-

Cash management

Inside downstream correspondent banking – and why it matters

9 April 2026

As regulation and standards evolve, the view of risk linked to downstream correspondent banking relationships is also changing. Deutsche Bank’s Matthew Probershteyn explores this shift in perception – and examines how banks are strengthening both control frameworks and transparency in practice

MINUTES min read

Correspondent banking refers to the arrangement between two financial institutions that enables one bank to provide international transaction services on behalf of the other. As explained in the 10 September 2025 flow article, ‘What’s next for correspondent banking?’, “Reliable, accessible and affordable correspondent banking underpins participation in the global economy by supporting individuals, SMEs, large corporates, charities and financial institutions.”

Downstream correspondent banking – also known as nested banking – takes this model one step further. In this structure, a respondent bank allows additional financial institutions – often smaller, local banks without a direct correspondent relationship – to access the international financial system through its own correspondent account with a global bank.

Without such arrangements those financial institutions that either cannot afford the cost of maintaining direct correspondent relationships, or do not generate sufficient transaction volumes to justify them, would lose their ability to participate in the global economy. By extension, the individuals, small businesses, charities, and others that rely on these localised banks would also lose access to essential cross-border services, from sending remittances to paying suppliers and purchasing goods, or for personal payments such as for education, vacation and similar.

Downstream banking therefore plays a key role in extending access, particularly in emerging markets and regions where direct coverage may be limited. But how can this access be delivered while meeting the transparency, oversight and trust required to operate safely across borders?

Challenging the perception of downstream banking

Despite its benefits, downstream banking has historically carried negative connotations within parts of the financial industry. The concern has largely centered on transparency: when multiple institutions sit between the originating bank and the correspondent account, it can become harder for the correspondent bank to see who is ultimately accessing their services. If not carefully managed, these additional layers of intermediation can reduce visibility into the underlying institutions or customers involved in a transaction. Over the past 10 years, however, this issue has evolved along with industry standards and compliance-related investments.

Regulatory expectations around financial crime prevention – including principles such as beneficial ownership transparency, suspicious activity reporting and sanctions compliance – have become more consistent across major jurisdictions. In parallel, industry initiatives have helped standardise due diligence practices across correspondent banking relationships.

Among these is the Wolfsberg Group’s Correspondent Banking Due Diligence Questionnaire (DDQ).1 Produced by the Basel-based Wolfsberg Group, an association of 12 major banks tasked with developing frameworks and guidance for the management of financial crime risks, the DDQ provides a common framework for banks to disclose and assess their compliance controls. Covering areas such as anti-money laundering governance, sanctions controls, transaction monitoring frameworks and internal compliance structures, the Questionnaire enables institutions to demonstrate that they meet the baseline standards required to participate in correspondent banking networks.

These transparency expectations also extend beyond the onboarding stage. Regulators expect banks to review downstream relationships on an ongoing basis, assess the risk profile of downstream institutions and ensure that respondent banks maintain robust due diligence programmes for their own customers. Correspondent banks support this oversight through advanced transaction monitoring, behavioural analytics and network-level surveillance, allowing unusual activity to be identified through patterns that may not be visible within a single institution.

An additional factor is that payment infrastructures have become increasingly digitalised and standardised, so the amount and quality of information available to institutions processing cross-border payments has increased substantially. For example, the November 20252 full adoption of ISO 20022 – the global messaging standard for cross-border payments – enables banks to capture richer and more consistent payment data, improving the identification of all parties involved in a transaction and strengthening screening and monitoring capabilities.

Taken together, these developments have created a more transparent and interconnected correspondent banking ecosystem, enabling institutions to manage downstream relationships with greater visibility and confidence than before.

“Correspondent banking remains at the heart of the global financial system”

Building robust risk frameworks

A key shift in industry thinking is the recognition that downstream banking does not necessarily create a single point of risk. When properly structured, it can instead engender multiple layers of oversight to create ‘strength upon strength’ resilience in risk management and financial crime prevention.

