-

Macro and markets, Trade finance and lending

Germany update: breaking from the brake

One year on from Germany’s radical loosening of the so-called debt brake that released €500bn to enhance defence capabilities and modernise infrastructure, all eyes are on how the borrowing is translating into actual investment and economic growth. flow’s Clarissa Dann provides an update, drawing on Deutsche Bank Research insights

MINUTES min read

When Germany reformed its balanced budget amendment – aka the ‘debt brake’ – on 21 March 2025 and presented a massive debt-financed multi-year public spending programme a few months later, the policy shift heralded an ambitious public spending agenda for the period 2025–29.1

A core objective was to modernise the ageing public infrastructure and bolster the country’s defence capabilities. Already – as the New York Times reported on 3 March Germany has allocated €108.2bn to military spending for 2026, far exceeding the UK’s and France’s defence budgets of around €72bn and €60bn respectively.2

As explained by the country’s Federal Ministry of Finance in February 2022, the debt brake, introduced by the Merkel government in 2009, had been put in place to “lower Germany’s public debt-to-GDP ratios which had increased sharply following the 2008-09 financial crisis, and to take account of the changed institutional framework conditions at the European level”.3

Historic reform

On 25 June 2025, the newly elected government of Friedrich Merz announced the ‘Big Berlin Bill’. This package of measures, observed Deutsche Bank Research Germany economists in their commentary next day, was “a large step towards implementing the fiscal regime shift that it initiated with the historic reform of the debt brake”.4 It comprised:

- A €500bn special purpose vehicle for infrastructure investment, climate protection and the green transformation of the economy over a 12-year period. Of this figure, €100bn has been allocated to the federal states.

- A reform of the debt brake to exempt any defence spending over and above 1% of GDP, effectively permitting open-ended borrowing for defence. The wider goal here is to raise the NATO quota to 3.5% of GDP, as agreed at the NATO Summit in The Hague on 25 June 2025.5

- A reform of the debt brake at the Länder (federal state) level to raise their net borrowing cap from 0% to 0.35% of GDP, as at the federal level.

The Deutsche Bank Research team pointed out that the government planned to spend more than €200bn on defence and infrastructure in 2025, with much of this being debt financed via the two off-budget funds for defence and infrastructure, as well as the debt-brake exemption for defence and other external security-related spending. Overall, the analysts added, the government planned “net borrowing of €143bn or 3.3% of GDP in 2025 – a sharp increase of two percentage points of GDP from 2024.

Opportunities for corporates and banks

The spending plan presents significant opportunities for private sector corporates. As flow’s Desirée Buchholz reported in ‘Germany at the crossroads’ (May 2025), “The fiscal investment package offers great opportunities for German companies, but also for international corporates – most obviously for those in the defence sector, which hope to benefit from public orders to ramp up Germany’s defence capabilities and military production.

“We see existing defence players increasing capacity”

Other corporates set to benefit are those in the fields of energy, transport infrastructure, telecoms and IT equipment, engineering, project management, etc, with commercial bank lending supported by development bank and export credit agency guarantees.

This is already being seen in defence spending and order uptick says Hauke Burkhardt, Head of Bund and Public Sector Coverage & Advisory at Deutsche Bank. “The larger quantities mean that supply chains need to be built out, so we see existing defence players increasing capacity.” He adds that civil industry suppliers have yet to enter the supply chain – the process requires accreditation and navigation of public procurement rules – which is currently set for simplification.6

Turning to infrastructure, he notes “we still need to see more activity” and points out that “the €100bn going to the federal states (over 12 years) still needs to be finalised. It is important to increase speed now, starting with easing approval requirements”.

Commenting in The Banker on 25 March 2025 on the fiscal policy shift, economist and former Bank of England Monetary Policy Committee member Tomasz Wieladek reflected, “Germany’s decision to shift its fiscal policy will permanently alter the economic destiny of the continent, with the European banking sector being one of the largest beneficiaries.”

