

In Europe, instant payments in euros are already operating effectively across multiple borders within the Single Euro Payments Area (SEPA). Since Serbia joined in May 2025, SEPA now covers 41 countries,11 with other countries hoping to join as well. While it is single-currency (the euro), SEPA Instant is still an important live example of cross-border instant payments at scale. Europe’s distinctive move is now to take a well-established instant infrastructure and extend it outward. The European Central Bank says TIPS now has a baseline cross-currency capability, available since October 2025, enabling Swedish and Danish users to pay euro-area beneficiaries in seconds.12 It is also exploring global interlinking through Nexus, India’s UPI and Switzerland’s instant-payments system.13 Likewise, in the UK, the domestic Faster Payment System infrastructure is already enabled to receive cross-border instant payments as ‘Payments Originating Overseas’.14 That makes Europe strategically important: it is no longer just harmonising instant payments within SEPA, but actively examining how the euro area can become part of a broader interoperable instant-payments ecosystem.

“The strategic theme in the Middle East is not just speed, but also regional financial autonomy”

Middle East: regionalisation, local-currency settlement and strategic sovereignty

In the Middle East, cross-border instant payments is less about consumer-facing bilateral request-to-pay (RTP) links and more about regional market infrastructure. AFAQ was built to support real-time cross-border processing in GCC currencies with same-day finality. A system called Buna is aimed at the broader Arab region and beyond, positioning itself as a centralised, compliant and multi-currency cross-border system with a participant base that has now surpassed 100.15 The strategic theme in the Middle East is therefore not just speed, but also regional financial autonomy, lower dependence on external correspondent routes, and stronger local-currency trade settlement.

Africa: building a continental payments spine

Africa’s most important development is the Pan-African Payment and Settlement System. Its proposition is explicit: enable instant and secure cross-border payments in local currencies across Africa, simplify FX complexity, and support trade flows within the African Continental Free Trade Area.16 This is significant because Africa is not merely digitising domestic payments – it is trying to build a continental payment spine that reduces the historical ‘US$ detour’ in intra-African trade.

Latin America: strong domestic rails, early outward expansion

Latin America’s defining feature is the success of domestic schemes such as Pix, and the gradual outward extension of those rails. Banco Central do Brasil describes Pix as a “few-seconds, 24/7 instant-payment” framework with open access and integrated information-and-funds processing.17 In March 2026, Banco Central do Brasil launched ‘Pix no exterior’ in Argentina, allowing Brazilian Pix users to pay merchants in Argentina through QR with automatic FX conversion behind the scenes.18 Latin America is therefore moving toward cross-border instant use cases not through a single regional utility, but by exporting the power of domestic real-time schemes into adjacent corridors.

North America: strong domestic instant rails, cross-border still nascent

North America is the most important reminder that domestic instant scale does not automatically create cross-border instant interoperability. FedNow gives the US a public-sector domestic instant rail operating 24/7/365,19 while The Clearing House’s RTP network offers a private-sector instant rail20 with rich ISO 20022 messaging and an enhanced transaction limit now at US$10m.21 Yet cross-border instant remains comparatively underdeveloped, underscoring that once payments leave domestic rails they still encounter legacy correspondent, FX, compliance and settlement frictions unless a specific inter-country model is in place.

