-

Securities services, Technology

Beyond the proof of concept

07 August 2024

With spot Ethereum exchange traded funds (ETFs) approved by the US Securities and Exchange Commission, cryptocurrency democratisation is advancing. This regulatory clarity could spell lower costs for asset management service providers. flow explains why, drawing on insights and published research from Deutsche Bank digital asset experts

MINUTES min read

While distributed ledger technology (DLT) itself is not new, its adoption in the financial services industry has evolved very rapidly over the past two years. Initially driven by consumers, interest from institutional players in digital assets has subsequently also surged. This presents a significant opportunity for financial institutions, not least because of the potential to deliver asset management services more quickly and at a lower cost. Through accelerating digitisation, tokenisation of a multitude of assets and the emergence of native digital assets, it is clear the financial services ecosystem will need to evolve to support these new and innovative business models. Moving beyond proofs of concept into adoption will require round-the-clock capabilities and enhanced risk management practices, and can only truly deliver its full potential through programmability and composability. Both of these key features allow new business models, facilitated through tokenisation (the conversion of rights to an asset into a distinct digital token on a blockchain network).

Maturing regulatory stance

Comprehensive regulation is on the horizon and the regulatory landscape has been maturing. For example, Markets in Crypto-Assets (MiCA), a pan-European regulation, was signed on 31 May 2023 and applies from 30 December 2024.1 “By enhancing the protection of consumers and investors as well as financial stability, the regulation promotes innovation and the use of crypto-assets,” says the European Parliament. MiCA aims to provide much-needed clarity and oversight for the crypto markets within EU borders.

“The technology that powers crypto is undeniably powerful”

In the US, holistic rules are still lacking, but regulatory authorities are beginning to take a more assertive stance and have prioritised penalties for lax controls relating to traditional finance firms. For example, 49% of all actions in the 2023 fiscal year made by the Commodity Futures Trading Commission (CFTC) involved digital asset commodities, a total of 47 actions.2 On 22 May 2024, the US House of Representatives voted in favour of the Financial Innovation and Technology for the 21st Century Act (FIT21), the first major crypto bill to pass the House.3 The resulting legislation would establish a regime to regulate the domestic crypto market, with defined consumer protections, involving the installation of the CFTC as the key regulator. The bill now awaits approval in the Senate.

We perceive regulation as a net positive for the industry as the clearer regulatory framework will drive further adoption and go some way towards addressing volatility.

Issuance

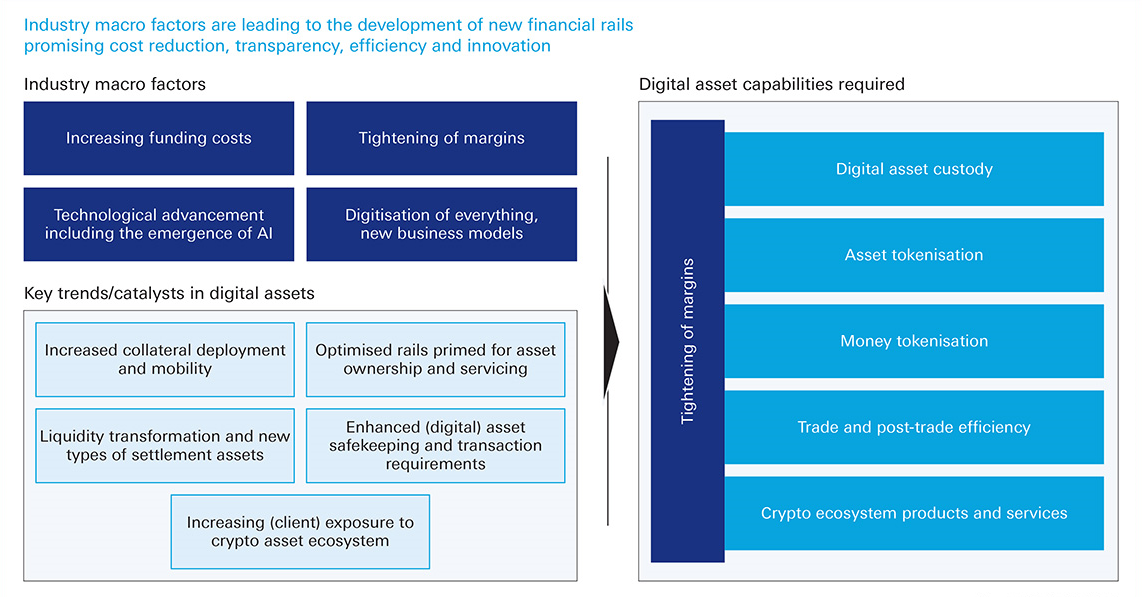

Significant progress has been made by global banks, with around US$4bn in digital bonds issued.4 While the value is very small compared to traditional issuance, the size, investor base and sophistication of these issuances has been growing. Apart from the issuance of native digital assets, several platforms are being built to achieve financial resource optimisation with the existing asset inventory, such as HQLAx, which aims to provide collateral capabilities enhanced by usage of DLT. To support the complete digital assets and currencies lifecycle, a whole range of capabilities is required that include digital asset custody, asset tokenisation, money tokenisation, trade and post-trade efficiency and crypto ecosystem products and services (see Figure 1).

Figure 1: Industry macro factors and digital asset trades

Source: Deutsche Bank

Most banks have segregated their approach towards the crypto ecosystem or DLT-based financial markets ecosystem, with almost all pursuing the latter and some with exposure in the former. Whatever the appetite for this asset class, the technology that powers crypto is undeniably powerful and we are seeing it make significant inroads into business – such as bitcoin ETFs being offered by highly regulated large-scale financial institutions. Collateral mobility through tokenisation is another key driver and this has led to recent announcements by major financial institutions of tokenised money market funds that seek to put to work high-quality liquid assets (HQLAs) that would otherwise be under-utilised. The potential of other new investment classes and real-world assets through tokenisation is just the beginning.

