-

Trade finance and lending, Macro and markets

What next for global energy?

22 April 2026

With a negotiated settlement to end the war in Iran not as yet confirmed, what does this mean for global trade with energy prices at current levels? flow’s Clarissa Dann examines insights from Deutsche Bank Research and key international agencies and reflects on what this means for trade finance demand

MINUTES min read

Between 2–6 April, a total of 15 tankers with a combined Deadweight Tonnage (DWT) of 1274K crossed the Strait of Hormuz, averaging three tankers and 255K DWT daily. This, noted Deutsche Bank Research in their dbDataInsights tracker of 7 April, “is a sharp increase from the March daily average of 82K DWT but still represents around 93% shortfall compared to pre-war levels”.1

Such events are a reminder of how crude oil pricing impacts the global economy and economic development as the world’s dominant energy source. As UNCTAD put it on 1 April, “Trade started 2026 on a strong footing but is expected to lose momentum as the year progresses. Growth in global merchandise trade is projected to decelerate from about 4.7% in 2025 to between 1.5% and 2.5% in 2026, as global demand weakens and uncertainty rises.”2

“Energy is at the heart of today’s geopolitical tensions”

Increasing demand for energy

Global demand for energy has grown by nearly 60% since 2000, with all the increase coming in emerging market and developing economies. All major energy sources grew over the period, stated the International Energy Agency (IEA) in its World Energy Outlook 2025 (12 November 2025).3 Although published more than three months before hostilities began in Iran, the IEA point that “pressing threats and longer-term hazards are elevating energy to a core issue of economic and national security” seems almost prophetic.

“Energy is at the heart of today’s geopolitical tensions, with traditional risks to fuel supply now accompanied by restrictions affecting supplies of critical minerals,” it adds, as a reminder that a transition to clean energy is dependent on those critical minerals supply chains. The flow article ‘Mining tomorrow’s energy infrastructure’ (26 June 2024), drawing on Wood Mackenzie data, seems all the more pertinent despite being published almost two years ago.

Emergency response

On 11 March, IEA member countries agreed to make 400 million barrels of emergency oil stocks available4 – the largest-ever release coordinated by the IEA. Previous collective actions were taken in 1991, 2005, 2011, and twice in 2022. The heads of the IEA, International Monetary Fund (IMF), and World Bank Group went on to announce the formation of a coordination group to maximise their institutions’ responses to the energy and economic impacts of the war in the Middle East on 1 April.5

In their joint statement, they point out how the conflict disproportionately affects energy importers – in particular low-income countries”. Its impact is, according to the agencies, “already transmitted through higher oil, gas and fertilisers prices, and is triggering concerns about food prices as well”.

In addition, global supply chains – including of helium, phosphate, aluminium, and other commodities – are affected, as is tourism due to flight disruptions at key Gulf hubs. “The resulting market volatility, weakening of currencies in emerging economies, and concerns about inflation expectations raise the prospect of tighter monetary stances and weaker growth,” says the statement.

Manageable economic shock?

In their Global Economics Monthly Flyover (24 March), the Deutsche Bank Research team note that “at current prices, the energy spike represents a material but manageable shock to the global economy, taking off slightly under 0.5 percentage points from global growth while adding one percentage point to inflation.”

But they warn, “oil prices nearing US$150/bbl would likely push the Euro Area and Japan into brief recessions and lead to stagflation across much of Asia”. To put it more starkly, they explain, “if the Strait of Hormuz traffic does not effectively re-open over the course of 2026, a global recession is likely to ensue as the required demand destruction intensifies.”

The variation of the impact across regions is also something the report highlights – in line with the IEA, IMF and World Bank Group statement. The Deutsche Bank Research team note that the US, as a net energy exporter, “is less exposed to a growth shock but faces a larger inflation impulse than most countries”. Deutsche Bank Research’s US Chief Economist Matthew Luzzetti projects Q4/Q4 2026 growth of 2.4% with the caveat that “rising oil prices pose a downside risk”.

For the Euro Area – reliant on energy imports, with baseline projects based on US$100/bbl Brent pricing – the team have reduced their 2026 GDP view from +1.1% to +0.5% “as the energy shock pushes the economy towards stagnation over the summer”.

