-

Cash management, Technology

Tech in corporate treasury: AI is not the whole story

18 June 2026

Across key treasury functions, artificial intelligence is moving from experimentation to active deployment. Drawing on his latest treasury survey, Dr Tobias Miarka of Crisil Coalition Greenwich explains where AI is adding most value – and why some companies are focusing on the wrong priorities

MINUTES min read

Artificial intelligence (AI) has become the centrepiece of corporate treasury innovation plans and investment budgets. A new study from Crisil Coalition Greenwich reveals that after a period of pilot programmes and experimentation, a growing number of global companies are already deploying AI solutions in their treasury departments or plan to do so within the next 12 months.

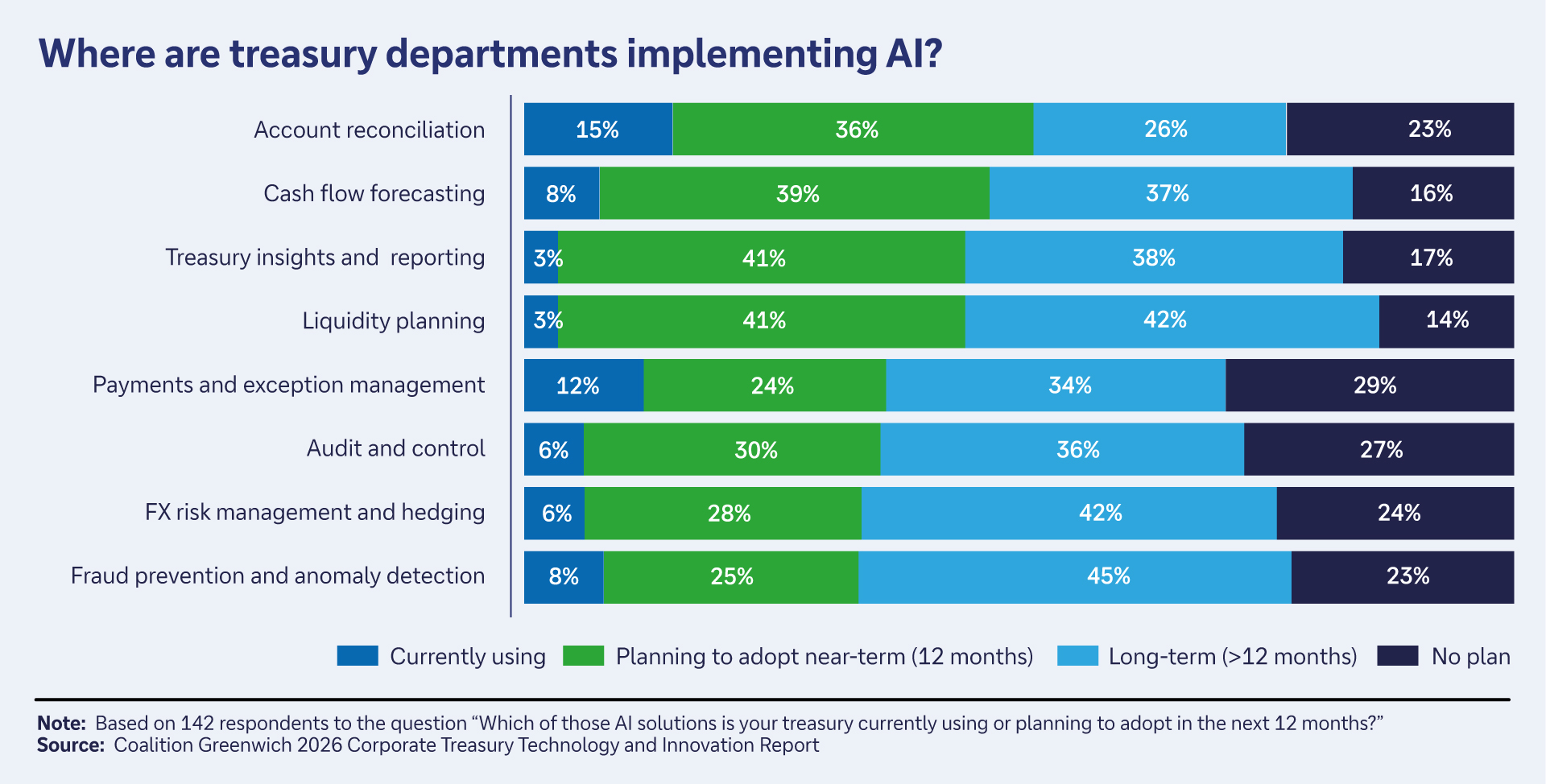

In an article for flow in February 2026 I noted that data issues and a lack of in-house expertise are preventing AI’s full potential from being realised in corporate treasury. While these obstacles persist, key treasury functions are now being ramped up with AI, as evidenced in our February 2026 survey among treasury professionals from 142 major companies around the world (see Figure 1).

