-

Macro and markets, Trade finance and lending

Macro outlook: when AI meets geopolitics

24 June 2026

Artificial intelligence (AI) and the fallout from the Middle East conflict are the two forces currently defining the global economy. Drawing on Deutsche Bank Research’s mid-year outlook, flow reports on how this is impacting GDP growth in different regions

MINUTES min read

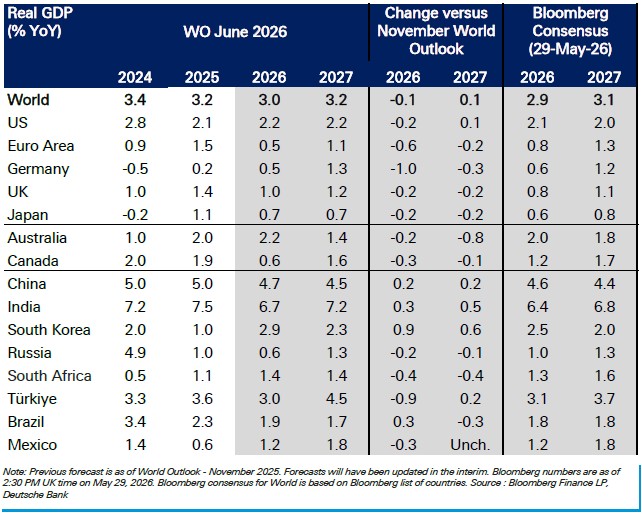

The energy shock brought about by the war in the Middle East has only slightly trimmed global GDP growth projections for 2026. Deutsche Bank Research now projects 3% growth compared to 3.1% in November 2025. Unsurprisingly, however, inflation is rising more sharply than anticipated seven months ago. Global headline CPI for 2026 is now expected to be 3.8%, versus the 3.1% projected in November 2025.

Renewed inflationary pressure is also shifting monetary policy expectations, with central banks in the euro area and much of Asia now expected to raise rates this year. The Fed, by contrast, is expected to remain on hold, although persistent inflation could still force it to tighten its monetary policy.

The US remains resilient, Europe is under pressure and China is stabilising: these are the central messages of Deutsche Bank Research’s mid-year World Outlook, published on 1 June. While the report pre-dates the 14 June announcement of a US-Iran framework agreement to end hostilities, its baseline scenario had already assumed that a deal would be reached in June.

Figure 1: Deutsche Bank GDP growth forecasts

Source: Bloomberg Finance LP, Deutsche Bank

Compared to the outlook published seven months ago, the team remains cautiously optimistic for the world economy. Yet, drawing on an analogy from history, Deutsche Bank Research’s Jim Reid and David Folkerts-Landau describe the uncertainty the economy currently faces: “The world economy is grappling with a complex interplay of persistent AI-driven optimism and the disruptive force of the Middle East conflict, making it feel like 1999 meets 1990, but hopefully not 1973.”

In 1990, the Gulf War led to a sharp but short-lived spike in crude oil prices. By contrast, 1973 evokes the outbreak of the Yom Kippur War and the Arab oil embargo that followed – a crisis that ushered in stagflation and a new awareness of energy vulnerability. 1999 was a landmark year for technology, introducing breakthroughs in computing hardware and early wireless internet – but also one where the Dotcom bubble reached its peak.

“It feels like 1999 meets 1990, but hopefully not 1973”

27 years on and the world again finds itself at geopolitical and technological crossroads, the Deutsche Bank Research team argues. “Geopolitical volatility has become less a temporary disruption and more a structural characteristic of the international system”, writes Helen Belopolsky, Global Head of Geopolitical Research and team. “We should expect more geopolitical shifts in the second half of 2026.”

New political order in the Middle East

Regarding the Middle East conflict, the team points to the fact that the war shattered the previous geopolitical equilibrium creating a new, unpredictable reality – as illustrated by the United Arab Emirates decision to leave the Organisation of the Petroleum Exporting Countries in May 2026.

Post-conflict normalisation and economic recovery will be a lengthy process, likely taking months, Belopolsky believes. “Rebuilding critical infrastructure like Qatar’s Ras Laffan gas field and restoring confidence for shipping through the Strait of Hormuz will take considerable time, with knock-on effects likely lasting well into the second half of 2026.”

The conflict somehow overshadowed what was expected to be the main narrative of 2026: the rapid investment and adoption of AI. However, once the war ends, the debate around how AI will reshape the world will intensify again, the economists stress. “So, expect the tech fever and its implications to intensify.”

How AI is impacting the US economy

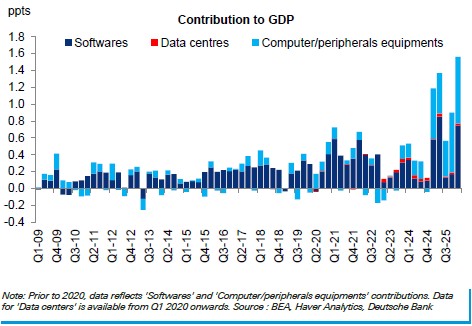

The US economy remains the standout among major developed economies. Chief US Economist Matthew Luzzetti and team expect US growth of 2.2% in 2026, a slight downgrade but still a notably strong pace given the external shocks. Fiscal support, easing financial conditions and continued AI-related investment are helping offset the drag from higher oil prices on household spending.