“The crypto world is gradually moving towards greater institutionalisation”

Crypto’s democratisation journey

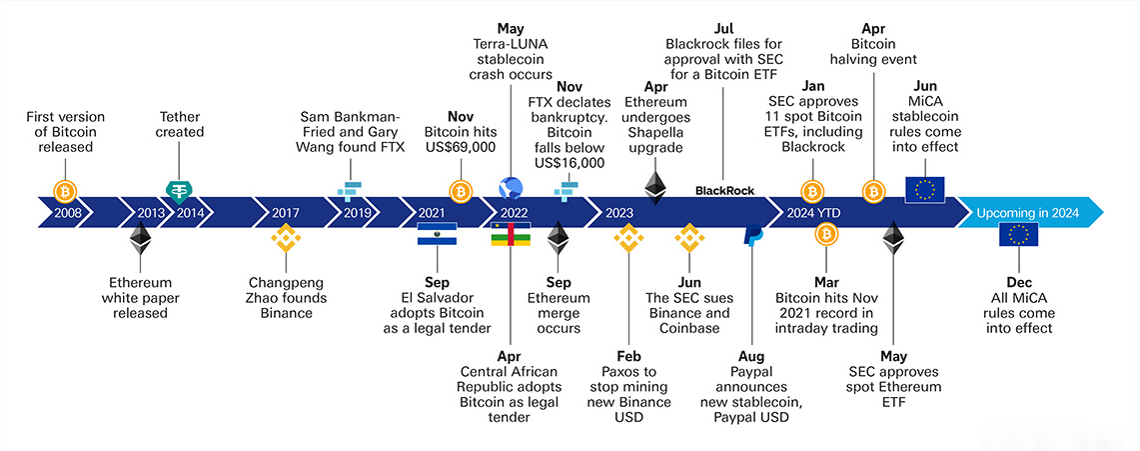

Despite efforts to clean up the crypto market and the implementation of new regulations like the EU MiCA Regulation, bitcoin’s and ethereum’s 30-day volatility still surpasses that of other major asset classes – in fact, volatility in the crypto market has increased recently in the period leading up to approval of both the spot bitcoin and ethereum ETFs.

On 23 May 2024, the Securities and Exchange Commission (SEC) approved all eight ethereum spot ETF applications: Ark Invest, VanEck, Grayscale, BlackRock, Bitwise, Invesco, Franklin Templeton and Fidelity. The SEC has since approved the final S-1 forms (required to publicly offer the new securities), enabling trading from 23 July 2024. This will be the first spot ethereum ETF available in the US for retail investors, following the approval of the spot bitcoin ETF in January. Bitcoin prices have surged 55% since then, and hit an all-time high of US$73,805 in March.

The crypto world is gradually moving towards greater institutionalisation as traditional financial players enter the market, and we expect prices to remain elevated. Upcoming spot ETF and exchange-traded product (ETP) approvals could drive further adoption by allowing for direct crypto exposure within the traditional financial system.

Cross-border payments, tokenisation and Project Agorá

The Bank for International Settlements (BIS) has long championed innovation in financial markets and in particular has written extensively on cross-border payments, tokenisation and central and commercial bank money. Beyond this, it has overseen several important projects, often run through its innovation centres, focusing on a variety of use cases. These have involved both private and public participation.

Project Agorá is one such recently announced initiative that seeks to showcase the benefits of tokenised cross-border payments while maintaining the two-tier financial ecosystem of today (commercial bank money transactions backed by central bank money).5 Through the involvement of seven central banks (Bank of England, Federal Reserve, Bank of Japan, Bank of South Korea, Bank of Mexico, Banque de France and Swiss National Bank), all five major currencies and up to around 30 commercial banks and private sector institutions, this is a major and significant industry undertaking. It is anticipated that a platform will be developed to simulate such transactions, with the possibility of moving into full production. Such a platform could potentially lead to the establishment of a new financial market infrastructure running new critical banking rails.

Figure 2: Timeline of cryptocurrency ETF developments

Source: Deutsche Bank

Sources

1 See europarl.europa.eu

2 See cftc.gov

3 See congress.gov

4 See hkma.gov.hk

5 See fintechfutures.com

You might be interested in

WHITE PAPERS/GUIDES

Regulatory outlook in securities services – H2 2024 Regulatory outlook in securities services – H2 2024

Updated twice a year, this issue of the Regulatory outlook in securities services white paper provides a deep dive into regulations impacting the post-trade landscape. Written by Deutsche Bank’s Boon-Hiong Chan and Britta Woernle, it covers accelerated settlement, digital assets, artificial intelligence, and client asset protection across various regions

WHITE PAPERS/GUIDES

The road to institutional DeFi The road to institutional DeFi

The evolution of decentralised finance (DeFi) – and the potential to apply it to institutional use cases where financial applications are built on blockchain technologies deploying smart contracts – is being met with great interest by industry spectators. Proponents see a strong case for the rise of a new financial paradigm, which is based on the principles of cooperation, composability, open-source code; and is underpinned by open, transparent networks

White papers and guides

Digital identity Digital identity

Identity is everything. It is key to the inner workings of our societies, governments and economies. Without it, we can only have the narrowest of realities: one without legal agreements, banking services, or even getting paid. Identity is the key to trust, and trust, really, is everything