A subsequent Deutsche Bank Research report published on 14 April makes the point that Europe’s structural vulnerability because of the crisis is twofold. “The direct part (trade exposure to Gulf countries on crude oil, gas, oil derivatives, chemicals and metals) is tangible.” However, energy that arrives embedded within industrial inputs with a precise fit in supply chains is much harder to substitute than fungible commodities such as oil or natural gas, for which Europe’s sourcing has already shifted to other suppliers.6

While in Europe the energy shock, they note, “is first and foremost a price shock”, Asia is more directly exposed “given it is the primary buyer of oil and LNG exports from the Middle East”.

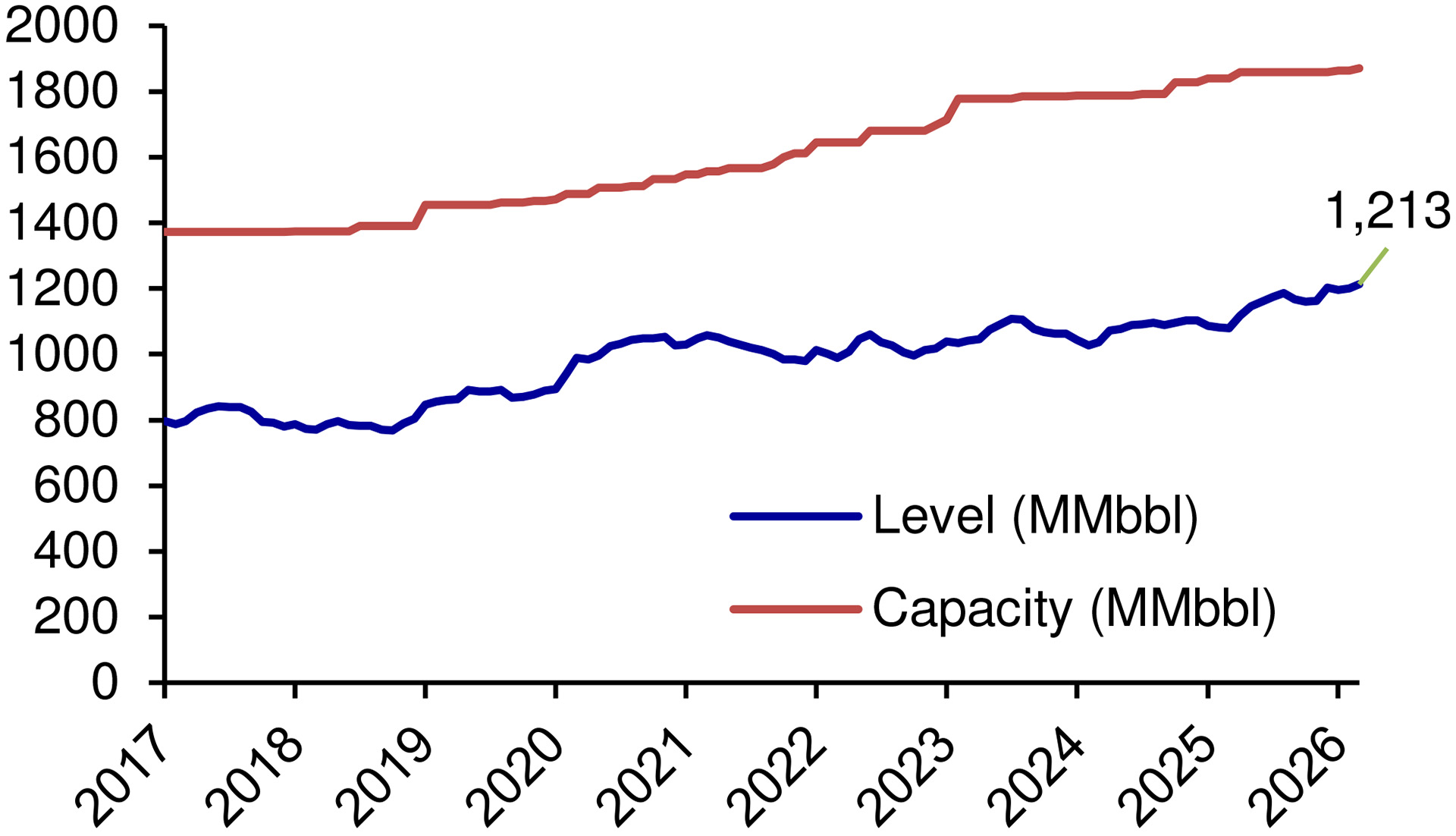

Yi Xiong, Deutsche Bank Research China Chief Economist points out that “China’s overall less reliance on oil and gas (26% of total energy supply compared with 52% in the world) and high oil reserves (see Figure 1) “could help maintain the economy’s resilience and potentially boost global demand for its renewable energy sector”.

