-

Cash management, Trust and securities services

Working with NBFIs

22 April 2026

Non-bank financial institutions (NBFIs) and the rapid growth of private markets offer investors an opportunity to diversify their portfolios, but what do they need in order to work safely within the financial system? flow’s Clarissa Dann and treasury correspondent Graham Buck set out the NBFI landscape and explain how regulated banks are supporting them

MINUTES min read

With the global asset management industry having surged past a record US$128trn of assets under management (AuM) in 2024,1 the role of non-bank financial institutions (NBFIs) in this global AuM sector is expanding fast. They have attracted significant capital, making them indispensable components of the modern financial system.

Alongside this growth, the increasing influence of NBFIs has also resulted in ongoing scrutiny from regulatory bodies to mitigate potential systemic risks. The sector includes:

- Asset managers;

- Private equity firms ('financial sponsors');

- Hedge funds;

- Insurance companies (many of them managing large investment portfolios);

- Pension funds (that manage huge sums for retirees); and

- Sovereign wealth funds (government-owned funds investing national reserves).

This ‘explainer’ article sets out the NBFI landscape and examines the partnership between financial sponsors (private equity investors backing high growth companies) and global banks, as these financial sponsors acquire target companies and exit them.

Once the legal entity or special purpose vehicle (SPV) is in place, the corporate banking services include setting up cash accounts and securities accounts in the relevant geographies.

A look at the alternatives market

According to the Private Markets in 2030 report published by data and intelligence firm Preqin on 16 October 2025, the global alternatives market is projected to reach more than US$32trn in size by 2030, spanning private equity, credit, infrastructure, real estate, hedge funds, and natural resources.2 By definition, the term ‘alternatives’ means non-traditional assets, typically less correlated with traditional asset classes such as equities and bonds.

The market currently sits at around US$17trn. Cameron Joyce, Preqin’s Head of Research Insights said, “The convergence of public and private markets is reshaping investor expectations, driving demand for transparency, standardised data, and whole portfolio solutions.” Joyce also expects artificial intelligence (AI) to “accelerate VC-backed innovation and infrastructure investment, fuelling growth across private equity”.