Figure 1

Source: Coalition Greenwich 2026 Corporate Treasury Technology and Innovation Report

The area where corporate treasurers see the greatest value in AI is account reconciliation, with more than half of corporate treasury departments either already employing this technology or planning to use it within the next 12 months. With the help of AI nearly half of the companies surveyed have already improved or plan to improve cashflow forecasting, treasury insights and reporting, as well as liquidity planning. It is equally significant that over a longer period, more than three in four companies are planning to implement AI tools in all but two areas that were discussed.

AI in treasury: buy or build?

As a general rule, most study participants appear to be ambivalent about how they acquire these AI solutions. While some companies opt either to build them in-house or buy them directly from technology vendors, many others will utilise AI tools built into the enterprise resource planning (ERP), treasury management systems (TMS) and other systems they already use and pay for. For example, firms such as SAP and Oracle are integrating predictive analytics and other AI applications that harness both the client’s proprietary data and anonymised data from other users.

These providers have a strong incumbency advantage. Their AI applications are already installed and available to treasury staff for experimentation and actual adoption. That’s a bonus for treasury departments, which can try out these offerings, figure out if their built-in applications meet their needs, and consider the comparative benefits of building or buying.

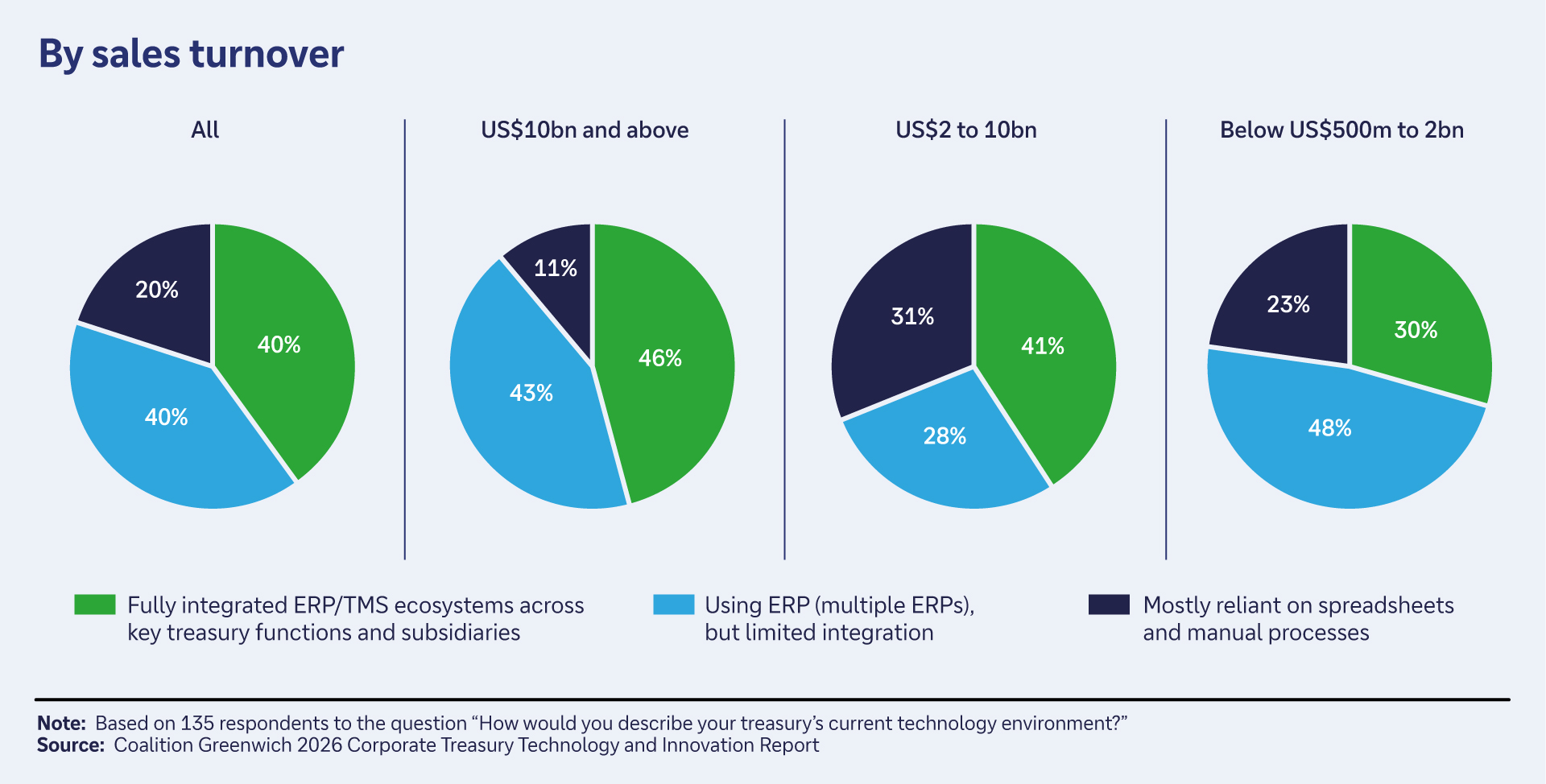

However, system and data fragmentation remains a challenge. The survey finds that about 40% of corporate treasury departments run on multiple ERP systems, with limited integration (see Figure 2). More worryingly, about one in five large corporates still work with spreadsheets and manual processes, with spreadsheets even now still the baseline technology used in corporate risk management processes.

Figure 2

Source: Coalition Greenwich 2026 Corporate Treasury Technology and Innovation Report

The good news is that companies recognise the need to modernise these systems, and they are moving to address the issue. Automating manual processes, eliminating spreadsheets, and integrating ERP, TMS and banking systems all rank among treasury departments’ top stated priorities.

Breaking down barriers between the systems is a first and necessary step in securing that data. But it’s not enough. To implement predictive analytics and other sophisticated AI solutions at scale, companies will need much more and much better data. This makes it imperative to first create comprehensive data management and governance platforms that operate across integrated systems.

However, our research suggests that some companies could be risking a misstep as they work to adopt and integrate new technology. Less than a quarter of large companies overall and only about one in five of all participant corporates cite improving data quality and reliability as a top priority for their treasury departments. Hence, companies risk missing out on AI’s full potential.

