-

Trade finance and lending, Macro and markets

Europe’s energy stress test

25 March 2026

How will this latest Iran oil shock impact the global economy, and what does this mean for ramping up Europe’s competitiveness? flow’s Clarissa Dann shares geopolitical insights from expert speakers at the 3–5 March 2026 BAFT Europe Forum

MINUTES min read

When BAFT (Bankers Association for Finance and Trade) President & CEO Tod Burwell welcomed more than 400 delegates to the 2026 Europe Forum, nobody could have foreseen what would unfold in the Middle East and the resulting impact on energy prices and cross-border trade.

While he had invited Deutsche Bank’s Head of Corporate Bank and Investment Bank and Management Board member, Fabrizio Campelli, for a fireside opening discussion some weeks ago on European competitiveness, the Iran shock had rearranged the agenda and created a new urgency to some of the talking points.

Gulf shock

“The events at the weekend did trigger a geopolitical shock that you normally see transmitted into the rest of the market when it affects certain things markets became very sensitive to,” opened Campelli. These, he explained, are “energy prices, inflation risk, trade and financial implications”.

He reminded delegates of how economic uncertainty impacts GDP, citing Deutsche Bank Research analysis. The team had published Iran shock: key transmission channels on 3 March where they share, “Our empirical estimates suggest that if the current increase in political uncertainty were to persist for a full year, it could reduce Euro Area GDP growth by 0.25%.”

