-

Trust and securities services

Shifting gears

03 June 2026

A tipping point for the tokenisation of structured products and securities, enabled by issuer and investor services, might finally be upon us predicts Deutsche Bank’s Paul Maley. Speaking to Janet Du Chenne, he makes clear that client voices and market shifts are pushing the industry toward a more unified model

MINUTES min read

flow’s 2021 ‘Pole position for growth article’ introduces Paul Maley, who set out on a career in automotive engineering in the late 1990s but was scooped up by Deutsche Bank in his final year of study. His methodical approach to bringing components together was sought in complex banking environments.

Over the next two decades, stints at the Investment Bank and the Corporate Bank (the transaction banking hub) helped him identify how the next generation of financial services would build on new customer services originating in the post-trade world such as custody, safekeeping and asset servicing – resilient, cycle-proof and touching every part of the bank.

In 2025, Trust and Agency Services also became part of that story, and Maley was asked to manage the unified Trust and Securities Services (TSS) platform. He meets me from the bank’s New York office to expand on how the function engages with issuers and investors around the world.

Bridging the value chain

At one stage, the securities services and trust and agency functions were combined, but were then made distinct businesses during Deutsche Bank’s overall restructuring in 2019, and then brought back together again last year. Maley explains the rationale: “Whether you look at issuers or investors, they’re part of one value chain. It’s issuer services, or trust and agency services, for the primary creation of new securities, the securitisation of those products, depository receipts and listing of those assets, and then the secondary market story at which point the owner of the underlying assets needs investor services such as asset servicing, tax processing and implementing corporate actions.”

Beyond factory specs

The integrated business has a notable feature: it operates on both the private and public sides of Deutsche Bank. Virtual ‘Chinese walls’ separate these sides to prevent misuse of material non-public information and require segregated office space, where assets are created, structured and listed (by issuers), which is bifurcated from the custody and safe keeping of those assets. An integrated TSS business makes it a conduit that bridges both private and public sides to service the whole asset lifecycle, while maintaining segregation, and servicing clients who themselves operate on both sides.

Maley explains: “On the private side of the wall, in our issuer services group, we are dealing directly with the Investment Bank and Capital Markets team, the M&A team, the Debt Capital Markets team, and private side components in structured finance within Fixed Income and Currencies (FIC). Whether those clients need an escrow partner, a loan agency partner, or any form of agent bank relationship; we’re the glue between those disparate groups. On the public side, as securities services, we’re dealing more often with the public side of our internal partners, such as the Institutional Client Group within FIC.”

