-

flow case studies, Trust and securities services

Redaptive: meeting corporate demand in an energy-hungry era

13 July 2026

Could the Energy-as-a Service industry represent the future of energy supply for large companies? flow’s Will Monroe scopes out US-based Redaptive’s business model and the innovative financing solutions that have helped the company to scale

MINUTES min read

Picture the scene. It’s winter in Denver, Colorado. A homeowner manually turns off their heating and hot water before leaving the house, to reduce their energy bill. Lastly, they remember to flick off the light switch as they walk out into the crisp chill of a January evening.

Now scale the behaviour of that one homeowner to a multinational corporation operating thousands of facilities worldwide. In addition to lighting and heating, electricity powers production lines, data centres, and other energy-intensive critical infrastructure. Companies that fail to ‘turn off the light’ stand to pay the price over the long run, with even marginal inefficiencies translating into millions of dollars in additional costs on balance sheets.

To get an idea of the potential savings on offer, it’s worth looking at the numbers. For a start, corporates aren’t immune from the global energy price rises that are currently affecting residential consumers. According to the US Energy Information Administration, commercial electricity prices increased by 4.8% year-on-year in April 2026, while industrial electricity prices rose by 5.5% over the same period.1 Over the five-year period from 2020–2025, commercial prices were up 26.6%, with industrial prices rising by more than 29%.2

Recent geopolitical pressures in the Middle East, and corresponding price shocks, are contributing factors. But while such pressures tend to be cyclical, the rapid expansion of artificial intelligence (AI) and cloud computing represents a structural shift – fuelling an unprecedented build-out of data centres and placing considerable strain on power grids (see the flow article, ‘How AI is reshaping the energy transition’).

BloombergNEF estimates that data centre power demand in the US alone will hit 106 gigawatts (GW) by 2035 – a 2.7-times increase on the 40 GW seen in 2025 – with demand easily set to outstrip supply based on current projections.3

This rising demand is compounded by the ongoing electrification of transportation, the proliferation of electric vehicle (EV) charging networks – see the flow case study ‘E.ON Drive: streamlining payments for EV charging’ – and the continued expansion of energy-intensive industries. Taken together, consulting and technology services firm ICF projects that overall US electricity demand will increase 25% by 2030 and 78% by 2050, compared with 2023 levels.4

Add ageing infrastructure into the mix and the scale of the challenge becomes clear. Many corporates are grappling with ageing and inefficient infrastructure, which contributes to higher energy consumption and elevated maintenance costs. A Redaptive white paper, (January 2026), says the US Department of Energy estimates that more than US$1.5trn in maintenance has been deferred across US commercial and industrial facilities.5

One option is to upgrade infrastructure and improve efficiency, harnessing advances in digital technologies. These include smart meters, IoT sensors, building management systems and cloud-based analytics, making it possible to track, measure, and optimise energy consumption accurately. But modernisation efforts require substantial upfront investment. How do corporates reconcile the need to reduce energy costs, without diverting capital away from core business priorities? The Energy-as-a-Service (EaaS) model could provide some of the answers.

Energy-as-a-Service explained

Infrastructure modernisation initiatives often compete with core business investments for both funding and internal resources, which can lead to delayed implementation and higher overall costs. The EaaS sector seeks to address this via a business model that enables corporates to access energy solutions without the burden of ownership and upfront capital expenditure.

Unlike traditional utility supplies, where energy is bought as a commodity at a fixed or variable rate, EaaS operates more like a ‘subscription’. The service provider finances, installs, manages, and maintains energy systems, and customers make predictable, often performance-based payments. The outsourced solutions are tailored to a company’s specific energy goals and could include, for example, lighting upgrades or solar and battery storage systems.

EaaS contracts are typically structured so that dependency on providers and the corresponding risk is mitigated. Contracts tend to be long term, for example 10–15 years, with various performance guarantees, protections and exit provisions in place, while grid infrastructure and base supply remain with utility companies. In short, this means the provider can’t simply switch off the lights.

Estimates vary between research providers, but broad consensus values the global EaaS market between US$80–100bn as of 2025, with double-digit compound annual growth forecast over the coming decade.

Redaptive, a leading global EaaS provider with headquarters in Denver, Colorado is one of the organisations tapping into the increasing appetite for EaaS solutions from the C-suite. John Kerrigan, the company’s Head of Structured Finance, notes that “the business case for infrastructure modernisation has become structurally compelling in a way it simply wasn’t a decade ago”, with demand having “evolved from opportunistic to strategic”. In this environment an EaaS model historically positioned as a creative financing solution for sustainability teams is “increasingly a board-level conversation”.