He explained, “With a €1trn public investment package, equivalent to 23.3% of German GDP, Berlin is not committing just to defence spending – half of the package will be spent on public infrastructure to revive the supply side of its economy. The new government will accelerate the German planning system and lower legal restrictions, giving the country’s potential growth rate a significant uplift.”7

Unpacking the ‘Big Berlin Bill’ stimulus

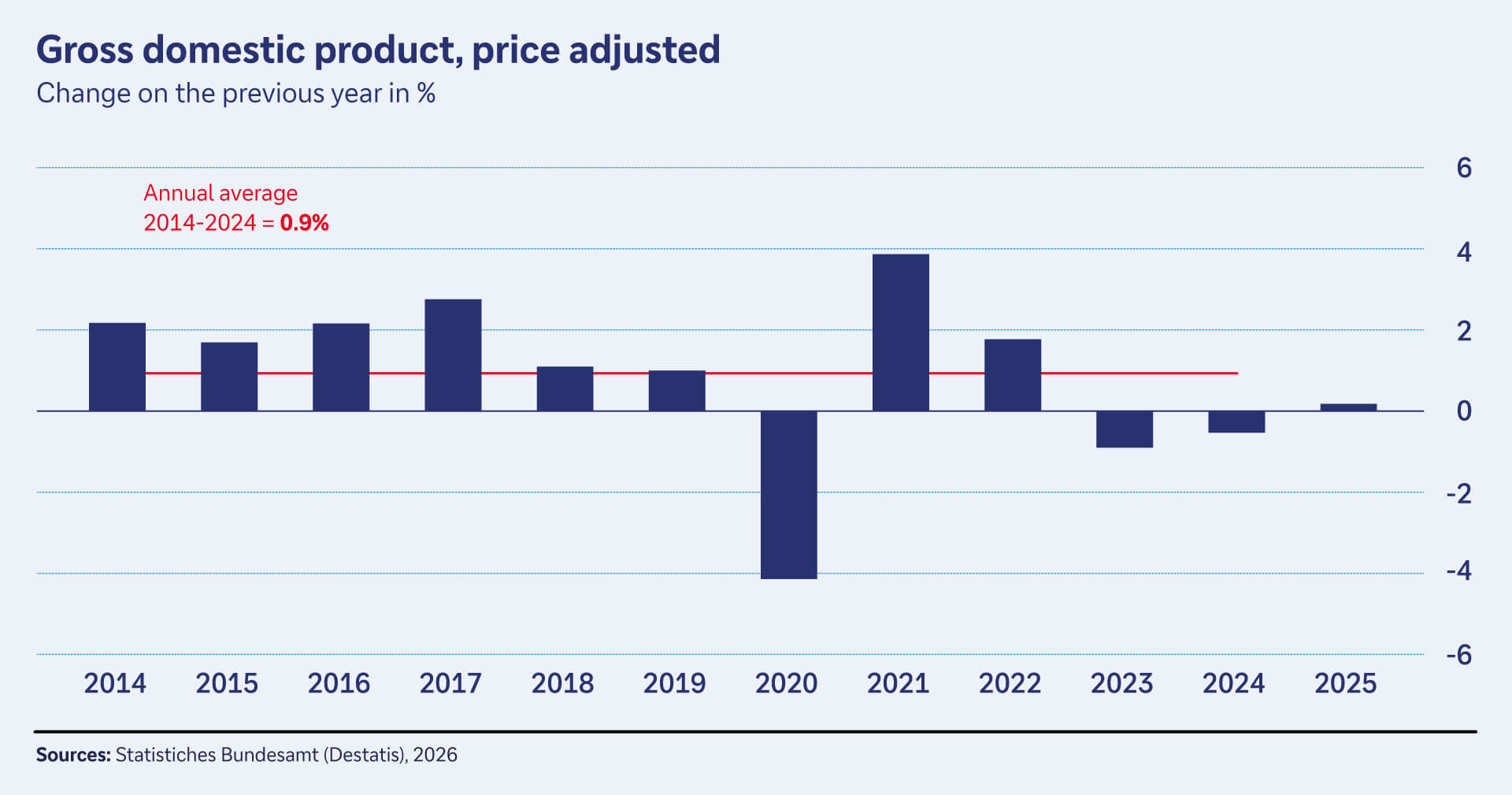

The stimulus plan has made an impact in the past 12 months, albeit more slowly than anticipated. “After two years of recession, the German economy edged back into growth. The growth is primarily attributable to increased household consumption and government expenditure,” said Ruth Brand, President of the Federal Statistical Office on 15 January 2026.8

Figure 1: German GDP uptick

Source: Statistisches Bundesamt (Destatis) 2026

The statistics also underline the point that Deutsche Bank Research economist Sebastian Becker made a month earlier on 15 December that “the ramp-up in defence and public investment spending is proceeding more slowly than the government had hoped for”.9

Furthermore, exports had declined, with the Federal Statistical Office reporting “strong headwinds owing to higher US tariffs, the appreciation of the euro and increased competition from China”. It added, “investment remained weak, with fixed capital formation in machinery and equipment and in construction down on the previous year.”

