-

Cash management, Regulation, Macro and markets

Asian banks keep up to speed on ISO 20022 migration

July 2020

The new global language for financial communications is very much a work in progress. In this article written for The Asian Banker, Nancy So assesses how banks across the region measure up

This article was first published by The Asian Banker

Across the globe, Payment Market Infrastructures (PMI) are overhauling their systems to streamline their infrastructure with a single, common “language” for all financial communications. XML ISO 20022 appears to fit the bill. It not only provides much-needed data enrichment, from both a commercial and a regulatory perspective, but could also fulfil The long-anticipated goal of greater interoperability between various settlement networks.

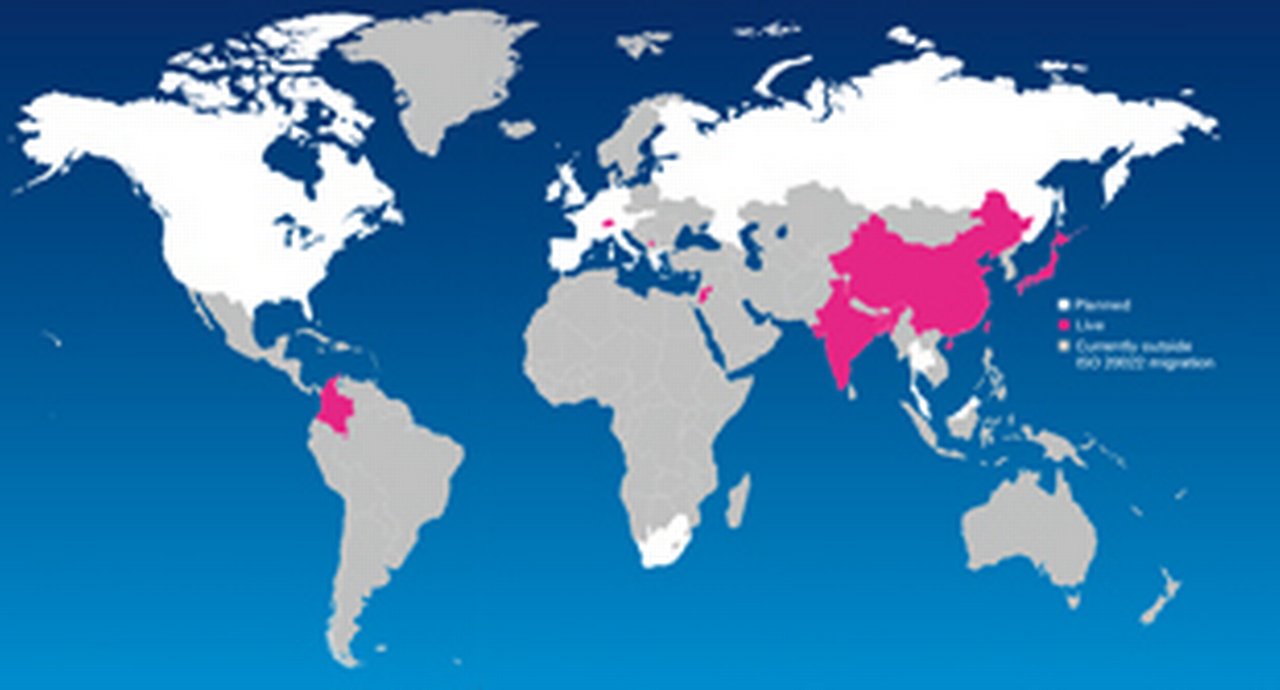

While major PMIs in the US (FedWire/CHIPS), the Eurozone (Target2/EBA Clearing) and the UK (CHAPS) have launched their respective ISO 20022 adoption projects, we have already seen actual live adoptions in Asia – most notably in China, Japan and India – with more to follow in the next few years. Additionally, SWIFT is pursuing its own network revamp towards ISO standards for its message categories 1, 2 and 9.

ISO 20022 migration significantly affects all banks – correspondent banking service providers and financial institution (FI) clients alike. So how are Asian banks approaching what has been dubbed “the payment industry’s greatest challenge since the introduction of the Euro – but also its greatest opportunity”? We take a closer look.