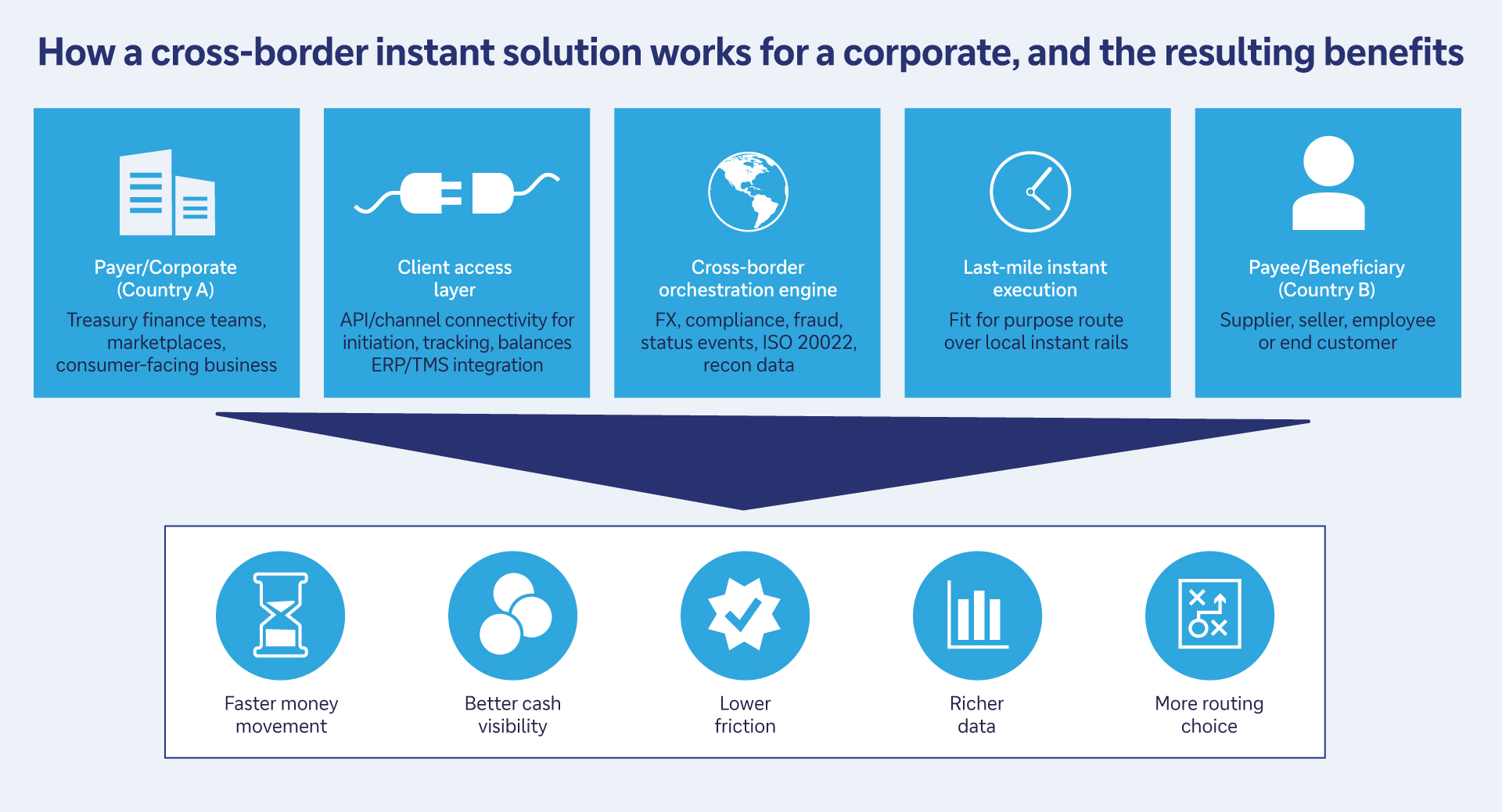

Cross-border instant payments to real-time treasury

For corporate banking, the biggest change is not simply faster payments; it is the move to always-on, multi-rail treasury. Treasurers no longer manage only end-of-day positions and batch cycles – they need intraday and even real-time visibility of balances, receipts, exceptions and liquidity as foundational elements as payments move across borders in real-time.

That is why APIs and data standards matter as much as payment rails themselves: APIs are needed for real-time payment initiation, live tracking, FX, fraud prevention and integration into treasury management systems and enterprise resource planning systems. In terms of data, ISO 20022 gives corporates richer structured data to improve reconciliation, working-capital forecasting and on-behalf-of payment models.22

Figure 2: How a cross-border instant solution works for a corporate, and the resulting benefits

Source: Deutsche Bank

Deutsche Bank’s Instant Cash Reporting (ICR) solution, launched in July 2025, is an example of how real-time multi-bank visibility delivered via a standardised API model over Swift connectivity helps treasurers manage global liquidity when inbound/outbound flows could hit accounts anytime. Spain-based energy company Iberdrola was the first to implement ICR, highlighting that it improved operational efficiency, reduced errors, helped identify unexpected incoming payments and therefore ultimately enhanced financial management.23

Another example is German biotech company BioNTech, which receives real-time account balances and push notifications for credits and debits from Deutsche Bank via APIs, equipping its treasury for a world where cross-border receipts could happen around the clock. “This allows us to have real-time data at every point in time via our standard treasury application,” Dirk Schreiber, Head of Treasury at BioNTech, said in an interview with flow.