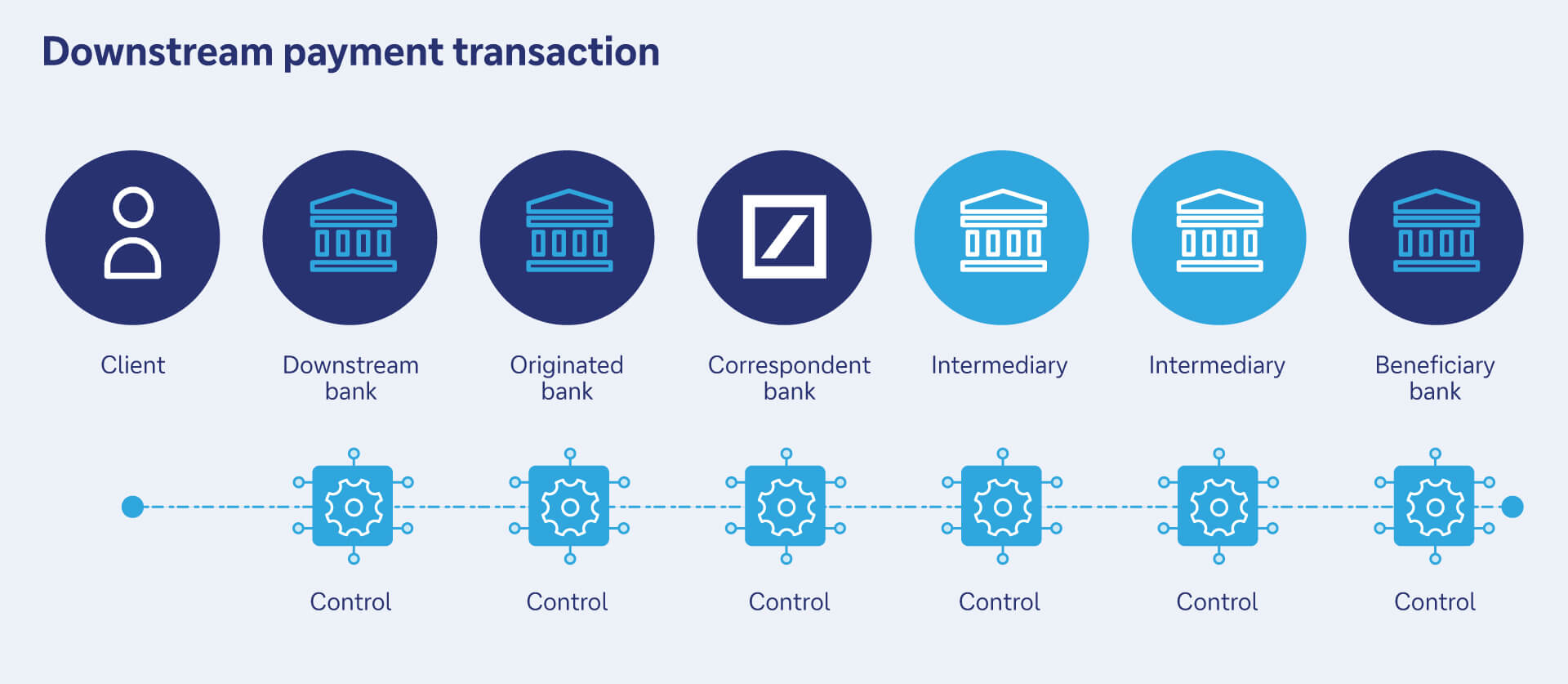

What this means in practice is that, in a typical downstream payment chain, several institutions apply controls to the same transaction. A payment initiated at the downstream bank will first pass through that institution’s compliance checks and monitoring processes before being processed by the respondent bank, which has already met the correspondent bank’s due diligence requirements. The transaction is then screened again by the correspondent bank before reaching the receiving institution, which applies its own controls. In addition to these three layers of controls, additional layers are applied by intermediary banks, and a beneficiary bank.

Figure 1: Downstream payment transaction

Source: Deutsche Bank

This is viewed not simply as a technical control framework but as an ecosystem approach to risk management in which partnership, shared responsibility and transparency apply across institutions with a common goal and shared risk appetites which is, these days, a prerequisite to participate. In this model, correspondent banks, respondent banks and downstream institutions all play complementary roles in protecting the integrity of global payments infrastructure, while maintaining connectivity for end customers around the world.

In this context, downstream banking becomes less about transferring risk and more about distributing oversight across a network of institutions. Rather than exiting relationships when concerns arise, banks increasingly collaborate to strengthen controls, share information, address vulnerabilities and reduce risk at its source. The flow article ‘An ecosystem approach to limit de-risking’ (10 June 2024) takes a deeper dive into the de-risking trend, highlighting “the collective role all constituents in the ecosystem have to play to curb the de-risking trend and enhance the fight against financial crime from central and commercial banks to law enforcement, regulators and clients”.

From downstream banking to access banking

As cross-border payment infrastructures continue to evolve, correspondent banking remains at the heart of the global financial system. While new technologies, payment platforms and settlement models may reshape how transactions move across borders, access to correspondent networks – directly, or indirectly through downstream banking relationships – will remain a key resource for many institutions.

The key is to ensure that transparency, due diligence and ongoing monitoring are exercised by all parties in the chain, with the broader ecosystem aligned around these principles. When these safeguards are in place, downstream banking becomes an enabler of financial inclusion rather than a perceived risk to correspondent banks. Through this lens, downstream banking – or, more accurately, ‘access banking’ – is increasingly recognised as a valued component of a resilient and inclusive global financial ecosystem.

Sources

1 See Publication of the CBDDQ, FCCQ, Guidance, Glossary and FAQs at wolfsberg-group.org

2 See Global financial community completes switch to ISO 20022, paving the way for new levels of cross-border payment speed and innovation around the world at swift.com

You might be interested in

Cash management, Opinion

What’s next for correspondent banking? What’s next for correspondent banking?

Correspondent banking is the backbone of cross-border transactions, but the sector faces pressure from an adverse and evolving risk environment as well as shrinking networks. Deutsche Bank’s Matthew Probershteyn and Vanessa Meister explore how reframing the model around access, resilience and innovation can future proof its longevity

flow case studies, Cash management, Trade finance and lending {icon-book}

Brazil’s gateway to global trade Brazil’s gateway to global trade

How can Brazilian businesses finance cross-border trade in a volatile global landscape? Drawing on the example of Banco do Brasil – the country’s second-largest bank – flow explores the role that correspondent banking plays in enabling these transactions

Cash Management, Regulation

One giant step to payments innovation? (Part 1) One giant step to payments innovation? (Part 1)

At Sibos 2025 Frankfurt, two clear themes for the payments industry emerged: the need to refresh its foundations and accelerate innovation. In the first of two wrap-ups, flow reports on sessions discussing the balance between a safe financial system and friction-free payments