-

Trust and Securities Services

Europe’s T+1 transition: lessons, readiness and what firms need now

6 May 2026

With Europe’s October 2027 T+1 transition deadline now firmly in scope – and its practical complexities crystallising – flow securities services correspondent Janet du Chenne meets the Deutsche Bank Trust and Securities Services team translating US lessons, internal readiness work and industry guidance into coordinated client action

MINUTES min read

The European Commission’s amendment to the Central Securities Depositories Regulation (CSDR)1 to effect T+1 securities settlement grounded the 11 October 2027 transition deadline in reality. Unlike the US – where a single Securities and Exchange Commission (SEC) rule set the 28 May 2024 countdown in motion – Europe’s ticking clock requires alignment across 27 markets and numerous CSDs, some with their own infrastructure, regulatory nuances, and cut-off times.

The flow article ‘Europe braces for T+1’ mapped that landscape and the high-level recommendations2 from the EU T+1 Industry Committee, published in June 2025. It framed 2026 as the year of readiness and 2027 for structured testing – as outlined in the European industry-wide testing plan for the EU, UK and Switzerland, published in March3 – and underscored the core risk: compressed timelines increase failure likelihood, and automation must be paired with collaboration. With less than 18 months to go – and impact assessments showing what that pairing looks like in practice – this article highlights some of the key emerging takeaways for industry participants.

US lessons revisited in 2026

In the US, automated post-trade solutions – real-time trade matching, streamlined allocation and affirmation – proved decisive. The Depository Trust & Clearing Corporation recorded affirmation rates above 90% in the days after go-live.4

"Early and comprehensive testing is absolutely essential," says Fiona Neville, Head of Custody & Fund Services Europe, Deutsche Bank. "In the US, firms that tested early and thoroughly had far smoother transitions. And as we saw in the US, firms cannot solely rely on hiring additional staff to manage the change. Europe must approach this with automation from day one."

The joint EU-UK-Switzerland T+1 industry testing plan brings structure to that imperative, alongside the EU T+1 implementation handbook,5 and market practices harmonising standing settlement instructions (SSIs)6 – including a market practice on PSET and PSAF, SSI Management and Exchange Market Practice and a Transaction Type Market Practice – and partial settlement,7 and settlement optimisation guidance for securities finance transactions (SFTs).8