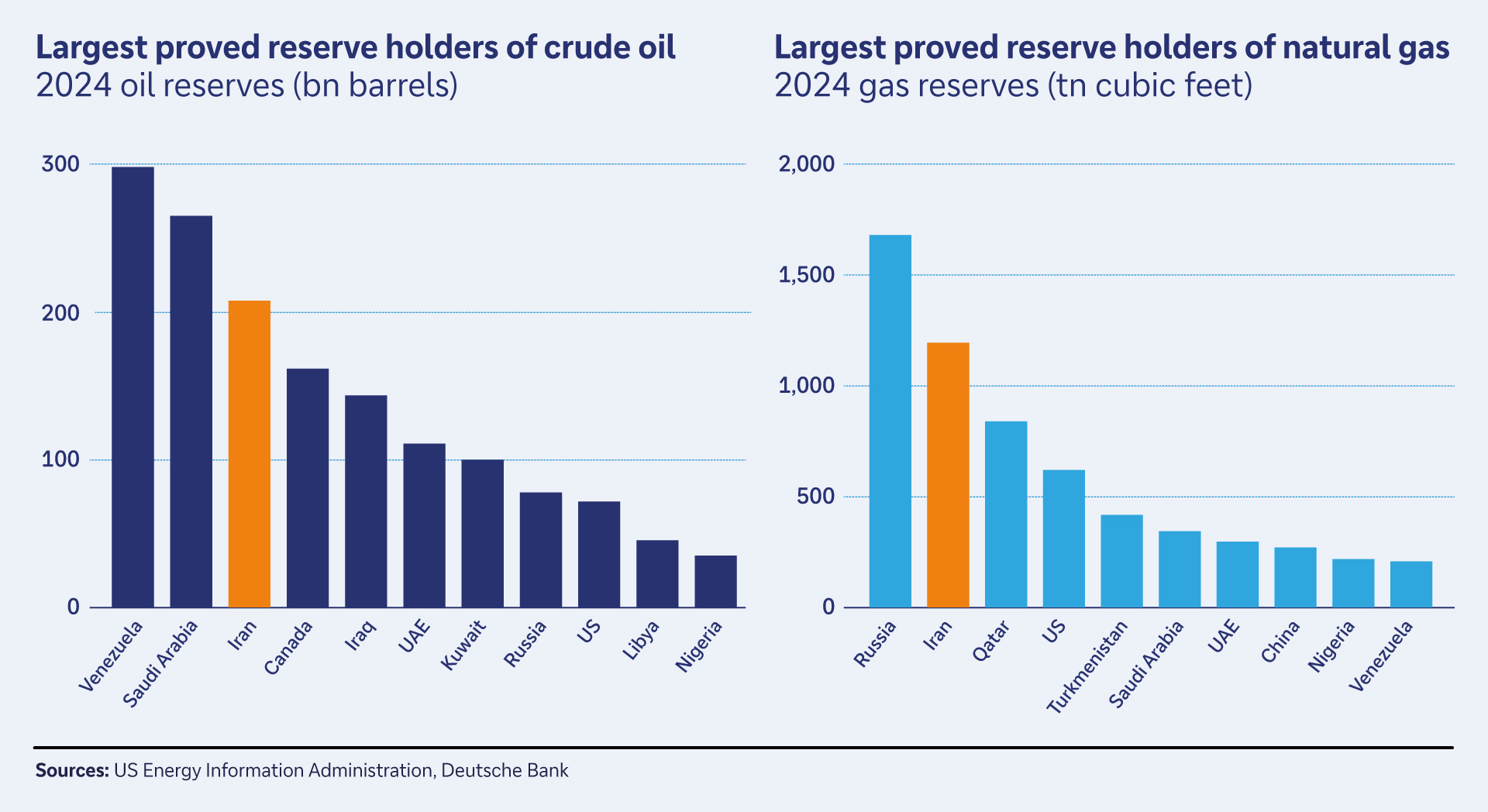

The next question on everyone’s lips involves oil and what changes in energy prices will do to inflation. Iran is a top three holder of crude and natural gas, which means, according to Deutsche Bank Research, that “the impact on the commodities markets will reverberate beyond the immediate disruptions to the oil trade”.1

By 4 March crude oil had surged past US$80 a barrel (bbl), and natural gas past EUR50 per MWh following Qatar’s suspension of LNG production and continued a rapid upward trajectory. Oil tankers are backing up at the Hormuz Strait awaiting safe passage, and many shipping lines have suspended Suez Canal transits – see our 2024 flow article, Trade’s choking hazards, as a reminder of these trade pinch points.

Figure 1: Iran is a top three holder of crude and natural gas

Source: US Energy Information Administration, Deutsche Bank

“People are watching to see how long this crisis will last and how disruptive it will be,” continued Campelli, who pointed out that given much of the oil stuck at Hormuz is China-bound, all of this will doubtless become part of the discussions at the (now delayed) US-China summit. Burwell added, “Every disruption of this nature really tests the resilience of the market, of trade in particular, and how the economy recovers.”

On 9 March, a few days after the BAFT Europe Forum, Jim Reid, Deutsche Bank’s Head of Macro and Thematic Research, went on to explain in a client note the differences between the past two Iran-related oil shocks and the current one. “In the late 1970s, expectations were poorly anchored and the second oil shock helped ignite a wage-price spiral that required aggressive monetary tightening. Today by contrast, expectations remain relatively anchored and the global economy is less sensitive to energy shocks than half a century ago.”

However he noted, “Central banks will want to make sure these expectations don’t build if energy prices stay elevated for a period of time. If so expect them to err on the hawkish side to maintain hard fought inflationary credibility.”

Europe in the slow lane

Rising energy prices have made European competitiveness even more of a key topic than when Campelli discussed this six months ago with Dr Rebecca Harding at Sibos Frankfurt 2025.

He reminded BAFT delegates how the bloc’s industrial policy had not exactly been evident but was very strong in China. “Supply chain vulnerabilities have put a lot of stress into the European model,” he reflected, and observed that European supply chains were “built on expectations of constant availability”. Quite apart from labour shortages, regulatory complexity and the compounding issue of FX impact on tariffs, Europe’s underlying problem is one of fragmentation and dependencies that create inherent weakness.

“Europe was designed to be open, it was designed to trade and interact with the rest of the world on an open basis,” said Campelli. Instead, he continued, “we created dependencies”. These included Russia for cheap hydrocarbons, China for growth markets, and the US for defence and, arguably, technology. Since the global financial crisis of 2008/9 and the sovereign debt crisis of the early 2010s, Europe focused on austerity, explained Campelli. This “reduced investment needed in infrastructure, therefore productivity lagged” and he sees an opportunity to improve this.

The second issue, he said, is one of trade competitiveness. Europe has competed by keeping wages low to the point that “the average European earns less than the average American”. But, he pointed out, attempting competitiveness by reducing the standard of living of one’s population “can catch up with you”.

The third issue – something that was flagged in the 2024 Draghi report – is the failure of Europe to use its “secret weapon” and operate as a single market: “Europe has focussed on external competitiveness and not realised we were building a lot of barriers within the market itself”.