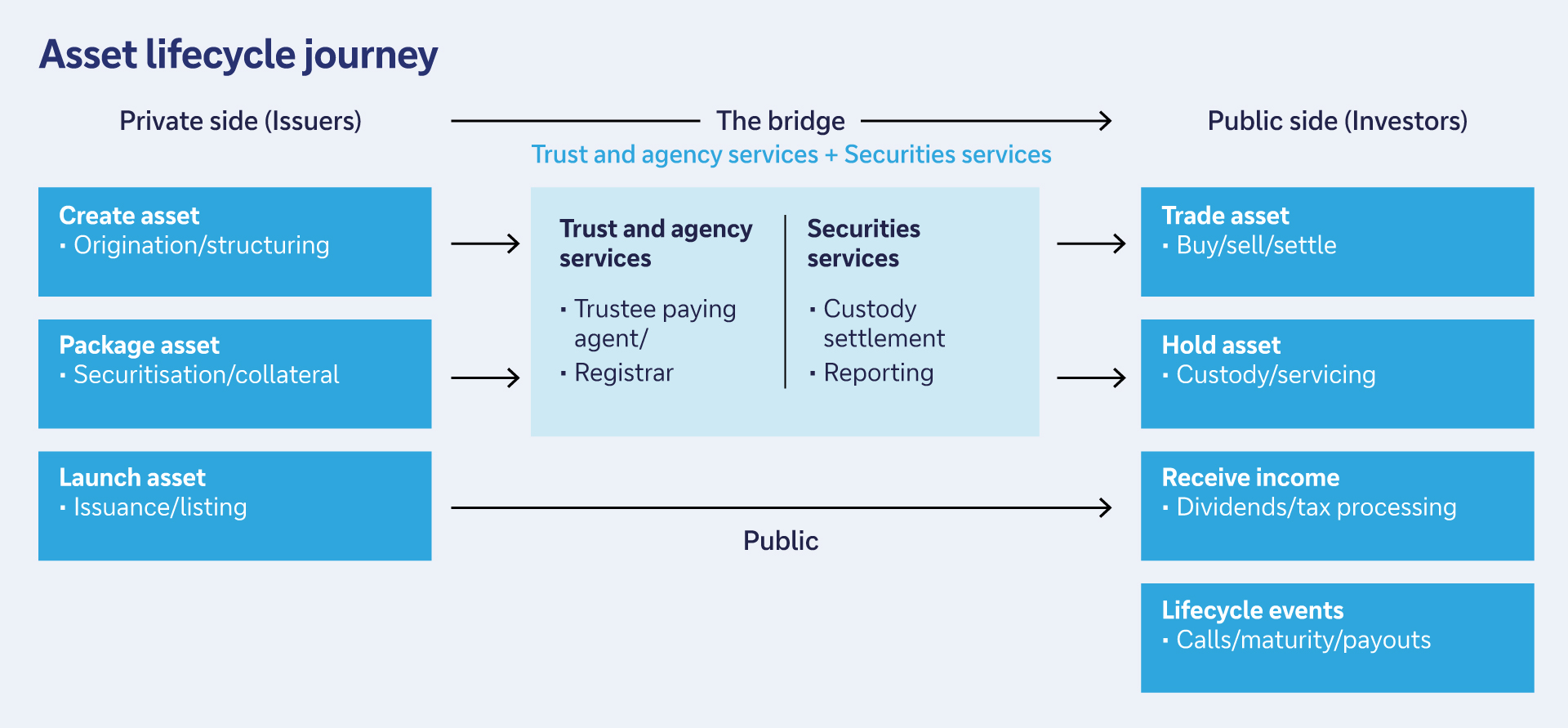

On the public side, custody, fund administration and asset servicing teams work with institutional investors whose buying centres are different from those on the private side, even though there is often an overlap in the parent names of those clients. That separation requires dedicated public side sales and servicing teams working with other parts of the bank. Yet at the senior levels, those same clients expect a single relationship across the whole bank to bridge the lifecycle of an asset (see Figure 1). As Maley puts it, “They don’t want to deal with agent bank complexity issues… they want the bank to cover the lifecycle of asset creation and the transaction itself, then brought back together in terms of the client experience.”

Figure 1: Summary of asset lifecycle, with TSS providing a joined-up client experience

Another distinction of this approach, says Maley, lies in TSS’s proximity to the bank’s lending and structuring capabilities, and he sees the growth story in connecting these components together to benefit customers. The core banking capabilities are provided to corporate and institutional clients who need to raise capital, monetise or fund projects by creating an asset (a loan, note, securitisation, or structured instrument) and selling it to investors. These components are flanked by ancillary and complimentary businesses that also serve the whole value chain. That business’s global investor services network also connects with Deutsche Bank’s Institutional Cash Management services to help institutions manage their cross-border payments and liquidity.

A safe harbour in the storm

The International Monetary Fund’s Payment Frictions, Capital Flows, and Exchange Rates paper1 looks at geoeconomic stressors to financial services and the role of financial intermediaries providing the operational infrastructure and continuity needed when markets fragment. Maley observes that it’s often the personal relationships that underpin this provision. “Clients often tell us, ‘If I’m going through a crisis, if I’m dealing with high levels of volatility and my P&L is moving rapidly, I want to talk to a trusted service manager, not a chatbot or a remote call centre’. Clients want a telephone number and a familiar voice that knows their business.”