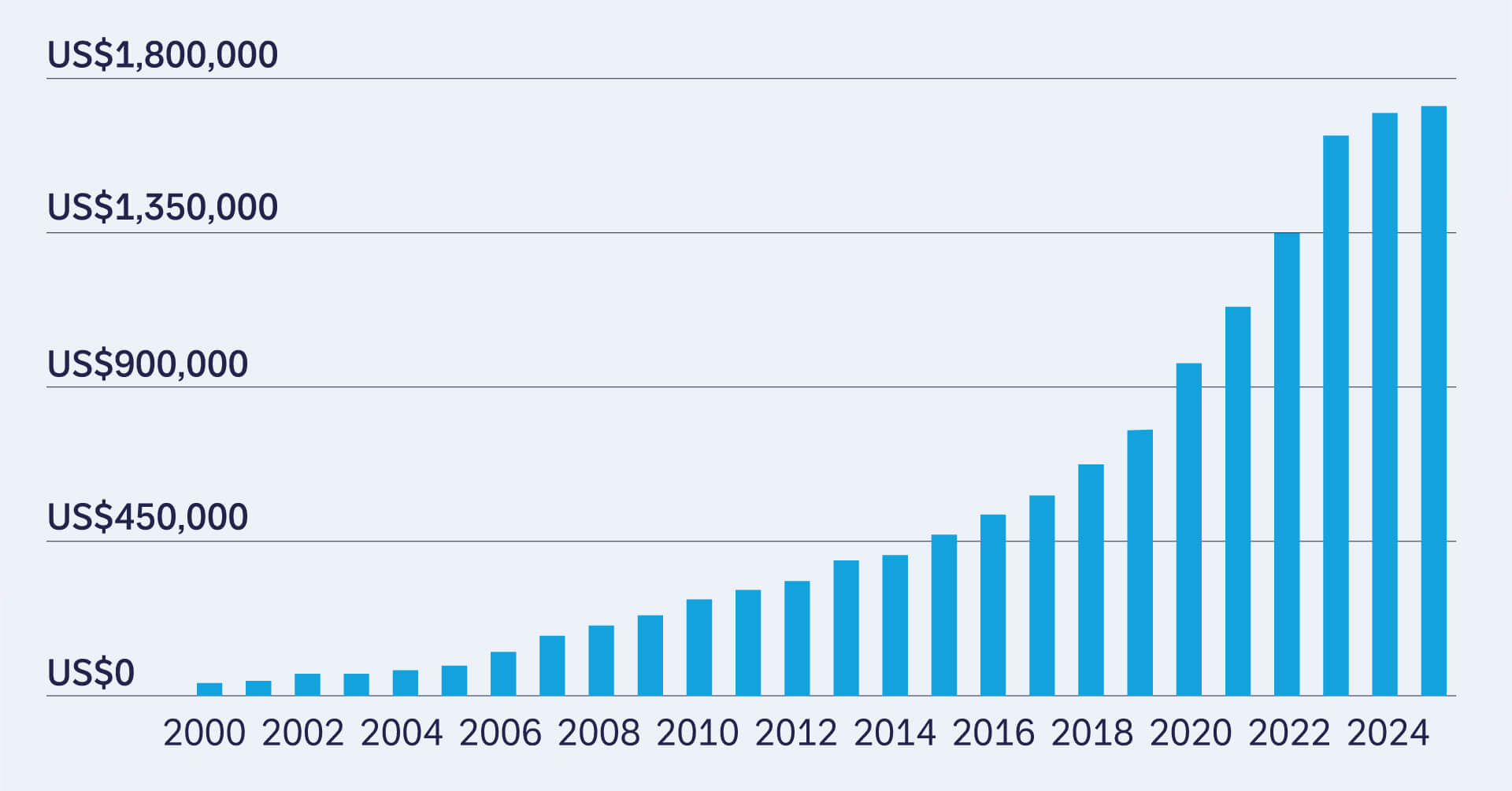

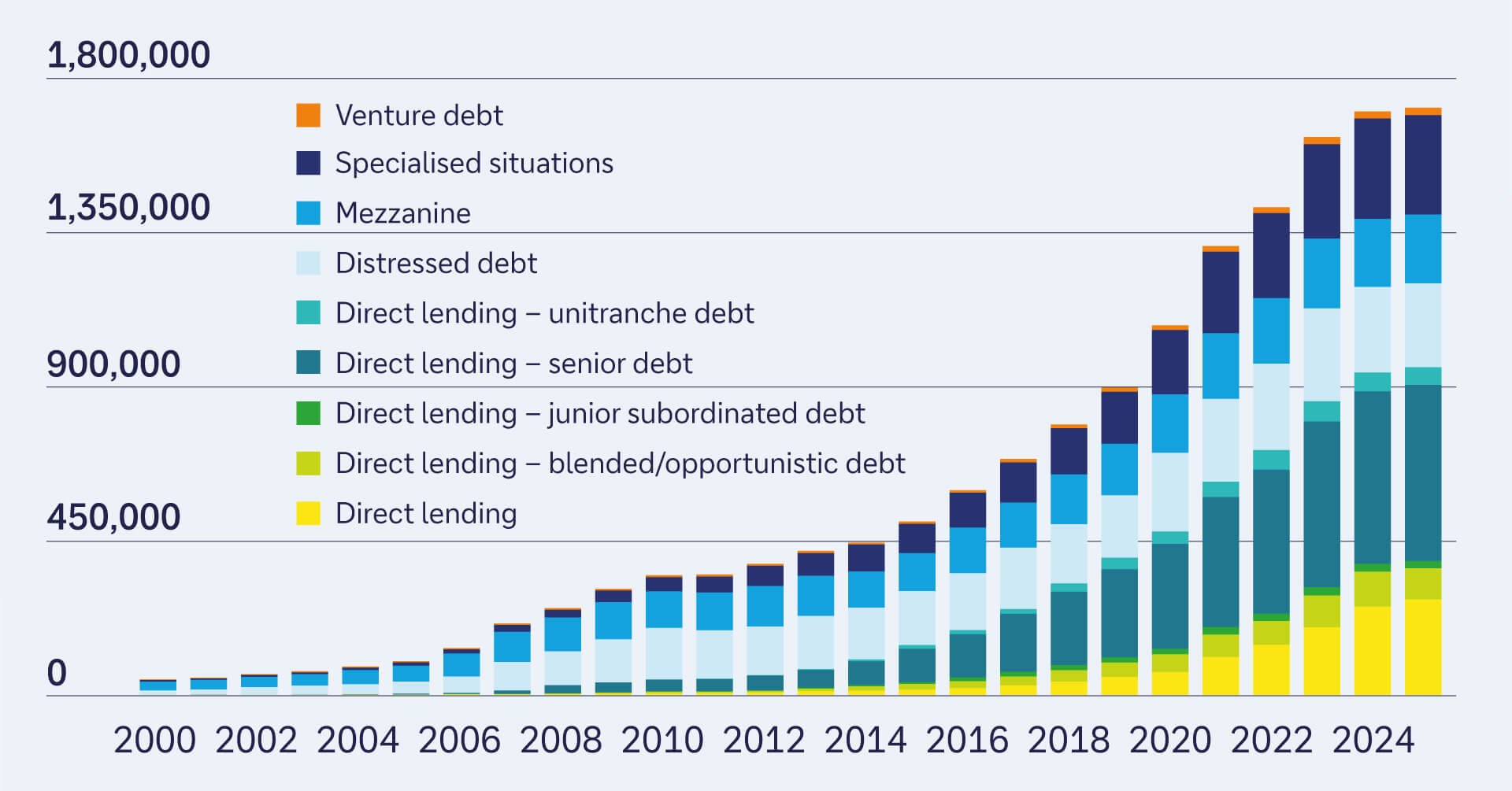

A growing component of this market are the private equity and private debt/credit markets (which includes structured products such as collateralised loan obligations). flow’s October 2024 article ‘Private credit – a rising asset class explained’ sets out the market’s characteristics: “Private credit is non-bank lending typically to middle market companies ranging in size from US$25m to US$75m in EBITDA. These companies can either be sponsored, or owned by a private equity firm, or non-sponsored.” The updated totals are set out in Figures 1 and 2 with the total AuM in this asset class at US$1.78trn as of the end of H1 2025.

Figure 1: Total private debt 2000 to H1 2025 (US$bn)

Source: Preqin - a part of BlackRock

Figure 2: Components of private debt 2000 to 2025 (US$m)

Source: Preqin - a part of BlackRock

This surge in growth underlines the global rise of financial sponsors from the increased ranks of NBFIs, particularly across the US and Asia, and alternative assets. These are investors (often a private equity firm) that, by providing capital to a target company (more often than not giving them a controlling stake) set out to increase its value before exiting via a sale or stock market flotation.

Widening investor base

While institutional investors traditionally dominated the alternatives market, the investor base is widening. Alongside pensions, insurers and sovereign wealth funds, individual investors can now access alternative strategies through collective investment schemes, contributing to the growing depth and diversification of capital flowing into sponsor-led vehicles.

Turning to Germany, its retail investors are belatedly warming to alternatives as lenders, including Deutsche Bank and fintech platform Trade Republic, expand access to private equity for retail investors. On 21 October 2025, the Financial Times reported Claudio de Sanctis, Head of Deutsche Bank Private Bank’s observation that “German retail investors represent one of the world’s largest untapped pools of wealth and private equity firms are eager to gain access.”3