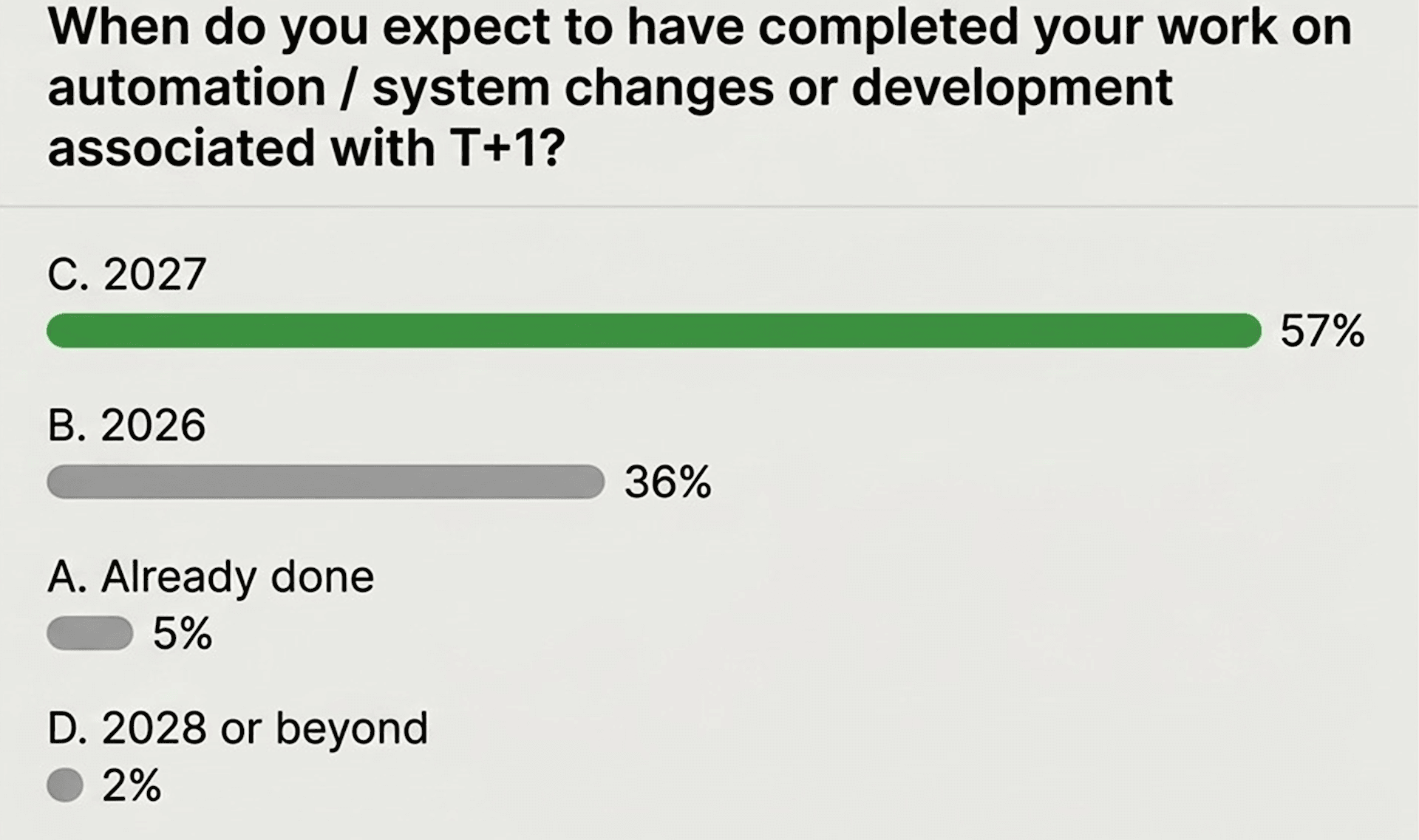

Building on a September 2025 Value Exchange survey that found 77% of firms are actively engaged in the project,9 an audience poll at the testing plan launch event found 57% of firms expect to complete automation and systems work in 2027, with 36% targeting 2026. See Figure 1.

Figure 1: Automation and systems changes work expected in 2026/2027

Source: Joint EU-UK-CH Industry Testing Plan launch event hosted by EU T+1 Industry Committee, the UK Accelerated Settlement Taskforce, the Swiss Securities Post-Trade Council, and Capco, March 2026