“We set out to turn infrastructure from a cost centre into a growth lever”

‘Infrastructure monetisation’

Redaptive was founded in 2015 with a focus on fixing what Kerrigan defines as a persistent market failure: “large commercial and industrial organisations were sitting on enormous potential energy savings but failing to capture them. So, we set out to turn infrastructure from a cost centre into a growth lever.”

Redaptive developed a full-service platform to modernise energy infrastructure at large multinationals, based on the premise of ‘infrastructure monetisation’, a tagline that speaks to the cost benefits of the offering. Financing, project development, installation, and ongoing measurement are packaged up into one single contracted outcome. The company funds and executes portfolio-wide upgrades for clients across a range of technologies, including energy-efficient lighting, heating, ventilation, and air conditioning (HVAC) systems and controls, and on-site generation such as solar, battery storage and microgrids.

Clients – who span sectors including industrial, real estate and healthcare – repay the investment through a fixed or performance-linked fee over an agreed period. This pivot from capital expenditure to operating expenditure aims to reduce balance-sheet impact, helping companies to modernise critical infrastructure without diverting funds away from core business priorities.

Sustainability reporting forms an important part of the business model. Redaptive’s service generates real-time energy, emissions and performance analytics, as well as audit-ready ESG documentation at a granular level to satisfy reporting frameworks including California’s climate disclosure laws, EU’s Corporate Sustainability Reporting Directive (CSRD) obligations flowing through to US subsidiaries, and investor and lender ESG requirements embedded in credit agreements and fund mandates. “This is increasingly important as corporate sustainability commitments shift from aspirational to auditable,” Kerrigan confirms.

A business model refined across thousands of sites and hundreds of Fortune 500 relationships is underpinned by a proprietary data platform measuring real-world performance at the asset level. To date, Redaptive has completed more than 12,000 client projects delivering a total of U$353m in energy savings, with US$1.2bn in capital deployed.6

EaaS in action

Gaurav Loya, a director on the Structured Finance team at Redaptive, points to the company’s partnership with Iron Mountain7 – an enterprise information management services organisation with a presence in 50 countries and three continents – as a measure of what can be achieved from both a costs and sustainability perspective.

An ambitious plan saw Redaptive replace outdated and inefficient fluorescent lighting across 428 locations.8 The LED retrofit programme update was completed in just two years, without disrupting the company’s complex, fully operational facilities.

In addition to delivering US$95m gross savings at no upfront cost to Iron Mountain, the reduced electricity consumption will avoid nearly 178,000 metric tons of CO₂ emissions over the next 10 years – the equivalent of the emissions from 34,630 private homes.9 For data giant Iron Mountain, which has more than 30 energy-hungry data centres in its portfolio, this is a significant energy and cost saver.

Figure 1: Redaptive’s Iron Mountain partnership in numbers

- Locations: 428

- Fixtures upgraded: 310,000

- Annual savings: US$6.5m

- Total savings*: US$95m

- 10-year reduction in kWh: 668 million

- Metric tonnes of CO2 emissions avoided*: 204,000

*Over the whole service term

Financing infrastructure modernisation

A business model designed to eliminate upfront costs for customers must, however, absorb them elsewhere. For Redaptive, this meant securing the financing muscle that would allow it to continue to support existing clients, while scaling the business.

To advance these ambitions, Redaptive first partnered with Deutsche Bank in the summer of 2023, securing US$125m in financing from Deutsche Bank’s US Private Credit & Infrastructure group for a committed warehouse facility. The facility supported the deployment of metering, HVAC, solar, LED, EV, and other efficiency and sustainability solutions. Deutsche Bank’s New York branch was appointed as facility agent, while Deutsche Bank Trust and Securities Services (TSS) was selected as account bank and verification agent, establishing a strong foundation for collaboration.