What is an NBFI?

As the name would suggest, NBFIs are financial institutions that are not legally banks, lack a full banking licence and cannot accept deposits from the public, although they are a source of consumer credit.

They also facilitate a range of alternative financial services (several of which are not suited to banks) including investment – collective and individual, risk pooling, financial consulting, brokering, money transmission, and cheque cashing.

The UK’s Financial Conduct Authority comments that “non-banks encompass a wide range of business models, including pension funds, insurers, hedge funds, and many others,” whose activities “are vital for the financial health and growth of the (UK) economy.”

Within the private capital markets, financial sponsors play a critical role in the private equity landscape and connect investment opportunities with sources of capital – they are specialist investors seeking companies not yet publicly traded and looking for enhanced value over time. Financial sponsors operate across private equity, private credit, infrastructure and real estate.

These firms include alternative asset managers, investment organisations that raise capital from investors and deploy it into companies, platforms and assets to generate long-term returns, currency exchanges and some microloan organisations.

The World Bank is approving: “Having a multi-faceted financial system, which includes NBFIs, can protect economies from financial shocks and recover from those shocks. NBFIs provide multiple alternatives to transform an economy’s savings into capital investment, which act as backup facilities should the primary form of intermediation fail.”4

Supervision and oversight

While insurers are the most obvious exception as they must meet the requirements of the Solvency II regime5 many other NBFIs are also, notably, exempt from supervision by a national or international banking regulatory agency. This absence has sparked concerns that there is only limited understanding within governments and regulatory bodies of the risks that entities sometimes termed ‘shadow banks’ pose to the stability of the wider financial system.