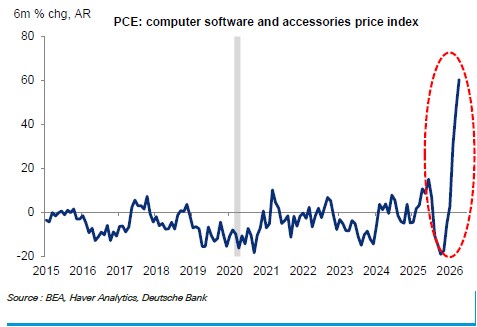

AI is seen as a transformative force that is likely to produce sustainably stronger productivity growth over the medium term. “However, in the near-term at least, evidence has emerged that the AI investment boom is buttressing demand and lifting inflationary pressures,” writes Luzzetti. While the team sees limited evidence that AI has meaningfully weakened aggregate labour market statistics so far, this could change in the future and “potentially act as a meaningful source of disinflationary pressures”.

Figure 2: AI has been an important driver of capex in recent quarters

Source: BEA, Haver Analytics, Deutsche Bank

Figure 3: AI-related demand likely driving some components of inflation higher

Source: BEA, Haver Analytics, Deutsche Bank

Germany waits for fiscal stimulus

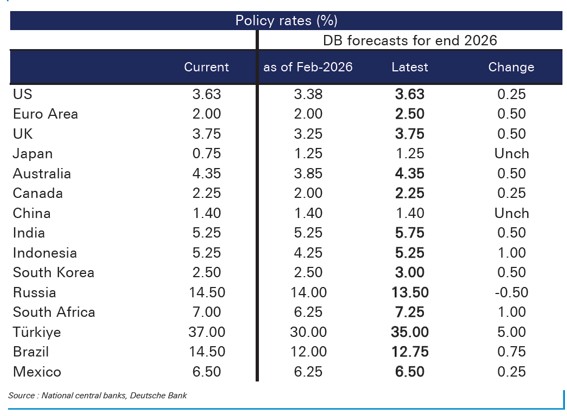

In the euro area, the picture is more fragile. The growth projection for 2026 has been cut sharply to just 0.5%, reflecting the region’s vulnerability to higher energy costs and weaker demand for exports. At the same time, inflation is moving back in the wrong direction: headline HICP is projected at 3.1% this year, well above earlier expectations.

That combination is pushing the ECB toward what the report terms “measured” tightening, with 50 basis points of rate hikes expected to take the deposit rate to 2.5% in summer 2026. “We see far higher chances of European success at the football World Cup across the Atlantic than the continent outperforming economically over the summer,” writes Chief European Economist Mark Wall.

Germany sits at the heart of that European dilemma. Europe’s largest economy is expected to grow by just 0.5% in 2026, with inflation at around 3%. Higher energy costs, fragile private consumption and structurally weak competitiveness are weighing on momentum. Strongest tailwinds will come from fiscal spending. In June 2025, the government set up a €500bn special purpose vehicle for infrastructure investment, climate protection and the green transformation of the economy over a 12-year period. This is expected to gain further traction in the second half of the year, states Chief Economist Germany, Robin Winkler.

Figure 4: Fiscal-driven order strength is set to support industrial activity

Source: Federal Statistical Office, Deutsche Bank Research

Mixed picture in Asia

Asia, meanwhile, is not just telling one story. China is expected to grow by 4.7% in 2026, down slightly from earlier projections but still relatively solid. Strong trade performance is cushioning softer domestic demand, while reflation is beginning to take hold. Consumer inflation is expected to average 1.6%, while producer prices are strengthening more noticeably, helped by higher oil prices and AI-related supply pressures.

India still stands out as one of the fastest-growing major economies, but here too the tone has become more cautious. Deutsche Bank Research now forecasts growth of 6.7% for FY27, down from a pre-conflict expectation of 7.5%, as higher oil prices and weather-related risks weigh on the outlook. CPI inflation is expected to move closer to 5%, prompting a shift in monetary policy expectations.

Figure 5: Hawkish shift in central bank expectations following Iran war

Source: National central banks, Deutsche Bank

Japan may be the clearest example of how sharply the energy shock has changed the macro narrative. Growth is now forecast at just 0.7% in 2026, while inflation has been revised materially higher. Deutsche Bank Research expects underlying inflation to accelerate meaningfully, with core-core CPI rising toward 3.5% in early 2027.

That is forcing a more hawkish policy view: the Bank of Japan is now expected to tighten more aggressively, with the policy rate projected to reach 1.75% by April 2027. For years, Japan represented the exception in global monetary policy. Now it is becoming part of the broader story of inflation persistence and policy normalisation – a shift that matters for funding markets, yen dynamics and regional trade flows alike.

Deutsche Bank Research reports referenced

World Outlook: 1999 meets 1990 by Jim Reid, Global Head of Macro and Thematic Research, and David Folkerts-Landau, Group Chief Economist and Global Head of Research, Deutsche Bank Research (1 November 2026)

You might be interested in

Macro and markets, Trade finance and lending

The world outlook 2026 – never a dull moment The world outlook 2026 – never a dull moment

Drawing on the Deutsche Bank Research annual next-year World Outlook, flow looks forward to a year of cautious optimism, with growth accelerated by AI adoption, clearer trade strategies, fiscal stimuli, and investment in security and infrastructure

Trade finance and lending, Macro and markets

What next for global energy? What next for global energy?

With a negotiated settlement to end the war in Iran not as yet confirmed, what does this mean for global trade with energy prices at current levels? flow’s Clarissa Dann examines insights from Deutsche Bank Research and key international agencies and reflects on what this means for trade finance demand

Macro and markets, Trade finance and lending

Germany update: breaking from the brake Germany update: breaking from the brake

One year on from Germany’s radical loosening of the so-called debt brake that released €500bn to enhance defence capabilities and modernise infrastructure, all eyes are on how the borrowing is translating into actual investment and economic growth. flow’s Clarissa Dann provides an update, drawing on Deutsche Bank Research insights.