The question for 2026, therefore, is how much of the new borrowing gets used for higher public consumption rather than productive infrastructure investments or the promised defence spending. As Becker put it, “The federal government is confronted with high consolidation needs in its core budget for the period 2027–29. This is because rising fixed expenditures, such as subsidies for the statutory pension system or interest payments, will increasingly strain the core budget.”

“The continued increases in defence and investment are likely to be large enough to drive the general government deficit noticeably higher”

Outlook for fiscal regime progress

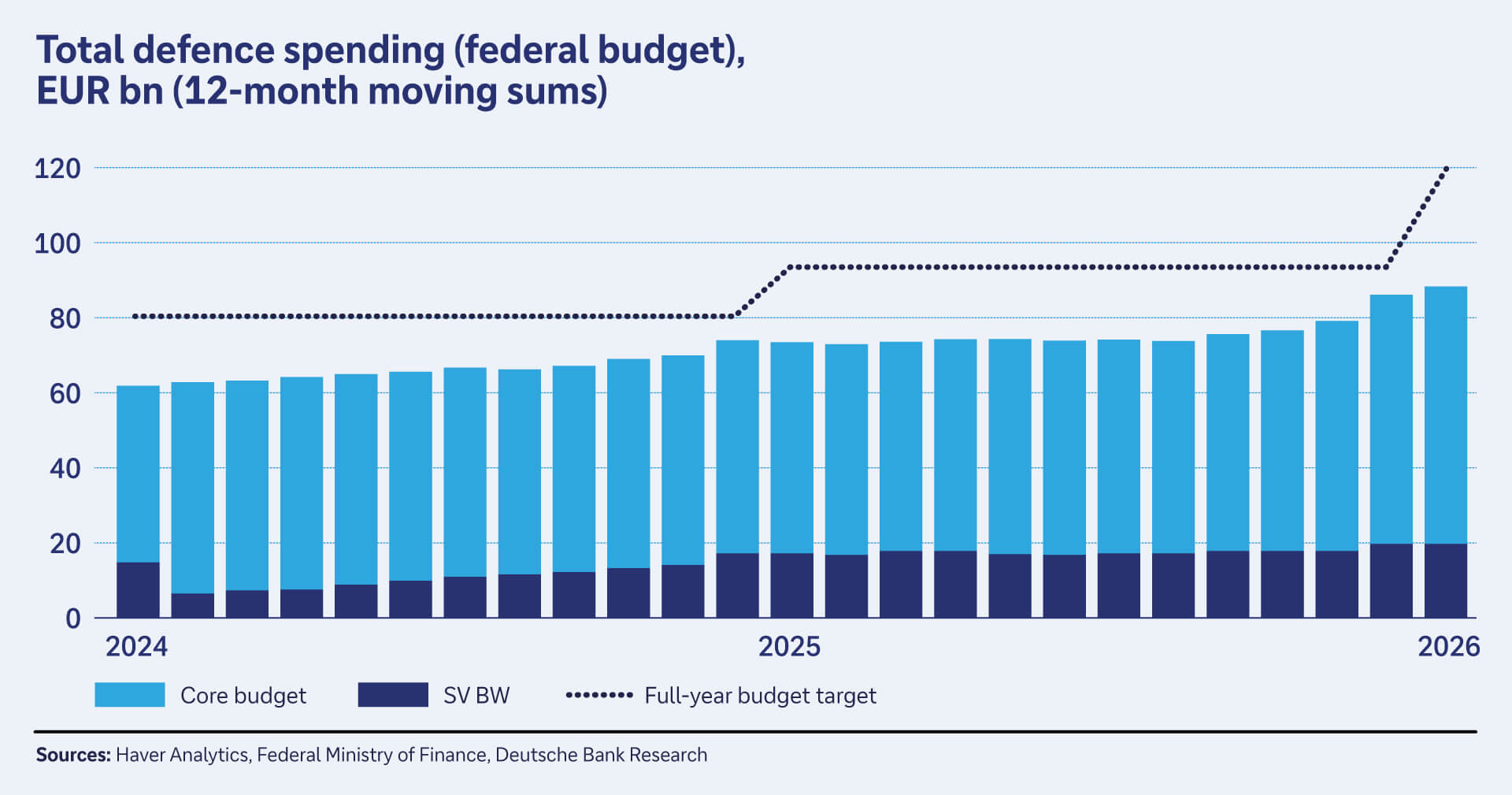

On 23 February, Deutsche Bank’s Becker reviewed the January 2026 data and confirmed that the fiscal regime shift had “continued to progress” into the new year: “Defence and investment expenditures, and consequently the financial deficit, have noticeably expanded in January (compared to the previous year’s figures).” See Figure 2 (SV BW denotes Federal Armed Forces Fund).

Figure 2: Defence spending is rising, but lags behind ambitious targets

Source: Haver Analytics, Federal Ministry of Finance, Deutsche Bank Research

While ongoing non-financial hurdles such as planning, approval and implementation delays would suggest that a full achievement of the Merz government’s ambitious expenditure targets for 2026 looks unlikely, and the government deficit will continue to widen. “The continued increases in defence and investment are likely to be large enough to drive the general government deficit (federal government, states, municipalities, social security funds) noticeably higher, from 2.4% of GDP in 2025 to a forecast 3.5% of GDP in 2026,” Becker concluded.

Deutsche Bank Research reports referenced

The Big Berlin Bill: lifting our growth forecasts for 2025 and 2026, 26 June 2025, by Robin Winkler (Chief Economist, Germany), Marc Schattenberg and Sebastian Becker, (Senior Economists, Germany) at Deutsche Bank Research.

Fiscal outlook 2026+: unpacking Germany’s big spending play, 15 December 2025, by Sebastian Becker, Senior Economist, Deutsche Bank Research