In 2021, the European Central Bank published its paper, Non-bank financial intermediation in the euro area: implications for monetary policy transmission and key vulnerabilities, which pointed out that “Compared with banks, NBFIs are more responsive to monetary policy measures that influence longer-term interest rates, such as asset purchase.”6

Bank of England (BoE) Governor Andrew Bailey has warned that the issue must be addressed as regulators cannot afford to rest on their laurels just because the resilience of traditional lenders was strengthened after the 2008 global financial crisis.

“The challenge now lies in managing risks that sit beyond the banking perimeter as well as identifying and understanding new interconnections between banks and non-banks,” he wrote in The Banker magazine.7 “There remains a particular and urgent need to increase resilience in market based finance globally.”

In December 2025, the BoE launched its second system-wide exploratory scenario focusing on how the private markets ecosystem operates under stress and the potential implications for UK financial stability and Britain’s real economy.8 The initiative – to gauge the potential economic and financial impact of any future crisis within the industry – is the first of its kind by any global regulator and the exercise has the participation of major private market players including Apollo, Ares, Blackstone, Carlyle and KKR.

“The rapid growth of private markets has brought many benefits, such as providing additional and more diverse forms of long-term capital to support economic growth,” the BoE commented. “However, the resilience of private markets, in their current form, to a severe downturn has not been tested yet.”9

Serving financial sponsors – coverage

Deutsche Bank’s Financial Sponsors Group (FSG) was set up in 1996, initially as a one-person unit to co-ordinate Investment Bank products together with corporate banking services aimed at private equity firms. It has developed over 30 years to offer coverage to the large global private equity entities.

The FSG’s resources span derivative products; equity products; industry expertise; leveraged finance – with services and products for each stage of a leveraged buy-out – and mergers and acquisitions advisory. The FSG will also set up accounts for the client to finance an acquisition and provide prompt transmission of funds to the interested party.

Deutsche Bank has been developing its partnerships with asset managers in recent years and expanding access to private equity for retail investors. Having provided fund backing for several acquisitions made by Blackstone (the world’s largest alternative asset manager10), in January 2025 it formed a global distribution partnership with the group to expand access to Blackstone’s evergreen private equity fund, Blackstone Private Equity.11

Corporate banking services

Financial sponsors will be constantly on the look-out for target companies, so will have a merger, acquisition and stock purchase pipeline that may span multiple jurisdictions, legal entities and tax arrangements.

Cash management

They require fast and efficient onboarding for up to several hundred accounts across their funds, SPVs, and other entities. Investment timelines are often sensitive, so account opening must occur within days and require bank capabilities such as digital KYC, centralised onboarding teams and the ability to support multiple jurisdictions.

“The ability to confidently move money across jurisdictions is what a fast-moving investment environment requires”

At the core of the Deutsche Bank cash management platform, explains Sanu Miah, Global Head of NBFI Corporate Cash Management Solutions Sales, is “a partner that allows sponsors to view and manage cash across funds, SPVs, and geographies as one ecosystem rather than a patchwork of accounts and banks”. For capital calls and distributions, he adds, “the payments solutions facilitate the straight-through processing incoming and outgoing wires, and files flow directly from the fund administrator or treasury system into the banks payment rails, reducing manual touchpoints and settlement risk”.

Once FX execution is layered in together with a choice of reporting options, and connectivity to fund administration platforms, the result, says Miah, is “a cleaner operating rhythm, stronger governance, and the ability to confidently move money across jurisdictions – exactly what a fast-moving investment environment requires”.

Reflecting on how the ECB Financial Stability Review (2023) underlines how deeply connected the NBFI community is with systemically important banks,12 Global Head of Corporate Cash Product Johnny Grimes notes, “At Deutsche Bank we are deeply dedicated to supporting this critical financial segment, working closely together on products and services which manage their cash safely and efficiently. This is a very nimble and fast-moving community and that agility, combined with Deutsche Bank’s strong capital base and resilience, makes for a transformative partnership.”

Trust and Securities Services (TSS)

This long-established Deutsche Bank business offers a comprehensive suite of solutions designed to support financial sponsors and NBFIs throughout their investment journey.