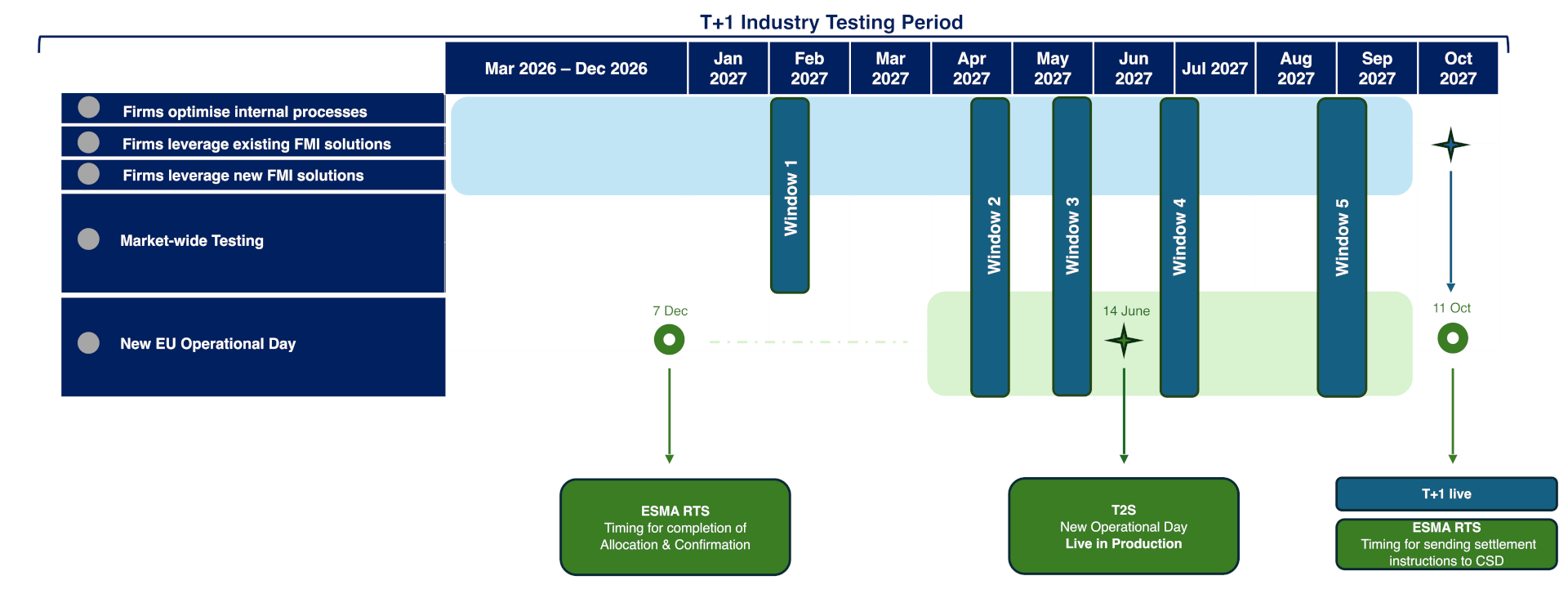

It’s here that the interdependencies between internal readiness and national market testing surface in five testing windows (see Figure 2).

“In short, this requires unprecedented cross‑jurisdictional coordination. But the awareness of that complexity gives us confidence – everyone understands what’s at stake,” adds Neville.

Figure 2: Internal readiness and five market-wide testing windows

Source: EU/UK/CH T+1 Industry Testing Plan, 25 March 2026 – EU T+1 Industry Committee, UK Accelerated Settlement Taskforce, and Swiss Securities Post-Trade Council T+1 Task Force

What clients are saying, and the key takeaways

Britta Woernle, Head of Market Advocacy Europe – Trust and Securities Services, Deutsche Bank, notes, "Larger market participants, active in multiple markets, want further process harmonisation because they’ve experienced it with T2S and seen the importance of harmonising across markets for efficient cross-border settlement. Smaller, more domestic-focused institutions expect their custodians to shield and guide them through the change.”

The level of preparedness varies sharply, observes Neville. Large global institutions are well advanced, while mid-tier firms are assessing impacts and planning technology uplift. Smaller firms are relying heavily on custodians for guidance to understand impacts and practical steps.

“There was a deluge of information early on, but clients now want actionable insight: checklists, practical steps, and clarity and guidance on what they should be doing now,” says Neville. Testing support, connectivity, infrastructure readiness, risk management and ISO 20022 are top of the agenda.

The bank is steering clients towards what they can do immediately via internal process reviews, preparing for bilateral connectivity in 2026, and gearing up for multi-national testing and market‑wide dress rehearsals in 2027.

While most clients understand the level of readiness required, many are still looking for a trusted guide to support them through the process. “We’re tailoring our approach accordingly; sharing our knowledge and experience to support and guide them through this transformation,” she reflects.

How other regulatory changes reinforce T+1

Settlement discipline, T2S operational changes, and SFT rules are all moving in parallel – and all reinforce the case for acting now.

The European Securities and Markets Authority (ESMA) has amended several regulatory technical standard elements to support a successful T+1:

- Allocation and confirmation deadlines have been fixed at 23:00 CET on trade date;

- SSIs must be exchanged in standardised, machine-readable formats;

- Place of settlement becomes mandatory in written allocations; and

- Settlement instructions must be submitted by 23:59 CET on trade date; and all CSDs must offer partial settlement and hold/release functionality in the settlement process.

The European Central Bank has redesigned the T2S operational timetable so that the first meaningful settlement cycle begins at midnight on T+1. This is essential because European exchanges trade late (some until 22:00 CET), then the clearing houses, or central clearing counterparties, need time to process and instruct. According to Woernle, T2S CR-858 for the adjustment of the night-time settlement for accommodating the shortening of the settlement cycle to T+1 was authorised by the T2S CSD Steering Group and will be available in T2S with the June 2027 release, pending approval of the ECB T2S Market Infrastructure Board.

In the same release, the new dedicated T2S gating event process10 might be implemented pending approval by the T2S governance. In parallel, SWIFT has agreed on a fast-track Change Request for a new dedicated field in SR2026 (November 2026), which is required for the SFT Settlement Optimisation Gating Event. A T+1 SFT market practice for the use of and participation in the gating event is currently being prepared by the EU Industry Committee. For SFTs, a new gating event11 will allow repo trades to benefit from technical netting and optimisation during daytime settlement on T+1, limiting the need for cash resources and preventing a sharp rise in liquidity costs. Further clarifications on partial settlement opt-outs are expected prior to the move to T+1.