Over the past five years, while Europe’s GDP only grew by 7%, that of the US and China managed 15% and 30% respectively. This, he said, can be explained by all these factors – some structural, some very contextual and some by decisions made during the past 12–15 years.

Left: Fabrizio Campelli, Head of Corporate Bank and Investment Bank and Management Board member, Deutsche Bank. Right: Tod Burwell, President & CEO, BAFT. Image: © BAFT

Unlocking potential

Burwell added that in recent years more expenditure had been seen around defence and clean energy and asked Campelli what more the public and private sectors could be doing.

“It ultimately comes down to where the resources are going to come from. We always speak of three blocks of issues that, if addressed first, could really unlock a lot of potential for Europe.” These, he said, are:

Energy. “Europe still pays too much for its energy – it imported the equivalent in fossil fuels around 2.1% of its GDP.” But Europe is getting smarter at contract negotiation. He added that the ability to transmit energy in Europe was critical, as “sometimes we have a lot of energy in the North and not enough in the South”. The EU’s €584bn grid plan for a full network of interconnected and transmission lines across Europe “could be a major infrastructure improvement”.2

Innovation. “There are 60% more patent applications in the US compared to Europe and there is twice as much research and development capital.” In addition, the US has shifted from different industries in each of the past two decades – auto and pharma in the 2000s, hardware and software in the 2010s, and from 2020 “it’s all digital services”. In contrast the top three spenders on R&D in Europe are all auto firms and this has not changed. Europe suffers from a “static, non-dynamic approach to innovation, and that translates into the fact that only four out of the top 50 tech companies in the world are European”.

Single market. Campelli circled back to Draghi’s point about Europe’s internal barriers – the IMF says that trading merchandise goods within the EU faces barriers equivalent to a 45% tariff, and trading financial services equivalent to a 110% tariff.3 The other issue is the logistics of getting agreement from 27 countries representing four million people and arriving at good decisions. He sees the Capital Markets Union as a real enabler to unlock capital that can be used to create incentives or spent and deployed.

Driving progress

Some of these themes were reprised on the final day of the conference in the session ‘Economic and Geopolitical Outlook - Draghi Report & EU/UK Competitiveness Agenda’. Reflecting on what the panel agreed was a “multi-speed eurozone which not everyone is a member of”, one speaker said that “there is definitely a way of creating structures within the EU to drive forward progress”, such as the concept of a legal framework that allows companies to act under one EU framework rather than being subject to individual rules and legislation. But he warned this could layer even more complexity than already exists today.

As for access to Europe’s trillions in savings, a third of which sits in cash, another speaker thought this could be put to better use. All agreed the elephant in the room was that the capital rich member states such as Ireland and Luxembourg “don’t really want to cede supervisory powers to ESMA in Paris”. And each country has a very different approach to pensions and savings. Creating momentum at European scale to leverage those savings was clearly going to be less than straightforward.

Will fear of missing out drive Europe to consensus? This panel agreed that “wait and see” was all that was possible for now until the outcome of the events in the Middle East became clearer.

The 2026 BAFT Europe Forum took place from 3–5 March 2026 in London

Sources

1 See Iran, its politics, economy and impact (4 March 2026) at dbresearch.com

2 See European grids - European Commission at energy.ec.europa.eu

3 See Europe's Choice: Policies for Growth and Resilience at imf.org

You might be interested in

Trade finance and lending, Opinion

After Draghi: what’s next for Europe’s economy? After Draghi: what’s next for Europe’s economy?

Competitiveness, resilience or preparedness – the big imponderables for European trade in 2026. Independent trade economist Dr Rebecca Harding explains why diverse and resilient supply chains are key – and how these should be financed

Macro and markets, Trade finance and lending

Germany update: breaking from the brake Germany update: breaking from the brake

One year on from Germany’s radical loosening of the so-called debt brake that released €500bn to enhance defence capabilities and modernise infrastructure, all eyes are on how the borrowing is translating into actual investment and economic growth. flow’s Clarissa Dann provides an update, drawing on Deutsche Bank Research insights.

Macro and markets, Trade finance and lending

The world outlook 2026 – never a dull moment The world outlook 2026 – never a dull moment

Drawing on the Deutsche Bank Research annual next-year World Outlook, flow looks forward to a year of cautious optimism, with growth accelerated by AI adoption, clearer trade strategies, fiscal stimuli, and investment in security and infrastructure