“Our mission is to be a trusted partner to financial sponsors, providing them with the critical infrastructure and expertise needed to navigate complex investment landscapes,” explains Daniel Clark, Global Head of Depositary Receipts and Head of Trust and Securities Services, APAC & MEA at Deutsche Bank. “We understand the unique challenges and opportunities that arise at each phase of an investment, and our integrated approach ensures our clients receive tailored support that drives success.”

This support includes ongoing safekeeping and asset servicing as sponsors venture into multiple global markets and invest across diverse asset classes. The overall TSS role comprises:

- Acquisition financing and corporate trust. When a financial sponsor seeks to finance an acquisition through a loan, Deutsche Bank’s corporate trust team steps in as the loan agent. They administer the loan, secure collateral, perform crucial calculations, and monitor covenants on behalf of participating banks. This ensures transparency and compliance throughout the financing period, safeguarding the interests of all parties involved.

- Protecting interests during negotiations using escrow solutions. For sellers engaging with financial sponsors, escrow solutions provide a vital layer of security during negotiations. Funds are securely held until all relevant conditions are met or negotiations conclude. This mechanism ensures that cash and shares are only transferred upon the successful closing of the transaction.

- Strategic exits via initial public offerings (IPOs) using depositary receipts. The final stage of the investment journey often involves a strategic exit, either through a private sale or an IPO. This is where Deutsche Bank's depositary receipts services support financial sponsors aiming to take their acquired private company public.

“When a financial sponsor considers an IPO, especially if they are looking to attract a broader investor base, particularly from the US, a depositary receipts facility offers a powerful avenue,” states Clark. “It allows them to elevate the profile of their target company among foreign investors and make their shares easily accessible in more liquid, sophisticated markets like the US.”

Outlook for financial sponsors

At the start of 2026, the sector appeared poised for further growth. Reducing inflation, strong corporate earnings and balance sheets, high volumes of ‘take-privates’ and dealmaking and an abundance of capital in search of deployment all pointed to a flurry of financial sponsor activity.

It remains to be seen what now takes place, given developments since 28 February and the economic uncertainty unleashed by war in the Middle East.

To find out more about Deutsche Bank’s services for Financial Sponsor clients visit: https://corporates.db.com/clients/financial-sponsors

Clarissa Dann is Editorial Director of Marketing at Deutsche Bank, and Graham Buck is a freelance treasury journalist and former Cash Management Editor at Deutsche Bank

Sources

1 See From Recovery to Reinvention at bcg.com

2 See Preqin Releases Private Markets in 2030 Report at preqin.com

3 See German banks push private equity funds to retail investors at ft.com

4 See Nonbanking financial institution at worldbank.org

5 See Solvency II at bankofengland.co.uk

6 See Non-bank financial intermediation in the euro area: implications for monetary policy transmission and key vulnerabilities at ecb.europa.eu

7 See Banks’ present stability is hard won at thebanker.com

8 See Bank of England launches system-wide exploratory scenario exercise focused on private markets at bankofengland.co.uk

9 See Bank of England launches system-wide exploratory scenario exercise focused on private markets at bankofengland.co.uk

10 See Home - Blackstone at blackstone.com

11 See Blackstone joins forces with Deutsche Bank to expand private equity distribution at pe-insights.com

12 See Key linkages between banks and the non-bank financial sector at ecb.europa.eu

You might be interested in

Trust and agency services, Macro and markets {icon-book}

Private credit – a rising asset class explained Private credit – a rising asset class explained

Following flow coverage of collateralised loan obligations (CLOs) and trade finance assets from an origination and investor perspective, the flow team reviews private credit, an asset class which has grown significantly since the financial crisis. This ‘explainer’ includes an overview of the sector’s asset managers, borrowers, financing structures, geographies, investor capital, and product offerings

Cash management, flow case studies

Embedding the future of finance Embedding the future of finance

Cash flow visibility and supplier engagement are among the benefits that result when financial services are embedded into non-financial platforms. flow’s Clarissa Dann examines corporate appetite for embedded finance and shares how Deutsche Bank has combined the innovation and agility of a start-up with the safety of a Tier-1 European bank to make this available to clients

Trust and agency services {icon-book}

Collateralised loan obligations explained Collateralised loan obligations explained

Against a backdrop of geopolitical and economic volatility, collateralised loan obligations (CLOs) continue to navigate uncertainty and hold net asset values. flow explains the role of this remarkable asset class in Deutsche Bank’s Trust and Agency Services portfolio