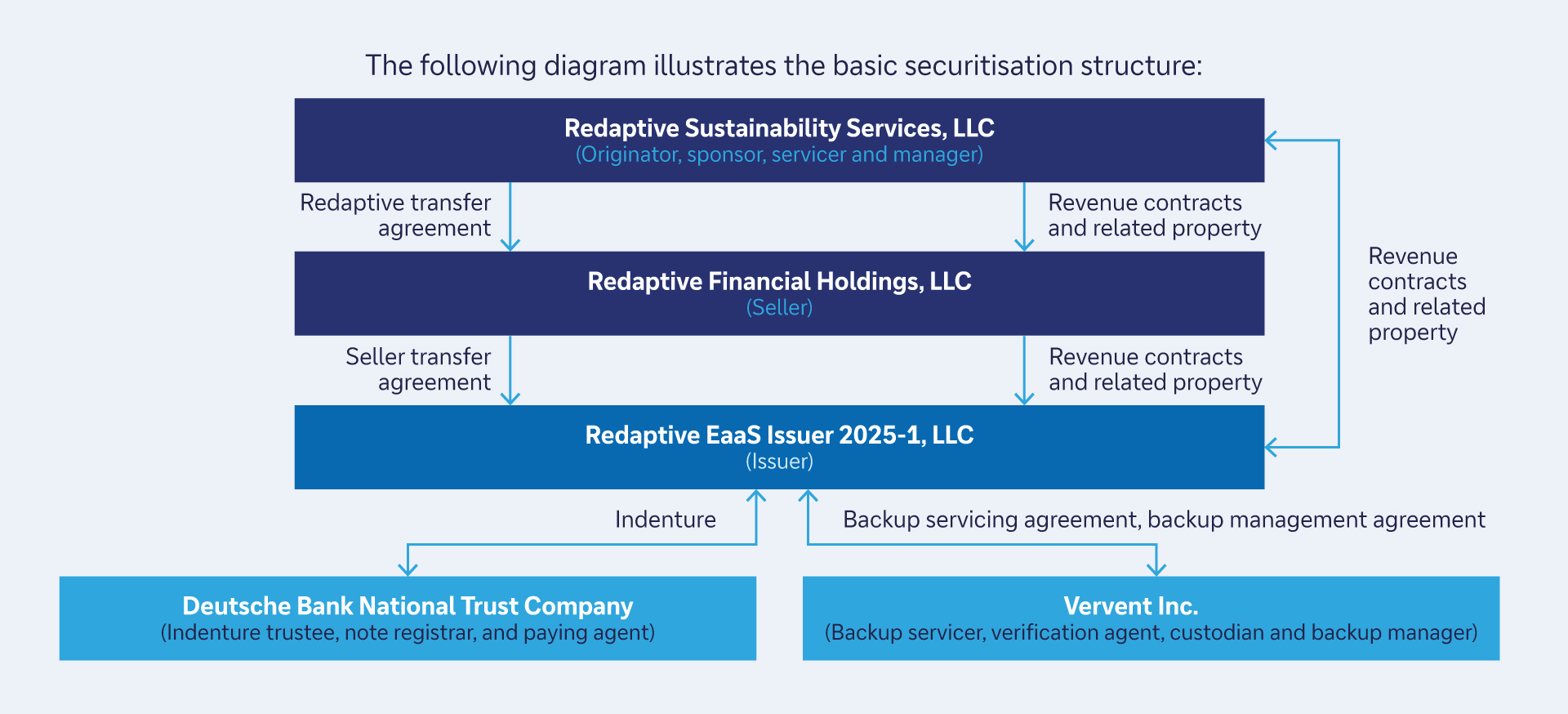

Building on this relationship, Redaptive once again turned to Deutsche Bank when it sought to execute its inaugural asset-backed securitisation (ABS) – a step Loya describes as “the natural maturation of our funding model”. The securitisation, which raised US$216m in financing, was the first of its kind for the EaaS sector and was underwritten and structured by the bank’s Securities team, while Deutsche Bank’s TSS team served as indenture trustee, registrar and paying agent on the landmark deal.10

Figure 2: Summary of Redaptive’s ABS transaction structure

Source: Redaptive

An ABS sees a pool of income-generating assets packaged and sold to investors as tradable securities, enabling companies to convert future cash flows into immediate capital. The Redaptive EAAS Issuer 2025-1 transaction, completed in December 2025, was backed by a portfolio of long-term energy efficiency agreements with Fortune 500 commercial and industrial companies.11

This included 1,445 leases to 46 obligors with the geographically diversified portfolio spanning all 50 US states, Puerto Rico, Hawaii, as well as Germany, Canada, and Ireland.12 The contracts support critical infrastructure, including lighting, HVAC and control systems, with Redaptive receiving contracted payments in return for owning and maintaining the equipment.

“Taking the EaaS asset class in the commercial and industrial space to the institutional capital markets for the first time was a genuinely novel undertaking,” Kerrigan explains. “We needed a partner with the structural finance expertise to appreciate the credit characteristics of long-term EaaS performance contracts. Deutsche Bank’s Trust and Securities Services team brought the operational rigour and institutional credibility that investors in a first-of-its-kind EaaS ABS needed to see.”

