-

Cash management

Pollinating payments

June 2019

Amid a delicate ecosystem of de-risking and reducing correspondent banking lines, how can the process of making cross-border payments be improved? Ruth Wandhöfer and Barbara Casu have researched market participant pain points and suggest seven scenarios for the future

The ability to transfer money across borders in a safe and secure way is an indispensable requirement for the global economy. Until now, the main method of executing money transfers globally has been via correspondent banking arrangements.

In this article, which is based on the SWIFT Institute paper published in October 2018,1 we develop the building blocks for a future blueprint for cross-border payments, with a particular focus on the wholesale aspects of these flows, as they constitute a systemically important area of business. Cross-border payments, notes McKinsey (2016), “represent 20% of total transaction volumes in the payments industry, yet they generate 50% of its transaction-related revenues” (i.e. transaction-related fees, float income and FX fees), which amounted to more than US$350bn in global revenues in 2014.

How the industry sees correspondent banking today

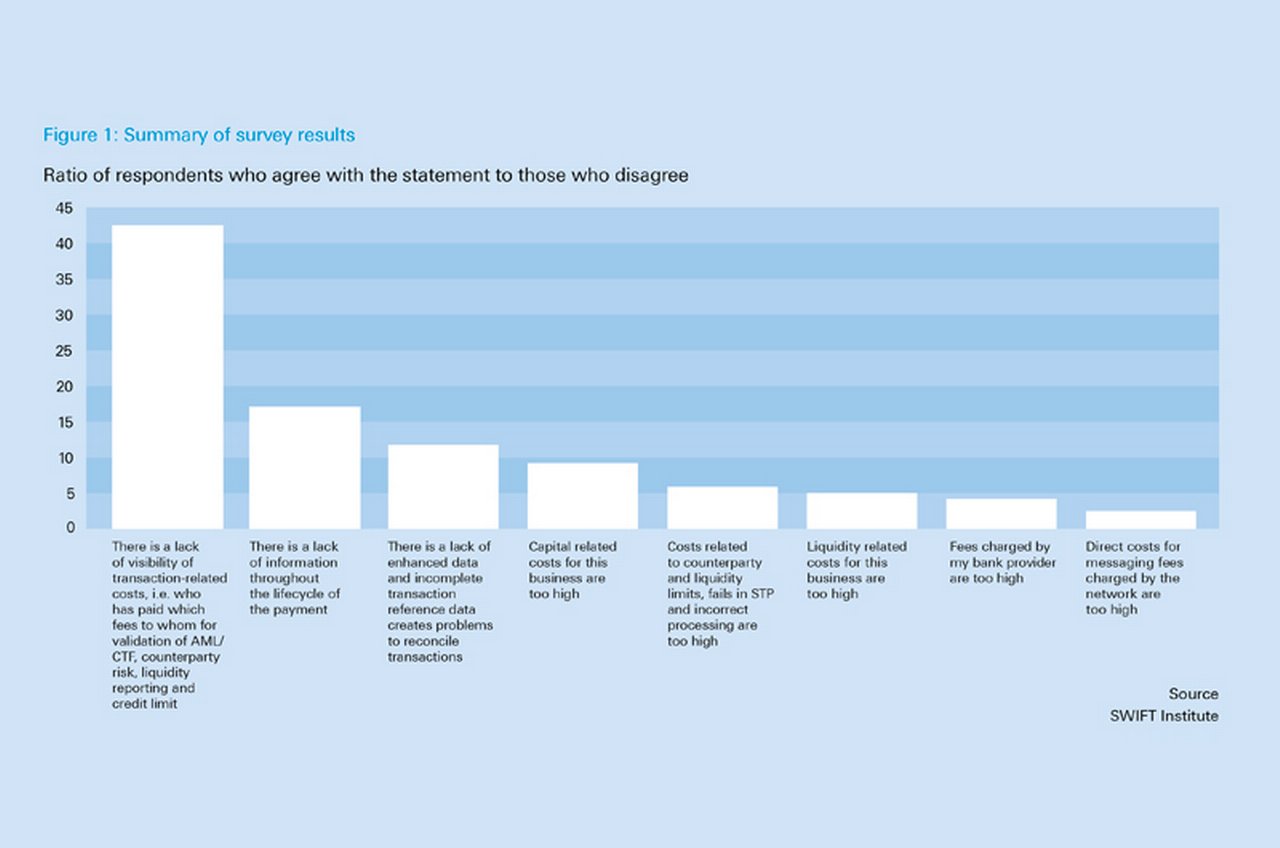

In order to identify pain points in correspondent banking, we decided to ask the community directly. A total of 95 entities from 37 countries (more than 50% of which were in Europe) responded to our online questionnaire, which was sent during September and October 2017.