These client voices drive the modus operandi. “We are the port in the storm that our clients can always rely on,” Maley points out. “The services themselves don’t change, but clients need a strong, resilient, trusted partner in periods of volatility and instability around asset prices, or tariff shocks, and sanctions shocks. These are moments where supporting our clients, via guidance on how to interpret the latest developments on the world stage, is a key reason why they choose to work with us.”

Amid geopolitical tensions, pressures on central bank policies are sharpening the search for safe havens. A Deutsche Bank Research Institute paper notes2 how these tensions influence the reserve banking system, the overlapping shifts in asset flows, and why some countries have begun to favour gold reserves.

The role of Deutsche Bank during moments like this is to enable clients to implement changes to their investment strategy and how that alters the shape of their portfolios.

AI and risk

We turn to the topic of artificial intelligence (AI), another force of change in businesses including for issuer and investor services. TSS is on the frontier of these changes at Deutsche Bank by introducing new services like Docutise (which is based on Deutsche Bank’s AI platform called dbLumina), built on Google Gemini, which scans collateralised loan obligation and other issuance-related documentation, extracting key points with a high level of accuracy – already saving tens of thousands of person-hours in the process.

The calculus shifts, however, when AI touches client assets. The advent of Claude Mythos in April this year, an AI software with possible ‘super hacker’ potential,3 illustrates the cybersecurity threat landscape that banks now need to navigate, given the network effect between agent banks, jurisdictional exposures, and the role of central securities depositories (CSDs).

Maley is direct on this point: “The AI narrative has been dominated by ‘hey, I can help you write your emails and organise your calendar’. So what? When I think about AI, I am more focused about the potential for systemic risk and our responsibility for other people’s money.” This is something that has concerned regulators as well – for example the Bank of England, the Financial Conduct Authority and HM Treasury in the UK published a joint statement on frontier AI models and cyber resilience in May 2026.4

“We are the port in the storm that our clients can always rely on”

New vehicles for growth

No discussion about change would be complete without touching on the advent of digital money. Deutsche Bank’s new whitepaper – ‘Digital Money: a perspective on stablecoins, tokenised deposits and CBDCs’ – shows how asset servicing companies, financial market infrastructure providers and custodians are enabling the interaction between digital money and real-world use cases.

Maley notes the newfound enthusiasm for tokenisation, promulgated by the US Genius Act5 – “the legal guardrails by which more traditional franchise players like us are going to navigate the brave new world”.

He observes that the natural competition between dematerialised assets at The Depository Trust and Clearing Corporation (DTCC) and Clearstream, and how they intersect in a world of tokenised assets, brings an unavoidable discussion topic. The challenges of supporting and paying for competing infrastructures and managing them in parallel need to be addressed. “Clients I hear from don’t want to pay for two ecosystems,” Maley states. “The CSDs have the advantage of being based in one jurisdiction, with one centralised platform – for the banks who operate in dozens of markets in parallel, the challenges are more material.”

International central securities depositories Clearstream,6 Euroclear7 and the DTCC8 are working to address this and offer a proxy for tokenising investor services. These settlement infrastructures plan to tokenise everything: whether the asset is a dematerialised security or a tokenised security; it will be the same asset each time.

But issuer services look different. The Bank for International Settlements noted that tokenised issuance of bonds and structured products remains small and fragmented, with limited secondary market liquidity preventing broader adoption in issuer services.9 Maley observes, “It’s easy to tokenise accessible and high-quality liquid assets such as cash, central bank reserves and government bonds. But unless liquidity moves, the business will stay where it is.”

He believes tokenisation of HQLA, the baseline against which all other assets are priced, would be a tipping point. “As long as the most easily accessed, most marginally risk-free assets are operating on traditional rails, that part of the ecosystem will be much slower to move. It’s a case of wait and see for issuer services – there’s more to come.”