Figure 1: China total oil reserves including commercial, SPR and refinery facilities

Source: Kpler, Deutsche Bank (from Hsueh on oil, Deutsche Bank Research, 31 March 2026)

Increased trade finance demand

From a trade finance perspective, periods of energy-driven volatility amid geopolitical stress typically increase clients’ need for liquidity, payment certainty, inventory availability and robust risk mitigation.

Trade finance is often most relevant precisely where an energy shock is felt most acutely. As counterparties come under greater pressure and supply chains become longer and more expensive, working capital tends to get tied up in goods in transit and higher inventory buffers. This combination can strain cash flows and make firms more sensitive to both timing and performance risk.

In such an environment, the demand for payment certainty rises first. Clients therefore place greater value on solutions that reduce settlement uncertainty and strengthen contractual performance, most notably letters of credit and guarantees. Depending on the risk set‑up, guarantees can be issued on an unsecured basis or supported by financial collateral.

“As volatility increases and sourcing shifts to new geographies, well-structured transactions… become even more important”

“As volatility increases and sourcing shifts to new geographies, well-structured transactions, appropriate collateralisation, and enhanced country and counterparty risk assessment become even more important to ensure that obligations are met as agreed,” explains Guenther Poettler, Global Head of Trade Finance & Lending Structuring and Syndication, Deutsche Bank.

At the same time, higher energy and transportation costs can extend the cash conversion cycle and increase pre-financing needs. This drives demand for funding solutions that release liquidity without disrupting commercial relationships. By combining export and commodity finance with supply chain finance – including receivables, payables and inventory finance – clients can free up cash, make payment terms more resilient and support suppliers throughout the supply chain. Where critical dependencies sit beyond Tier‑1 suppliers, deep‑tier SCF can extend this support beyond direct suppliers by tying funding to identifiable supply‑chain invoices/flows and anchoring the risk set‑up closer to the buyers.

Taken together, these dynamics make trade finance a critical tool to protect performance, unlock liquidity, and keep supply chains moving in volatile energy-driven markets.

Deutsche Bank Research reports referenced

Global Economics Monthly Flyover (24 March), by Peter Sidorov and Jim Reid

Hsueh on oil, Deutsche Bank Research, (31 March 2026) by Michael Hsueh

Gulf shipping tracker & global response, 7 April edition, by Debbie Jones and Jim Reid

Beyond the barrel – Europe’s hidden energy vulnerability, 14 April, by Yacine Rouimi and Mark Wall

Sources

1 Gulf shipping tracker & global response, 7 April edition, Deutsche Bank Research

2 See Hormuz disruption deepens global economic strain across trade, prices and finance at unctad.org

3 See Executive summary at iea.org

4 See IEA Member countries to carry out largest ever oil stock release amid market disruptions from Middle East conflict at iea.org

5 See Joint Statement by the Heads of the International Energy Agency, International Monetary Fund, and World Bank Group at iea.org

6 See Beyond the barrel: Europe's hidden energy vulnerability at dbresearch.com

You might be interested in

Trade finance and lending, Macro and markets

Commodities Outlook 2026 – where next Commodities Outlook 2026 – where next

Copper is up, oil down, but amid the uncertainty and volatility that characterises the current geopolitical landscape there is one constant – China. As the world’s second biggest economy enters its year of the Fire Horse, flow’s Will Monroe shares key updates from Deutsche Bank Research’s Commodities Outlook, where supply and demand is clearly linked to what China might do next

Trade finance and lending, Opinion

After Draghi: what’s next for Europe’s economy? After Draghi: what’s next for Europe’s economy?

Competitiveness, resilience or preparedness – the big imponderables for European trade in 2026. Independent trade economist Dr Rebecca Harding explains why diverse and resilient supply chains are key – and how these should be financed

Macro and markets, Trade finance and lending

The world outlook 2026 – never a dull moment The world outlook 2026 – never a dull moment

Drawing on the Deutsche Bank Research annual next-year World Outlook, flow looks forward to a year of cautious optimism, with growth accelerated by AI adoption, clearer trade strategies, fiscal stimuli, and investment in security and infrastructure