Other new technologies on the horizon

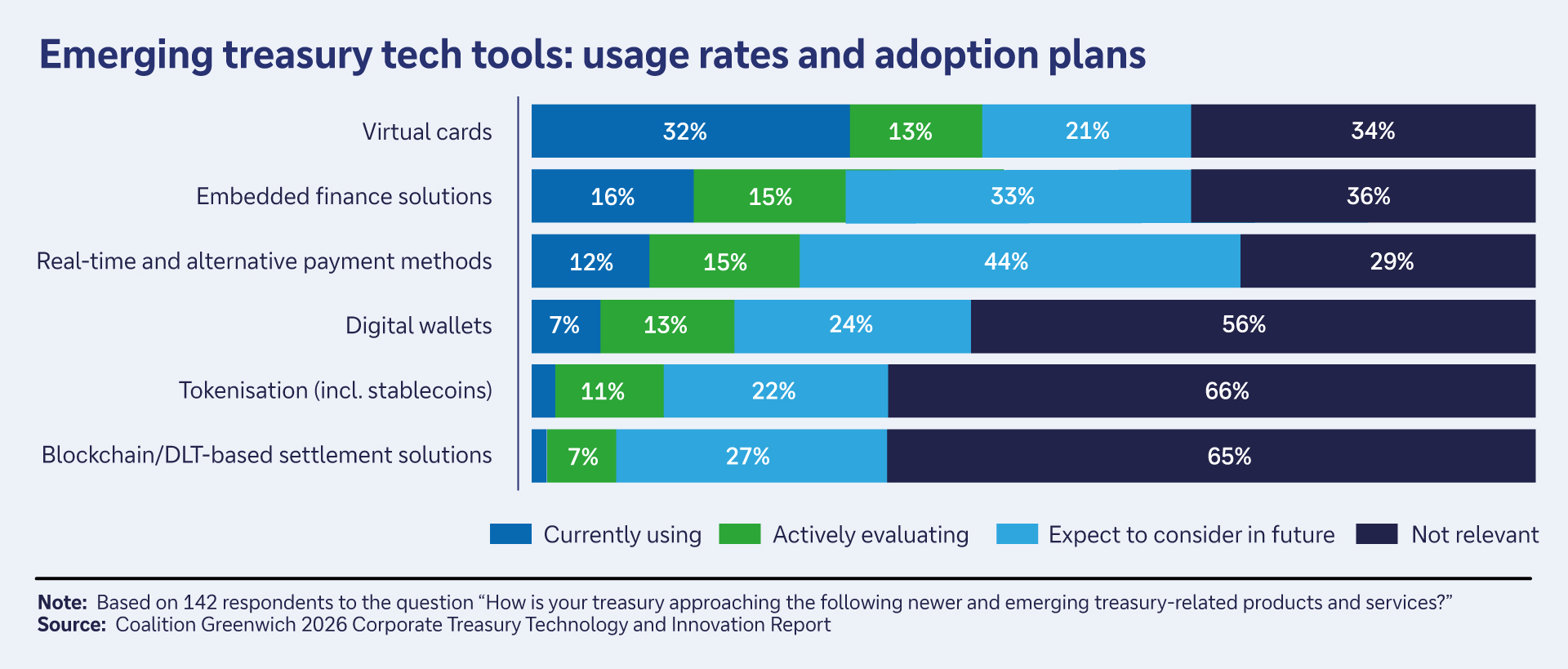

AI is not the only innovation companies are using to overhaul the treasury function. They are equally advancing on the adoption of new structures and concepts as the survey shows. As shown in Figure 3 below, approximately 45% of companies are using or actively evaluating the use of virtual cards, and nearly a third are using or evaluating embedded finance solutions. By using application programming interfaces (APIs), banking functions such as payments, liquidity and lending can now be embedded directly into ERP and TMS improving efficiency and transparency of these processes.1

Moreover, roughly 70% of companies expect to consider real-time and alternative payment methods at some point. While instant payment regimes have been around for quite some time, they are only just entering the wider B2B space. In the euro area, for example, all banks and payment service providers must now be able to receive and send SEPA Instant Payments according to the EU Instant Payments Regulation.2 With reachability becoming the baseline assumption rather than the exception, one of the obstacles for corporate adoption was removed.

Looking further ahead, around 45% of companies plan to take a close look at digital wallets, and about a third expect to consider adopting tokenisation (including stablecoins) and blockchain/DLT-based settlement solutions. These digital money rails could, for example, reduce frictions in the cross-border payment space and allow for programmable payments.3

Figure 3

Source: Coalition Greenwich 2026 Corporate Treasury Technology and Innovation Report

The survey also took a deep dive into the solution corporates are using for liquidity management (see Figure 4). As the chart show, physical cash concentration, zero balancing, in-house banking, and intercompany liquidity and funding have all emerged as common liquidity management solutions.

Figure 4: Popular uses for liquidity management solutions

Source: Coalition Greenwich 2026 Corporate Treasury Technology and Innovation Report

Yet, one thing is clear: most of the demand for these products is coming from the world’s largest corporates that have both the need and the budget for advanced tools. This is particularly apparent for a very sophisticated solution: virtual account management (VAM). While the efficiency gains and other returns on that investment can be significant, the VAM approach remains—at least for now—most appropriate for the biggest companies with complex structures, multiple entities and operations and cash flows across many regions and currencies. It has, however, good potential to develop over time into simpler and more cost-effective versions and become more accessible to a broader base of corporates.