Paul Maley, Global Head of TSS at Deutsche Bank, notes: “We were delighted to work with Redaptive on this landmark transaction – which has had no direct precedent in the ABS market – as trustee, registrar and paying agent, working closely alongside our colleagues from Deutsche Bank’s asset-backed securities team. This partnership demonstrates our commitment to providing clients with world-class service in the energy infrastructure sector.”

“This landmark transaction has had no direct precedent in the ABS market”

Financing the future

The structural conditions driving energy demand both in the US and globally – including data centre build outs, grid pressures, and ageing infrastructure – are only set to intensify over the coming years.

When it comes to data centre energy consumption, in particular, the figures are staggering. A December 2024 paper published by the Berkeley Lab, 2024 United States Data Center Energy Usage Report13, tracks this rise over the previous decade. Back in 2018, US data centres consumed about 76 terawatt-hours (TWh), representing 1.9% of total annual electricity usage across the country. Fast forward a decade to 2028 and the Berkely Lab forecasts a top range estimate of 580 TWh, accounting for 12% of total US electricity usage – a more than sixfold increase.

And data centre consumption forms just one facet of the energy demand juggernaut. It’s easy to see, therefore, why Redaptive believes a cycle of rising energy costs is baked in for the long term: “Factors such as AI workloads and electrification are driving a step-change in grid load,” Kerrigan states. “Energy costs are rising faster than most financial models assumed. The 2–3% electricity inflation assumption that underpinned most corporates’ long-range financial planning is now materially wrong.” In other words, this is not a cycle that will correct, but a structural repricing event.

Against this backdrop, Redaptive envisions a unique market opportunity that could see outcome-based infrastructure financing become the default model for large commercial and industrial organisations, rather than the exception.

Could the company’s recent securitisation represent a potential blueprint for scaling EaaS globally? Kerrigan believes so: “It established the proof of concept for institutional capital markets participation in EaaS at scale. We expect that template to catalyse a significant expansion of the capital available to finance the energy and infrastructure transition – it’s ultimately a beginning rather than a conclusion.”

To find out more about Deutsche Bank’s ABS agency services and solutions click here.

Sources

1 As measured by calculating average retail revenues per kWh. See Electricity Monthly Update at eia.gov

2 See Electricity data browser - Average retail price of electricity at eia.gov

3 See AI and the Power Grid: Where the Rubber Meets the Road at about.bnef.com

4 See Electricity demand growth: How will the grid keep pace? at icf.com

5 See The Infrastructure Gap: Why Enterprise Modernization Needs a New Model at redaptive.com

6 See redaptive.com

7 See Iron Mountain saves $101.7M with 10-year facility modernization program at redaptive.com

8 See Iron Mountain saves $101.7M with 10-year facility modernization program at redaptive.com

9 See Iron Mountain saves $101.7M with 10-year facility modernization program at redaptive.com

10 See Redaptive Closes $216M Securitization — A First for Energy-as-a-Service at redaptive.com

11 See Redaptive Closes $216M Securitization — A First for Energy-as-a-Service at redaptive.com

12 See KBRA Assigns Preliminary Ratings to Redaptive EAAS Issuer 2025-1, LLC at kbra.com

13 See 2024 United States Data Center Energy Usage Report at escholarship.org

You might be interested in

Sustainable finance, Technology {icon-book}

How AI is reshaping the energy transition How AI is reshaping the energy transition

As artificial intelligence (AI) drives innovation across sectors, it’s not only fuelling technological progress, but also significantly increasing electricity demand. Deutsche Bank’s Lavinia Bauerochse describes how this development is transforming the global energy transition – and why investments in grid expansion and transition finance are taking centre stage

Trust and agency services, Sustainable finance {icon-book}

Greening the night with the SunZia Wind and Transmission projects Greening the night with the SunZia Wind and Transmission projects

US renewable energy company Pattern Energy is transforming the energy supply for three million Americans with its SunZia project. With insights from the company’s Project Finance and Corporate Development Director Carlyne Mickle and Deutsche Bank’s Trust and Agency Services team, flow’s Clarissa Dann tracks progress so far

Trade finance and lending, Macro and markets

What next for global energy? What next for global energy?

With a negotiated settlement to end the war in Iran not as yet confirmed, what does this mean for global trade with energy prices at current levels? flow’s Clarissa Dann examines insights from Deutsche Bank Research and key international agencies and reflects on what this means for trade finance demand