Maley, speaking at the ‘The future of custody roadmap’ industry discussion, hosted by Global Custodian, on 14 May 2026 in London. Image: Global Custodian

Tracking TradFi and DeFi

With plans to launch digital assets custody, Deutsche Bank will track the natural tension between commercial bank payment rails and new entrants in cross-border payments and remittances such as stablecoins. “Clients want access to both and expect Deutsche Bank to be able to deliver that,” Maley states. “That is our job to provide those services. However, the overarching element and more interesting part is what it will mean for all commercial banks if payments move closer towards stablecoin rails.”

“We will service clients in both domains,” he continues. “We want to prepare for the future, which lies more in the direction of tokenised deposits. If all securities were to be tokenised, then you’re going to have to be able to deal with a tokenised or digital asset environment for even your existing inventory of securities.”

The next big thing

With tokenisation moving the payment and asset legs closer together, Maley observes that “atomic settlement of both payments and securities becomes not just a possibility, but a reality”.

Do any of these natural tensions present a threat to the status quo? Maley doesn’t believe so. “I don’t think there’s a threat to the reserve banking business model. Stablecoins will be an important use case and will likely continue to grow further – particularly for international remittances and store-of-value for people who live in unstable economies.”10

In conclusion, Maley envisages tokenisation moving together as a concept across securitised products and cash, with providers such as Deutsche Bank helping to make it happen. “This is not a three-year story – but 10 years from now, that is a genuinely credible outcome that could move financial markets onto entirely new platforms,” he states. “This could also enable increasingly higher levels of balance sheet velocity because you can then exchange and trade assets 24/7.”

What our discussion illustrates is that in a world defined by change, the future belongs to those who innovate and stay close to clients. For Maley, that means building businesses by connecting components in ways the market clearly values.

Janet Du Chenne is a freelance financial journalist and a former Co-Editor of flow and of Global Custodian

Sources

1 See Payment frictions, capital flows and exchange rates at elibrary.imf.org

2 See The return of history: gold, the dollar, and the monetary future at dbresearch.com

3 See When AI Becomes the Hacker: Claude Mythos Risks by Boston Institute of Analytics – May 2026

4 See The Bank, FCA and HM Treasury joint statement on Frontier AI models and cyber resilience | Bank of England at bankofengland.co.uk

5 See Fact Sheet: President Donald J. Trump Signs GENIUS Act into Law at whitehouse.gov

6 See Clearstream’s official page for D7 / D7 DLT , covering digital and tokenised securities issuance at clearstream.com

7 See Euroclear’s hub for its digital issuance and settlement model at euroclear.com

8 See DTCC’s hub for its official tokenisation service at dtcc.com

9 See Tokenisation in the context of money and other assets: concepts and implications for central banks at bis.org

10 See Digital money: A perspective on stablecoins, tokenised deposits and CBDCs at flow.db.com

You might be interested in

Trust and securities services

Custody in an age of fragmentation Custody in an age of fragmentation

How are global custodians navigating the fragmented geopolitical landscape? And what’s their take on digital assets and artificial intelligence? flow shares insights from BBH, Clearstream, JP Morgan and State Street

Custody in an age of fragmentation More

Trust and securities services

Ready for take-off: scaling digital assets Ready for take-off: scaling digital assets

As digital assets move from proof of concept to application, banks face a number of operational and regulatory challenges. Sabih Behzad, Head of Digital Assets and Currencies Transformation at Deutsche Bank, shares what it takes to scale digital assets responsibly

Trust and Securities Services

Europe’s T+1 transition: lessons, readiness and what firms need now Europe’s T+1 transition: lessons, readiness and what firms need now

With Europe’s October 2027 T+1 transition deadline now firmly in scope – and its practical complexities crystallising – flow securities services correspondent Janet du Chenne meets the Deutsche Bank Trust and Securities Services team translating US lessons, internal readiness work and industry guidance into coordinated client action