Respondents felt the strongest about the lack of visibility of transaction-related costs, followed by the lack of information throughout the life cycle of the payment and lack of data and/or incomplete transaction reference data, which create problems in reconciling transactions. Interestingly, the direct costs associated with messaging fees charged by the network were considered the least important.

Different models for cross-border payments

We then held a number of industry focus group sessions with a selection of respondents where the aim was to propose a potential approach to remove the identified pain points. In those discussions, the first of which took place in January 2018, we developed a set of seven design scenarios for the future of cross-border payments. Our main objective was to propose a blueprint to take correspondent banking into the digital age. This could translate into a new model altogether (i.e. correspondent banking arrangements being replaced by something else) or represent changes to the way the system works today, for example in relation to the messaging system/type/content, or the introduction of utilities. Key requirements were:

- Settlement (including synchronisation);

- Liquidity efficiency;

- Availability (technical access and uptime);

- Ubiquity (relevant connectivity between systems and players);

- Transparency;

- Predictability; and

- Interoperability of systems.

Scenario 1: SWIFT gpi

"Cross-border payments would significantly benefit from harmonised conduct rules"

The SWIFT Global Payments Innovation (gpi) solution provides a cloud-based service, accessible via application programming interfaces (APIs) or MT199 messages, which enables financial institutions (FIs) to track their payment transactions in real time by deploying the Unique End-to-End Transaction Reference (UETR) for every gpi transaction. The transparency along the chain around payment fees and the final payment amount that will reach the beneficiary supports users in better managing their accounts payables. Participants already see significant reductions in their payment enquiry costs.2

Even though gpi is only a messaging solution and does not deliver settlement, it does support transparency and risk management in commercial credit settlement. SWIFT gpi does not require structural changes to the current correspondent banking Nostro/Vostro account-based model and does not require banks to rethink and replace their front-to-back office infrastructures. Our recommendation is for participating FIs in correspondent banking to embrace and implement SWIFT gpi, to their own and their clients’ benefit.

Scenario 2: SWIFT gpi next generation

This looked further at reducing systemic risk in the critical area of inter-bank high-value payments. The aim of reducing settlement and counterparty risks in correspondent banking is being tackled from a gpi perspective with the rollout of the gpi Financial Institutions Transfer (gFIT) service. The underlying rulebook will require FIs to confirm to the tracker once the beneficiary’s agent’s Nostro account has been credited, or flag any processing issues inside the FI, such that FI intraday liquidity management can become more accurate and reconciliations of payments can improve.

By 2022/2023, SWIFT is planning to migrate to the ISO 20022 standard, including gpi, which will allow parties to send more data in the payment message.

A planned ‘pre-validation service’ will further support preventing straight-through processing (STP) and data gap-related issues (e.g. missing clearing codes), as well as problems with closed or wrong beneficiary accounts down the payment chain. And finally, the case resolution service currently under exploration would support FIs in the context of missing information in payments.

Scenario 3: Regional RTGS

20%

In this model, we see national real-time gross settlement (RTGS) systems directly connecting with each other. An example of this is in rollout mode across six countries in the Middle East under the Cooperation Council for the Arab States of the Gulf (GCC).

A central RTGS system links all participating RTGS systems and thus provides a full cross-border solution. The domestic RTGS systems in the region have accounts in each other’s books, enabling transactions via the system to settle immediately with finality in central bank money. This will provide financial stability. However, the GCC model is very specific to this region and it is unlikely that this can be easily replicated at a global scale, given the legal, regulatory and political issues, as well as standards- and operational-related challenges of alignment.

Scenario 4: Clearing bank

This is a scenario that captures the situation where a clearing bank – narrow bank – connects individual banks and corporates to an automated clearing house (ACH) and allows them to exchange funds in real time, leveraging the bank’s messaging network. This scenario is already live in the UK3 with an ambition to expand globally.

Settlement is achieved in near real-time in commercial bank credit and all positions are pre-funded, such that counterparty credit risk is managed.

The success of this model depends on the extent of network adoption. This is likely to be a challenge, as would be costs arising from know your customer (KYC) and anti-money laundering (AML) risk management, in particular at a cross-border level. The liquidity and settlement dimension will also be challenging as higher-value transactions start to be processed.

Scenario 5: ACH interconnectivity

Rather than having one and the same clearing bank, a more complex but also more network-effect-friendly system would be the interconnection of national ACHs. The difference between this model and the clearing bank model is reflected in the need to have an overall interoperability scheme rulebook, complemented by harmonised messaging standards.

Overall, the clearing bank and ACH interconnectivity models have limited application in the context of managing settlement risk in the high-value cross-border inter-bank space. ACH transactions are not immediate and irrevocable in all instances, and systems usually have transaction amount limits.