“Firms that wait risk a costly scramble. The time to secure capability is now”

"Being proactive in managing all of those changes will ensure that we make the most of this moment," says Woernle. She makes the point that with T+1, ESMA settlement discipline, the T2S operating timetable, and the SFT changes are all interconnected. “You cannot manage one in isolation.”

"As we progress towards October 2027, resources, particularly external expertise, will become scarce," adds Neville. "We saw this with UCITS and other major shifts. Firms that wait risk a costly scramble. The time to secure capability is now.”

How Deutsche Bank is supporting clients

Deutsche Bank’s T+1 programme spans the Corporate Bank, Investment Bank, and other business areas. A central client webpage – a repository of aligned messaging, progress updates, and clear accountability (including tasks owned by Deutsche Bank and what it needs from clients) – is in development and set to be published in due course. Relationship managers will coordinate outreach, with clients segmented to avoid multiple uncoordinated touchpoints.

“To date, we have focused on our own impact analysis; documenting, planning and developing as needed to address any dependencies,” explains Neville. “Our internal impact assessments have provided us with practical insights we can share. We’re now helping clients review operating models and identify their own potential bottlenecks and solutions.”

Deutsche Bank is actively engaged in industry forums, working groups, and panels, and is encouraging clients to focus on:

- Cross-jurisdictional nuances and their operational implications;

- Liquidity and FX impacts, given the scale of re-engineering required;

- Operational resilience and robust exception-handling processes; and

- Seeing T+1 as a catalyst for broader transformation – compliance now, but with an eye on what 2027 demands.

Neville stresses that 2026 is the year to complete as much internal testing as possible – Pillar 1 – so that firms can fully leverage the five market-wide testing windows in 2027 (Pillar 2).

"We’re very much in action now," she concludes. "Momentum is there. We’re talking practical application, not theoretical, and that’s exactly where we need to be."

Five key points for clients

- Robust real-time data management is essential

- A proactive testing plan. Use 2026 for internal process review and bilateral connectivity; use 2027’s market-wide windows for end-to-end and dress rehearsals

- Invest in your workforce. Staff must be proficient in new processes and tools – especially exception handling – in ways they haven’t previously needed to be

- Automate wherever possible

- Communicate early. T+1 is a network effort and you’re therefore only as strong as the weakest link in your settlement chain

Janet Du Chenne is a freelance financial journalist and a former Co-Editor of flow and of Global Custodian

Sources

1 See Commission proposes to shorten settlement cycle for EU securities from two days to one at ec.europa.eu

2 See High-level roadmap to t+1 securities settlement in the EU at eu-t1.eu

3 See EU/UK/CH T+1 Industry Testing Plan, 25 March 2026 at acceleratedsettlement.co.uk

4 See DTCC Comments on Industry’s T+1 Progress at dtcc.com

5 See EU T+1 Securities Settlement Handbook at eu-t1.eu

6 See EU T+1 Industry Committee SSI Task Force – SSI Market Practice at eu-t1.eu

7 See EU T+1 Industry Committee Taskforce on Partial settlement Market Practice – Final report at eu-t1.eu

8 See EU T+1 Industry Committee SFT Settlement optimisation TF Report at eu-t1.eu

9 See EU T+1 Industry Committee Readiness Survey – ValueExchange Key Findings at thevx.io

10 See T2S-0865-URD Dedicated T2S gating event to optimise settlement resources in the context of the move to T+1 at ecb.europa.eu

11 See EU T+1 Industry Committee SFT Settlement optimisation TF Report at eu-t1.eu

You might be interested in

Securities services, Macro and markets

Rethinking investment and post-trade in Asia Rethinking investment and post-trade in Asia

As Asia continues to attract investor attention for its high growth and promising returns, how is post-trade keeping pace in a shifting global economic landscape shaped by tariff shocks? flow shares key takeaways from a seminar hosted by The Asset in association with Deutsche Bank

Securities services {icon-book}

Euroclear and tomorrow’s capital markets trades Euroclear and tomorrow’s capital markets trades

Becoming a next-generation financial market infrastructure requires balance. Euroclear CEO Valérie Urbain spoke to Janet Du Chenne about how she’s doubling down on client-centricity and innovation while retaining the company’s DNA as a trusted settlement engine in capital markets

Cash management, Trust and securities services

Working with NBFIs Working with NBFIs

Non-bank financial institutions (NBFIs) and the rapid growth of private markets offer investors an opportunity to diversify their portfolios, but what do they need in order to work safely within the financial system? flow’s Clarissa Dann and treasury correspondent Graham Buck set out the NBFI landscape and explain how regulated banks are supporting them