Tracking Germany’s fiscal regime shift: with some momentum into 2026, 23 February 2026, by Sebastian Becker, Senior Economist, Deutsche Bank Research

Sources

1 See What does German debt brake reform mean for Europe? at uk.investing.com

2 See See Germany Is Pumping Up Its Military Spending. That Worries Its Neighbors at nytimes.com

3 See Germany’s Federal Debt Rule (Debt Brake) at bundesfinanzministerium.de

4 The Big Berlin Bill: lifting our growth forecasts for 2025 and 2026, Deutsche Bank Research, 26 June 2025

5 See NATO concludes historic Summit in The Hague | NATO News at nato.int

6 See Germany to simplify defence procurement | White & Case LLP at whitecase.com

7 See Why Germany’s fiscal shift will make European banks great again - The Banker at thebanker.com

8 See Gross domestic product up 0.2% in 2025 - German Federal Statistical Office at destatis.dev

9 Fiscal outlook 2026+ Unpacking Germany’s big spending plan, Deutsche Bank Research 15 December 2025

You might be interested in

Macro and markets, Trade finance and lending

The world outlook 2026 – never a dull moment The world outlook 2026 – never a dull moment

Drawing on the Deutsche Bank Research annual next-year World Outlook, flow looks forward to a year of cautious optimism, with growth accelerated by AI adoption, clearer trade strategies, fiscal stimuli, and investment in security and infrastructure

Macro and markets, Trade finance and lending {icon-book}

Germany at the crossroads Germany at the crossroads

With a GDP of €4.66trn, Germany remains the third biggest economy in the world behind the US and China – but the country is facing secular stagnation. flow’s Desirée Buchholz explores the most pressing tasks for the new government and how corporates could benefit from the public investment package

flow case studies, Cash Management

Siemens Treasury: leading innovation in real-time payments Siemens Treasury: leading innovation in real-time payments

Siemens’ belief in the potential of new technology is reflected in the company’s continued Corporate Treasury evolution. Heiko Nix, Siemens’ Global Head of Cash Management and Payments, updates treasury journalist Graham Buck on the ongoing journey