Scenario 6: Market utility

Expanding the regional RTGS system hub creation (with the GCC model as an example), one could also consider the creation of a global market utility that facilitates settlement in central bank money by connecting country RTGS systems on the one hand and commercial banks on the other. This could ultimately deliver a payments and settlement utility for global trade and trading. However, its implementation would face a number of non-trivial challenges, ranging from network adoption to agreement on a common scheme rulebook and compliance with multiple regulatory regimes. The entity would have to be a regulated financial market infrastructure (FMI). Many open questions remain with this model. For example, in what currency would settlement take place? How would liquidity across the system be managed? Would the FMI be responsible for sanctions/AML/CTF? In which currency would FIs have to fund their accounts with the FMI?

Scenario 7: RTGS interconnectivity leveraging DLT/synchronisation

A variant of the global settlement utility model could be the deployment of the method of synchronisation, leveraging emerging (e.g. distributed ledger technology (DLT)) or existing technologies. Such a model is currently being discussed in central bank circles.

In the future, we could even imagine central banks issuing fiat currency on the DL (Central Bank Digital Fiat Currency (CBDFC)), where interledger protocols could provide central bank-settled cross-border payments via atomic settlement. Cross-border legal and regulatory questions would need to be tackled, as well as the extent to which such a solution could truly reduce inter-bank settlement and counterparty risk.

Policy recommendations

For the purpose of ensuring a harmonised process of identification of payers and payees in a transaction, it is recommended to use the global Legal Entity Identifier (LEI) – a standard identifier for legal entities – in the payment message. Technology, in this instance DLT, could be used to broadcast the LEIs of participating institutions to the market.

The development of a second standard identifier for individuals could also be considered and ISO might be an appropriate entity to look into such standardisation work. The development of national KYC registries should be encouraged further. Note that various types of local and regional registry solutions have already started to emerge, such as the SWIFT KYC Registry, and the KYC utility being explored by the Nordic banks. One could even consider putting registries on a DL, and the legitimacy of use of such registries could be supported by the Basel Committee in collaboration with the Financial Action Task Force (FATF). An essential item to address in all of this is legal liability for KYC in the context of outsourcing.

"Our main objective was to propose a blueprint to take correspondent banking into the digital age"

The process of AML/CTF-related information sharing between FIs across borders also needs improvement. Local data privacy legislation and unclear messages from various national regulators make this difficult today.

And finally, cross-border payments would significantly benefit from harmonised conduct rules, in particular regarding transparency around fees, deductions and FX rates applied, as well as the prohibition to take float on incoming customer payments.

Harnessing innovation

Our research highlights that innovation is available today that can significantly improve the way cross-border payments are being executed. gpi is the answer, here and now. We also demonstrate that network governance is a key requirement that cannot be delivered by technology alone. SWIFT is well positioned to continue providing both network and governance, but technology change cannot be overlooked. This is why we recommend that SWIFT continues its work on exploring DLT as a potential model for the next generation of messaging. The role of APIs will be equally key in this context. It is therefore encouraging to note that SWIFT has just announced a proof of concept with enterprise blockchain software firm R3 in relation to creating a connectivity between DLT and gpi.

Ruth Wandhöfer is a regulatory and fintech expert in the financial services space and is pursuing a PhD on blockchain at Cass Business School, London

Barbara Casu is the Director of the Centre for Banking Research at Cass Business School, where she is Professor of Banking and Finance

Sources

1 See https://bit.ly/2T6SqmS at swiftinstitute.org

2 See https://bit.ly/2q9O80r at swift.com

3 ClearBank, launched in 2017, is the UK’s first new clearing bank in more than 250 years. See http://www.clear.bank/ at clear.bank

Go to Corporate Bank EXPLORE MORE

Find out more about products and services

Go to Corporate Bank Go to Corporate Bank

Stay up-to-date with

Sign-up flow newsbites

Choose your preferred banking topics and we will send you updated emails based on your selection

Sign-up Sign-upYou might be interested in

CASH MANAGEMENT {icon-book}

One-way ticket One-way ticket

The Covid-19 pandemic forced corporate treasury teams to suddenly adapt to working from home, but not all of them are planning a return journey to the office anytime soon, reports Rebecca Brace

CASH MANAGEMENT {icon-book}

Heart of the enterprise Heart of the enterprise

Business software provider SAP leads a consistent programme of innovation, the latest being its digital boardroom. Head of Global Treasury Steffen Diel demonstrates why leaving one’s comfort zone and being permanently curious can work miracles

CASH MANAGEMENT

Cybersecurity and fraud protection: exposing bad actors Cybersecurity and fraud protection: exposing bad actors

As spear phishing, business email compromise and other attacks on corporates increase, the chief information security officer is everyone’s new best friend, report Wade Bicknell and Vanessa Riemer.