The second change is that payments, FX and data are converging into one proposition. Cross-border instant is only commercially useful if companies also get pre-trade FX visibility, straight-through reconciliation, confirmation events, consistent API behaviour and strong fraud controls. The Committee on Payments and Market Infrastructures has repeatedly emphasised that API harmonisation and ISO 20022 data consistency are central to better cross-border outcomes.24

Ultimately, cross-border instant payments are needed to fulfil the promise of a real-time treasury – and the necessary architecture is being built now.

More information on Deutsche Bank’s instant payments offering can be found here: and on API connectivity here.

Sources

1 See Project Nexus: enabling instant cross-border payments at bis.org

2 See Deutsche Bank and Ant International Announce Strategic Partnership to Provide Integrated Cross-Border Payment Solutions to Global Merchants at db.com

3 See How BioNTech masters real-time treasury – Deutsche Bank at flow.db.com

4 See Southeast Asia’s Payment Push at imf.org

5 See TIPS to connect to other fast payment systems globally at ecb.europa.eu

6 See Cross-border payments at ecb.europa.eu

7 See Project Nexus: enabling instant cross-border payments at bis.org

8 See Gulf payments system to execute financial transactions in a real-time basis with low fees, in a secure, safe, and stable ecosystem at gulf-payments.com

9 More information on Deutsche Bank’s instant payments offering can be found here and on API connectivity here

10 See Southeast Asia’s Payment Push at imf.org

11 See The inclusion of Serbia in the SEPA payment schemes’ geographical scope | European Payments Council at europeanpaymentscouncil.eu

12 See Cross-border payments at ecb.europa.eu

13 See Cross-border payments at ecb.europa.eu

14 See Faster Payments Service Principles at wearepay.uk

15 See Transforming cross-border payments at one.buna.co

16 See Connecting Payments. Accelerating Africa’s Trade. at papss.com

17 See what is Pix? at bcb.gov.br

18 See Banco do Brasil lança Pix no exterior at bb.com

19 See Federal Reserve Board - Federal Reserve announces that its new system for instant payments, the FedNow® Service, is now live at federalreserve.gov

20 See Real Time Payments | The Clearing House at theclearinghouse.org

21 See RTP Network $10 Million Transaction Limit Spurs High-Value Payment Surge | The Clearing House at theclearinghouse.org

22 See ISO 20022 for corporates at swift.com

23 See Deutsche Bank launches Instant Cash Reporting – Corporates and Institutions at corporates.db.com

24See Harmonised ISO 20022 data requirements for enhancing cross-border payments – original report at bis.org

You might be interested in

Cash management

How the EU Instant Payment Regulation impacts corporate treasurers How the EU Instant Payment Regulation impacts corporate treasurers

Following the introduction of the EU Instant Payment Regulation, the volume of real-time payments is increasing. For corporate treasurers this means that they need to review liquidity management, account statement processing, and fraud prevention. But instant payments also create new opportunities, explains Deutsche Bank’s Christof Hofmann

flow case studies, Cash management, Technology

How BioNTech masters real-time treasury How BioNTech masters real-time treasury

Innovation and speed have been part of BioNTech’s DNA ever since its formation 16 years ago. Back in 2020, it took the German biotech company less than a year to develop a vaccine against Covid-19. flow’s Desirée Buchholz talked to Dirk Schreiber, BioNTech’s Head of Treasury, on why real-time treasury is key for him – and how APIs help to achieve this goal

flow case studies, Cash Management

Siemens Treasury: leading innovation in real-time payments Siemens Treasury: leading innovation in real-time payments

Siemens’ belief in the potential of new technology is reflected in the company’s continued Corporate Treasury evolution. Heiko Nix, Siemens’ Global Head of Cash Management and Payments, updates treasury journalist Graham Buck on the ongoing journey