Degrees of awareness

At Deutsche Bank – the biggest EUR clearer in the world and a top USD clearer – we recently reached out via a survey to around 200 of our correspondent banking clients across 15 countries in Asia in order to better understand the Asian banks’ perspective and level of readiness.

On the one hand, the survey showed that the vast majority of Asian banks keep updated on XML ISO 20022 developments; mostly via information shared by their payment service providers and through public news. Further, 91% of respondents are aware of SWIFT’s migration programme. This clearly shows that Asian banks do recognise the importance of the migration and monitor developments in this space. The benefits are apparent to most as well; 64% agree that processing of cross-border payments will improve upon the ISO 20022 migration and 50% expect that the majority of market participants to be ISO 20022-ready by the end of 2022 ahead of the hard deadline in 2025, in order to fully benefit from rich structured data.

Yet on the other hand, are as many aware of the magnitude of changes to the EUR and USD payments services?

Less than a third of the respondents were aware of Europe (Target2/EBA Clearing) and US (Fedwire/CHIPS) migration projects respectively. That lower proportion is noteworthy, given the Asia-Pacific region boasts numerous banks – particularly from China, Singapore, India, Korea and Japan – that have direct access to these PMIs through their respective offshore entities. Some banks may just assume these projects to be less relevant for Asian FIs than they are for their EUR and USD correspondent banks.

Whilst that is surely the case, we still recommend that Asian banks keep abreast of these market infrastructure changes – directly or indirectly – via their EUR and USD correspondent banks. The latter are well situated to proactively play that role, as they are in full swing on their migration projects. Ultimately, the benefits are mutual if FI clients follow soon with their XML readiness. For instance, from a risk perspective it is fair to assume that no correspondent bank would be happy to take on the data truncation risk that derives from converting an MX message, containing rich data, into an MT format that cannot fit all that data, which would ultimately transfer liability for that data from receiver to sender. Consequently, this means increased reconciliation pain for the receiving bank – at a time when Asian banks are seeking more automation in back-office processes.

Looking more on the inside, only 26% could confirm that their organisations have begun their ISO 20022 migration programme. Half have only just started forming a project team, while the other half have projects in-flight, with the majority of this latter group taking a global approach to the transformation.

SWIFT sparks reassessment

With SWIFT having recently announced a delay to its migration deadline of one year, the survey finds that 58% of those who have begun their migration programmes feel that this hold-up will have a major impact on their organisations and they will need to reconsider their overall strategies. A noteworthy finding, given that SWIFT has stated that its decision will have little impact on banks’ decision to adopt ISO 20022 for market infrastructure initiatives and that the work already undertaken by the community – such as data remediation, channel improvements and back-office processing – has not been a wasted exercise.

"The adoption of XML ISO 20022 is not a question of ‘íf’ but rather ‘when’: the standard is here to stay globally."

At Deutsche Bank, our advice to clients is to continue on the migration project path, while always factoring in what resources and budgets allow for. The adoption of XML ISO 20022 is not a question of ‘íf’ but rather ‘when’: the standard is here to stay globally. Although some details will need to be clarified by the payment industry, banks should use this extra time to plan the implementation of ISO 20022 throughout their internal end-to-end processes in a strategic manner. This is key for FIs if they intend to benefit from the increased efficiencies of a standardised and data-enriched messaging format and ultimately improve client service. Adoption can also save costs by simplifying internal processes as well as potentially fulfilling more stringent Anti- Money Laundering (AML) reporting requirements with additional data fields in MX messages. The core tasks deemed relevant to the strategy, such as infrastructure investments, should then be accomplished in order to prevent sunk cost from unnecessary project interruption, to allow FIs to move forward with the migration.

On the flipside, almost half of the respondents stated that their organisations have not begun an ISO 20022 migration programme. Although each of them acknowledged that no correspondent bank would be able to handle their ISO requirements and they need to become actively engaged, 40% believe it is currently not a priority for their organisations, and 50% believe there is sufficient time to be ISO 20022-ready before SWIFT’s mandatory migration timeline expires in November 2025.