In the interim, even among the largest corporates, VAM could prove a tough sell for banks unless the return on investment is more clearly explained. Around 40% of companies with annual sales in excess of US$10bn say they have no plans to even look at VAM solutions. That finding suggests banks might have to further reduce implementation complexity and make adoption easier for corporates if they want VAM to gain widespread traction.

Dr Tobias Miarka leads Crisil Coalition Greenwich’s Corporate Banking research globally and advises both international and domestic banks on strategic client service and product issues that develop profit-enhancing and sustainable solutions. He is also affiliated with the ESCP Business School where he teaches Banking and Fintech related subjects as part of the school’s Master in Management programme.

Sources

1 See Embedding the future of finance – Deutsche Bank at flow.db.com

2 See Instant Payments Regulation at ecb.europa.eu

3See Digital Money – a perspective on stablecoins, tokenised deposits, and CBDCs – Deutsche Bank at flow.db.com

You might be interested in

Cash management, Technology

AI in corporate treasury: what are the barriers to adoption? AI in corporate treasury: what are the barriers to adoption?

Data issues and slow integration/adoption are preventing artificial intelligence’s full potential from being realised in corporate treasury. Dr Tobias Miarka of Crisil Coalition Greenwich examines what this means for businesses and treasurers

flow white papers and guides

Digital Money – a perspective on stablecoins, tokenised deposits, and CBDCs Digital Money – a perspective on stablecoins, tokenised deposits, and CBDCs

This new white paper explores the digital money landscape – spanning stablecoins, tokenised deposits and central bank digital currencies – the regulatory and market forces shaping it, and how these changes are impacting financial institutions, corporate treasury and custody models

Cash management, flow case studies

Embedding the future of finance Embedding the future of finance

Cash flow visibility and supplier engagement are among the benefits that result when financial services are embedded into non-financial platforms. flow’s Clarissa Dann examines corporate appetite for embedded finance and shares how Deutsche Bank has combined the innovation and agility of a start-up with the safety of a Tier-1 European bank to make this available to clients