This wait-and-see approach could be fuelled by uncertainty. Our survey found that Asian FIs see a whole set of unknown challenges. The results offer something of a mixed bag; 39% of respondents believe tight investment budgets for enhancing internal systems and uncertainty on the committed migration timelines due to the impact of COVID-19 are of lowest concern – but 23% of them believe these same two factors are of the highest concern. However, what most of the respondents could agree on is the uncertain impact on payment processing resulting from different migration timelines by PMIs, which seems to be the most prominent concern. This sentiment is further underpinned by the expectation, held by 70% of respondents, that the industry as a whole may face many challenges during the first years of implementation, likely driven by a number of factors, including industry-wide data truncation and varying ISO specifications for different regions.

Conclusion

It is a positive sign that the majority of survey participants are aware of this global payment industry modernisation and recognise the long-term benefits. Asian banks that have seen their home market’s local PMIs already upgrade to ISO 20022 standards are ahead of the curve in the region (and some possibly globally) and are already making a valuable contribution to global industry working groups with their experience and subject matter expertise.

The uncertainties expressed in our survey come as little surprise and Asian banks are not alone in that respect. FIs across the globe are still attempting to grasp the magnitude of the impact on internal systems and operations with appropriate resource and budget allocation, in addition to enhancing their product offering to customers. Further, the COVID-19 pandemic is forcing banks to focus their resources on ensuring business continuity and supporting immediate client needs. So SWIFT’s one-year delay of the ISO 20022 transition process, along with its offer to provide in-network translation services, may bring relief to some. In the meantime, major correspondent banks should lead the way in continuing to service and advise their FI clients and share own experiences accordingly.

At Deutsche Bank, we are actively supporting our clients’ own migration strategies. Operationally, this includes continuing to accept SWIFT FIN MT messages and providing SWIFT FIN MT reporting during the coexistence period for their EUR/USD payments. We also still keep our Asian FI clients in the loop with market updates, white papers and our very own XML ISO 20022 migration approach.

This migration is just the first step towards operating in a new payments landscape that all FIs need to embrace. Over time, further benefits brought about by enhanced data attributes and infrastructure interoperability will follow. They range from enabling payment factories and payments- and collections-on-behalf-of (POBO/COBO) capabilities to enhanced business analytics and a contextual banking experience. Being first movers could provide considerable competitive advantage in this regard, opening up even more opportunities than the industry can imagine now. The march towards more seamless payment processing continues.

Nancy So

Managing Director, Head of Institutional Cash Sales and Client Management Asia Pacific, Deutsche Bank

Go to Corporate Bank EXPLORE MORE

Find out more about products and services

Go to Corporate Bank Go to Corporate Bank

Stay up-to-date with

Sign-up flow digest

Choose your preferred banking topics and we will send you updated emails based on your selection

Sign-up Sign-upYou might be interested in

CASH MANAGEMENT, TRADE FINANCE, SECURITIES SERVICES, TECHNOLOGY {icon-book}

Responsible innovation Responsible innovation

How can you connect four billion accounts across the world in an instant? That is the bold vision of SWIFT’s CEO, Javier Pérez-Tasso. flow's Clarissa Dann talks to him about the responsibilities vested in a cooperative founded to create mutual benefit for the financial community and why a virtual Sibos for 2020 will keep the global financial community engaged

CASH MANAGEMENT {icon-book}

ISO 20022 takes off ISO 20022 takes off

Many of the world’s most important payment market infrastructures are transforming to meet the needs of automation, integration and real-time services. All of this is underpinned by the migration to a new payments messaging standard – ISO 20022. For banks and corporates, this is more than just another IT project; it signals a major opportunity to improve payments processes and reassess business models. Paula Roels looks at the implications

CASH MANAGEMENT

Open banking unwrapped Open banking unwrapped

Neil Frederik Jensen joined the 5000 attendees of Money2020 in its new Amsterdam home and reports a sea-change in bank-fintech cooperation to deliver a better financial services experience to the end user